They look almost identical on the surface. Both track the same indexes. Both charge tiny fees. Both have crushed actively managed funds for decades. So why does the internet treat index funds vs ETFs like some complicated debate?

Here’s the truth: for most beginners, the difference is smaller than you think — but in specific situations, picking the wrong one could cost you in fees, taxes, or just plain confusion.

This guide gives you the honest, plain-English breakdown. No jargon. No vague advice. By the end, you’ll know exactly which one fits your situation — and which popular options are worth a look in 2026.

1. Index Funds vs ETFs: The One-Line Answer

Index fund = you buy it once, it runs itself, prices update at end of day.

ETF = trades like a stock during market hours, slightly more flexible, often a tiny bit cheaper.

That’s it. Both track the same markets. Both are low-cost. Both beat most actively managed funds over the long run. The differences only really matter depending on how you invest, where you invest, and how much you care about taxes.

Pro Tip: If you’re investing inside a 401(k) or IRA, the tax difference between index funds and ETFs is basically zero. The ETF tax advantage only shows up in a regular taxable brokerage account.

2. What Is an Index Fund?

An index fund is a type of mutual fund that automatically copies a market index — like the S&P 500, which tracks the 500 largest U.S. companies. Instead of a fund manager picking stocks (and usually underperforming), the fund just… buys everything in the index. Automatically.

You buy shares directly from the fund company (like Vanguard or Fidelity). The price — called the Net Asset Value (NAV) — is calculated once per day, after the market closes at 4 p.m. ET. It doesn’t matter if you place your order at 9 a.m. or 3:30 p.m. — you get that day’s closing price.

Key features:

- Priced once daily at market close

- Bought directly from the fund company or through a brokerage

- Many have a minimum investment (Vanguard’s VFIAX requires $3,000; Fidelity and Schwab often require nothing)

- Automatically reinvests dividends in many cases

- Ideal for automated, recurring investments (dollar-cost averaging)

The biggest names in index funds — Fidelity, Vanguard, and Schwab — have driven costs so low that some index funds now charge literally 0% in fees. Fidelity’s ZERO Large Cap Index fund charges 0% expense ratio and has no minimum investment amount, so you can start investing with as little as $1. Semrush

3. What Is an ETF?

An ETF (Exchange-Traded Fund) works almost exactly like an index fund — except it trades on a stock exchange throughout the day, just like Apple or Tesla stock. You can buy or sell it at 10:14 a.m. and get that exact moment’s market price.

Most ETFs are also index funds — they track the same S&P 500, NASDAQ, or bond indexes. The difference isn’t what they track. It’s how you buy and sell them.

Key features:

- Priced in real-time, all day during market hours

- Bought through any brokerage account (Fidelity, Schwab, Robinhood, etc.)

- No minimum investment beyond the cost of one share (some brokers offer fractional shares)

- Slightly more tax-efficient in taxable accounts

- Cannot typically automate purchases as easily as index funds

ETFs typically have no minimum investment beyond the price of one share. Vanguard’s VOO, one of the most popular S&P 500 ETFs, trades at roughly $500 per share as of 2026. Some brokers offer fractional shares, lowering the entry point further. Link Assistant

4. The 7 Real Differences Between Index Funds and ETFs

| Feature | Index Fund | ETF |

|---|---|---|

| How you buy it | Directly from fund company or broker | Through any brokerage, like a stock |

| When price is set | Once daily at market close | Real-time throughout trading day |

| Minimum investment | $0–$3,000 depending on fund | Cost of 1 share (often $50–$500) |

| Expense ratio (avg 2025) | 0.05% average | 0.14% average (but 0.03% for top S&P 500 ETFs) |

| Tax efficiency | Good | Slightly better in taxable accounts |

| Automatic investing | Easy to set up recurring buys | Less straightforward to automate |

| Intraday trading | Not possible | Yes — buy/sell any time market is open |

The most important row? Expense ratio. The Investment Company Institute found index mutual funds’ expense ratios were 0.05% per year on average in 2025. Index equity ETFs’ asset-weighted average expense ratio for 2025 was higher, at 0.14% — but some S&P 500 ETFs charge 0.03% or less per year. Google Support

That means the “ETFs are always cheaper” rule isn’t automatic. You have to compare specific funds.

5. Expense Ratios: The Numbers That Actually Matter

This is where most beginner articles get lazy — they say “both are cheap” and move on. Let’s be more specific.

