Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, legal, or insurance advice. Rates shown are averages compiled from third-party sources and will vary based on your personal driving profile, location, vehicle, and insurer. Always obtain personalised quotes before making coverage decisions.

Texas is not a cheap state for car insurance. With three of the largest cities in the country, a high proportion of uninsured drivers, and increasingly severe weather events, insurers price Texas policies to reflect real risk. The result: the average full-coverage policy in Texas now costs somewhere between $150 and $247 per month depending on which data source you trust — significantly above the national average in most analyses.

But averages are almost meaningless here. The difference between the most expensive and cheapest major insurer in Texas can exceed $2,000 per year for the same driver. The difference between the cheapest and most expensive city in the state is over $100 per month. And the difference between a driver who shops around and one who stays with their current insurer on autopilot can be hundreds of dollars annually.

This guide gives you real 2026 rates, ranks the cheapest insurers for every major driver profile, explains exactly what’s driving Texas premiums, and shows you the specific steps to reduce what you’re paying — starting today.

1. What Texas Drivers Actually Pay in 2026

Texas car insurance rates in 2026 vary noticeably between sources, because different analysts use different driver profiles, coverage levels, and ZIP code mixes. Here’s an honest overview of what the major data sources show for a typical driver:

| Coverage Type | Average Monthly Cost | Average Annual Cost |

|---|---|---|

| Minimum liability only | $65–$87/month | $780–$1,044/year |

| Full coverage (all sources avg.) | $150–$247/month | $1,800–$2,964/year |

| State average (Insure.com) | $259/month | $3,106/year |

The variation between sources reflects different driver profiles — a 40-year-old with a clean record pays far less than a 20-year-old with a recent accident. The takeaway: if your premium is above $250/month for full coverage and you have a clean record, you’re likely overpaying and should get competing quotes immediately.

Texas ranks as the 14th most expensive state for car insurance nationally. The main reasons: three of the country’s largest cities (Houston, San Antonio, Dallas) generate high accident frequency; around 14.5% of Texas drivers are uninsured, raising costs for everyone; and the state’s severe weather history — from flooding to hailstorms — drives comprehensive claims upward.

2. Cheapest Car Insurance Companies in Texas: Ranked

Based on 2026 rate data from NerdWallet, ValuePenguin, U.S. News, Insure.com, WalletHub, and Bankrate, here are the consistently cheapest insurers for Texas drivers with clean records.

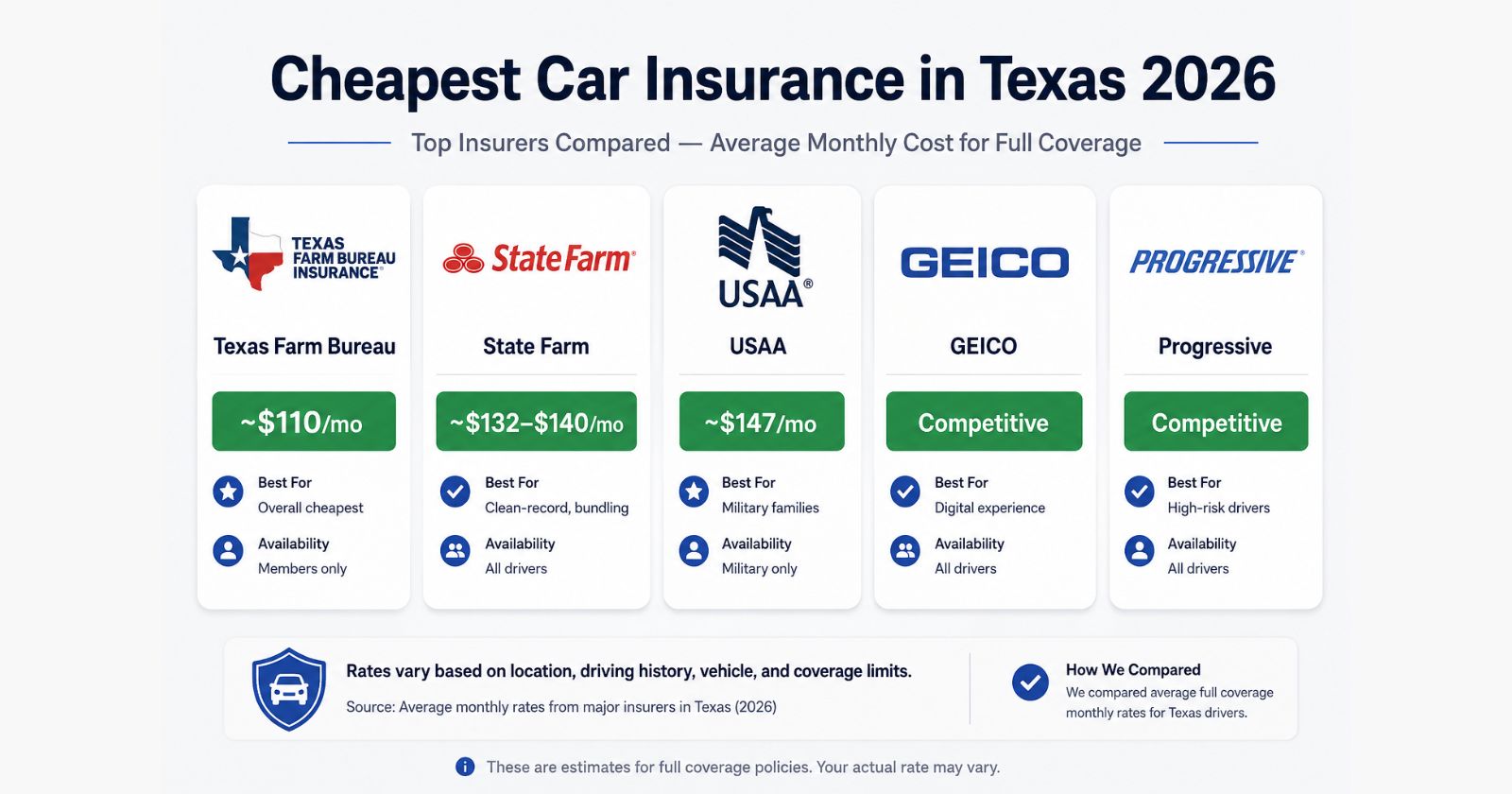

Texas Farm Bureau — Overall Cheapest (Members Only)

Texas Farm Bureau appears at or near the top of every major 2026 ranking for outright cheapness. As a member-owned company focused exclusively on Texas, it can price more competitively than national carriers. Full coverage runs around $110/month ($1,321/year) in NerdWallet’s analysis, and as low as $940/year in U.S. News data. Membership requires a nominal annual fee, but the savings typically far exceed it.

Best for: Budget-conscious drivers willing to join a membership organisation. Young drivers on a parent’s policy. Drivers with poor credit (also strong here).

Limitation: Members only. No national footprint. Fewer digital tools than major carriers.

State Farm — Best for Most Drivers Without Membership Restrictions

State Farm is the most frequently cited cheapest nationally available insurer in Texas in 2026. Depending on the data source, full coverage runs between $132 and $140 per month — roughly half the Texas average. State Farm has a vast network of local agents across the state, strong customer satisfaction ratings, and substantial bundling discounts for home and auto. It’s also the cheapest option after an at-fault accident, at around $148/month for full coverage.

Best for: Good drivers wanting the cheapest widely available rate. Homeowners who can bundle. Drivers who prefer in-person agent access.

Limitation: No gap insurance product. Discount range narrower than Geico.

USAA — Best for Military Families

For active-duty service members, veterans, and their eligible family members, USAA is consistently either the cheapest or tied for cheapest insurer in Texas. Full coverage runs around $147/month ($1,764/year) in most analyses — well below the state average — combined with the highest customer satisfaction scores in the industry. USAA also offers car replacement assistance that pays out 120% of a car’s value if it’s totalled or stolen, which exceeds standard gap coverage.

Best for: Anyone with military eligibility. The best combination of price and service quality available in Texas if you qualify.

Limitation: Eligibility restricted to military community only.