An expense ratio is the annual fee you pay the fund, expressed as a percentage of what you have invested. On $10,000 invested:

- 0.03% expense ratio = you pay $3 per year

- 0.50% expense ratio = you pay $50 per year

- 1.00% expense ratio = you pay $100 per year

Over 30 years, that difference compounds into thousands of dollars. Here’s what the top S&P 500 funds actually charge in 2026:

| Fund | Type | Expense Ratio | Min. Investment |

|---|---|---|---|

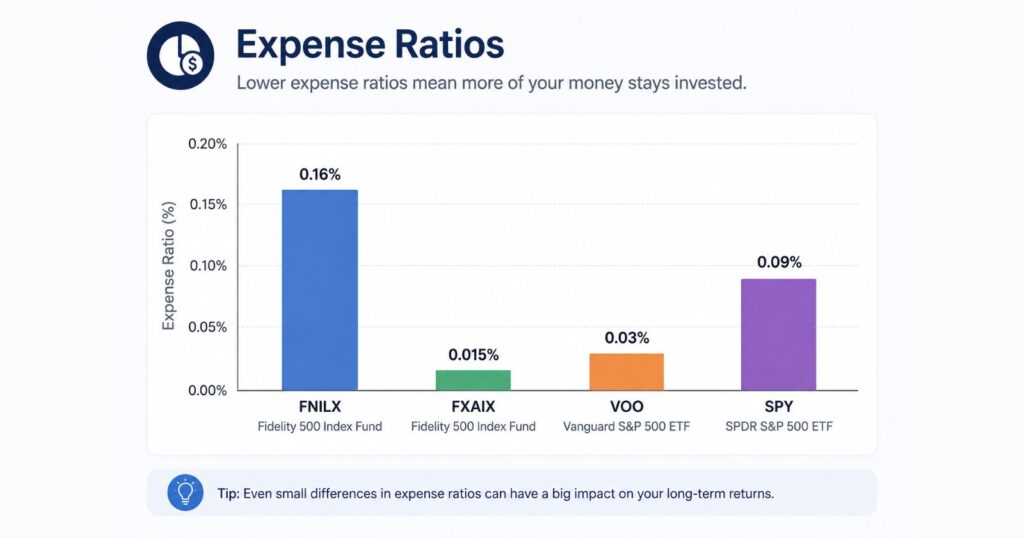

| Fidelity ZERO (FNILX) | Index Fund | 0.00% | $0 |

| Schwab S&P 500 (SWPPX) | Index Fund | 0.02% | $0 |

| Fidelity 500 (FXAIX) | Index Fund | 0.015% | $0 |

| Vanguard 500 (VFIAX) | Index Fund | 0.04% | $3,000 |

| Vanguard S&P 500 (VOO) | ETF | 0.03% | ~$500/share |

| iShares Core S&P 500 (IVV) | ETF | 0.03% | ~$600/share |

| SPDR S&P 500 (SPY) | ETF | 0.095% | ~$600/share |

VFIAX (mutual fund) charges 0.04% vs VOO (ETF) at 0.03%. The gap is small but compounds over decades. Link Assistant

The takeaway: Fidelity’s index fund (FXAIX at 0.015%) is actually cheaper than most ETFs. The idea that ETFs are automatically lower-cost is a myth worth busting.

6. Tax Efficiency: Which One Keeps More of Your Money?

This is the one area where ETFs have a genuine, structural advantage — but only in specific accounts.

In a 401(k) or IRA: Tax efficiency doesn’t matter at all. Both grow tax-free or tax-deferred. Choose whichever is available.

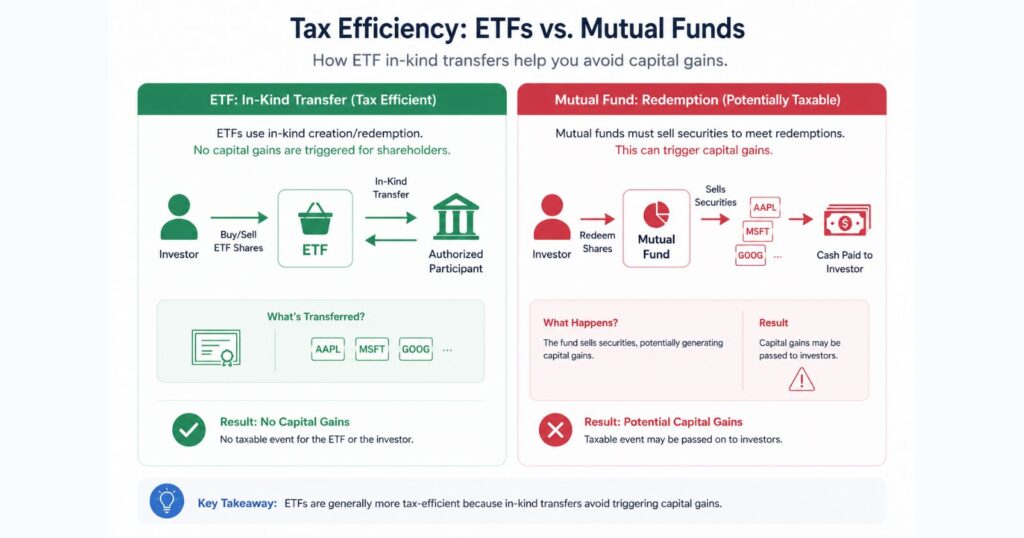

In a taxable brokerage account: ETFs win.

Here’s why. When investors sell shares of a mutual fund (including index funds), the fund sometimes has to sell underlying stocks to meet those redemptions — which can trigger capital gains distributions that get passed to all shareholders, even ones who didn’t sell anything.

ETFs use a different mechanism called in-kind transfers that largely avoids this. The result? ETFs are generally more tax-efficient due to their ability to avoid distributing capital gains, which can help maximize your after-tax returns over the long term. Sencha Tea Bar

If you’re investing in a taxable account and you’re in a high income bracket, this matters a lot. If you’re investing inside a Roth IRA or 401(k), it’s irrelevant.

7. Real Examples: Vanguard, Fidelity & Schwab Side by Side

Let’s look at how this plays out with real funds that track the same index — the S&P 500:

Vanguard:

- Index Fund: VFIAX — 0.04% expense ratio, $3,000 minimum

- ETF: VOO — 0.03% expense ratio, no minimum (fractional shares available)

- Verdict: VOO wins on cost and accessibility

Fidelity:

- Index Fund: FXAIX — 0.015% expense ratio, no minimum

- ETF: No direct equivalent S&P 500 ETF at Fidelity

- Verdict: FXAIX is one of the cheapest options available, period

Schwab:

- Index Fund: SWPPX — 0.02% expense ratio, no minimum

- ETF: SCHB — 0.03% expense ratio, no minimum

- Verdict: The index fund is actually cheaper here

The point? Costs are among the lowest, and these funds mirror the S&P 500 closely, making them a good fit for investors who want full participation in both market ups and downs. Compare the specific funds — not the categories. Practical Ecommerce

8. Which One Should a Beginner Start With?

Here’s a simple decision tree:

Start with an Index Fund if:

- You want to invest automatically every month (paycheck → investment, on autopilot)

- You have less than $500 to start and your broker requires a minimum for ETFs

- You’re investing inside a 401(k) — index funds are almost always the only option anyway

- You don’t want to think about market prices, bid-ask spreads, or timing

- You prefer total simplicity over maximum optimization

Start with an ETF if:

- You’re opening a taxable brokerage account and want maximum tax efficiency

- You want to invest with as little as $1 (via fractional shares on Fidelity or Schwab)

- You like knowing you can sell at any moment during the trading day

- You want access to niche strategies (sector ETFs, international ETFs, bond ETFs) easily

Both are excellent, but index funds suit beginners who prefer automation. ETFs offer more flexibility for active investors. Slow Living Kitchen

For most people reading this, the honest answer is: it barely matters. Pick one, start investing, and don’t stop. The gap between VOO and FXAIX over 30 years is tiny compared to the gap between investing at all versus waiting for the “perfect” choice.

9. Can You Own Both?

Absolutely — and many experienced investors do.

A common approach: hold index funds inside your 401(k) or IRA (because that’s what’s available), and hold ETFs like VOO or IVV in a taxable brokerage account for the tax efficiency advantage.

Many investors hold both for diversification and balance. There’s nothing wrong with this. Just make sure you’re not doubling up on the same index in a way that gives you the illusion of diversification without the reality. Slow Living Kitchen

For more practical personal finance guides, check out InfoBrave’s Finance section — and browse InfoBrave for more everyday guides on money, tech, and lifestyle.

Financial Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always do your own research and consult a licensed financial advisor before making investment decisions.

10. Frequently Asked Questions

What is the main difference between index funds and ETFs?

The main difference is how and when you buy them. Index funds price once at market close and are purchased directly from the fund company. ETFs trade like stocks throughout the day at real-time prices. Both track the same market indexes and offer similarly low fees — the practical difference for long-term investors is small.

Are ETFs riskier than index funds?

No. Both carry the same market risk since they track the same indexes. ETFs fluctuate in price throughout the day while index funds are priced once daily, but this doesn’t make ETFs riskier for long-term investors — it’s simply a structural difference in how they trade.

Which has lower fees — index funds or ETFs?

It depends on the specific fund. Index mutual funds averaged 0.05% expense ratios in 2025 versus 0.14% for index equity ETFs on average — but some S&P 500 ETFs charge 0.03% or less. Fidelity’s FXAIX index fund (0.015%) is cheaper than most ETFs. Always compare specific funds, not categories. Google Support

Is Vanguard VOO an index fund or an ETF?

VOO is an ETF — the Vanguard S&P 500 ETF. It tracks the S&P 500 index but trades like a stock on the NYSE. Vanguard also offers VFIAX, which is the mutual fund version of essentially the same thing, with a $3,000 minimum investment.

Can I lose all my money in an index fund or ETF?

Both carry market risk — if the entire stock market crashed to zero, yes, you’d lose everything. But that would require every major U.S. company to go bankrupt simultaneously. In practice, index funds and ETFs that track broad markets like the S&P 500 have never permanently lost value over any 20-year period in history.

Which is better for a Roth IRA — index funds or ETFs?

Inside a Roth IRA, there is no meaningful difference in tax treatment. Both grow tax-free. Choose based on convenience, minimum investment requirements, and expense ratio. If your broker offers a great index fund like FXAIX at 0.015% with automatic investing, that’s hard to beat.

Do index funds and ETFs pay dividends?

Yes, both distribute dividends — typically quarterly. Index funds often reinvest dividends automatically. ETFs distribute dividends as cash, which you can then reinvest manually or set to auto-reinvest (DRIP) through your broker.

You may also like: Top 10 Personal Finance Tips for Millennials