GEICO — Best Digital Experience and Clean-Record Rates

GEICO earns particular recognition in 2026 for clean-record drivers and for having the most streamlined digital quoting and claims experience. CNBC Select and others cite it as the lowest-premium option for the general public in some analyses. GEICO also offers close to two dozen discounts, including savings for anti-theft devices, new vehicles, and accident-free records, and is one of the more forgiving carriers for drivers with speeding tickets.

Best for: Tech-savvy drivers who prefer a fully digital experience. Clean-record drivers. High-risk drivers with tickets who want competitive rates.

Limitation: Fewer local agent offices than State Farm. No gap insurance.

Progressive — Best for High-Risk Drivers

Progressive is consistently the most competitive insurer for drivers with accidents, tickets, or DUIs on their record. Their Snapshot telematics programme also gives higher-risk drivers a genuine path to lower rates by demonstrating improved driving behaviour. Accident forgiveness is available as an add-on. Not the cheapest for clean-record drivers, but meaningfully competitive where other insurers penalise heavily.

Best for: Drivers with blemished records. Anyone willing to use telematics to earn discounts. Drivers who want accident forgiveness.

Limitation: Rates for clean-record drivers are not as competitive as State Farm or GEICO.

Summary Comparison Table

| Insurer | Full Coverage (monthly) | Best For | Availability |

|---|---|---|---|

| Texas Farm Bureau | ~$110 | Overall cheapest | Members only |

| State Farm | ~$132–$140 | Clean-record, bundling | All drivers |

| USAA | ~$147 | Military families | Military only |

| GEICO | Competitive | Digital experience | All drivers |

| Progressive | Competitive | High-risk drivers | All drivers |

| Allstate | Above average | Wide agent network | All drivers |

| Farmers | Highest among majors | Broad coverage options | All drivers |

3. Best for Specific Driver Profiles

Young Drivers (Under 25)

Young drivers pay significantly more for insurance than any other age group. Texas Farm Bureau has the cheapest rates for young drivers overall, with an average of $166/month ($1,996/year) for full coverage as a standalone policy. The cheapest route for most young drivers is remaining on a parent’s existing policy: Texas Farm Bureau averages $230/month for full coverage covering a new young driver plus two parents — still the cheapest family policy in the state.

Drivers After an At-Fault Accident

State Farm at around $148/month for full coverage is the cheapest post-accident option among major carriers. Progressive is the next most competitive, particularly because their Snapshot programme gives drivers with incidents a way to actively reduce their premium over time.

Drivers After a Speeding Ticket

Texas Farm Bureau offers the cheapest rates for ticketed drivers at approximately $110/month ($1,321/year) for full coverage. GEICO is also notably forgiving on speeding violations compared to carriers like Allstate and Farmers.

Senior Drivers

Senior drivers in Texas generally pay higher rates than middle-aged drivers, though still less than teenagers. State Farm and Texas Farm Bureau offer the most competitive rates for seniors, and both reward clean records more aggressively than most competitors.

Low-Mileage Drivers

Usage-based or pay-per-mile policies can be significantly cheaper for drivers covering fewer than 7,500 miles per year. Progressive’s Snapshot, Allstate’s Drivewise, and State Farm’s Drive Safe & Save all offer telematics-based savings for demonstrably safe, low-mileage driving.

4. Texas Minimum Coverage Requirements (and Why They’re Not Enough)

Texas is an at-fault state, meaning the driver determined to be responsible for an accident is liable for bodily injury and property damages incurred by others. The state requires all drivers to carry minimum liability coverage of:

- $30,000 bodily injury liability per person

- $60,000 bodily injury liability per accident

- $25,000 property damage liability per accident

This is known as 30/60/25 coverage and costs around $65–$87/month on average. Texas law also requires insurers to offer Personal Injury Protection (PIP) for medical bills, though drivers can reject it in writing. Uninsured/underinsured motorist coverage must also be offered with every policy — and given that approximately 14.5% of Texas drivers carry no insurance, this add-on is worth serious consideration.

Why minimum coverage is often insufficient: In a serious accident involving hospitalisation, $30,000 per person can be exhausted quickly. Medical bills, lost wages, and legal fees can all exceed the minimum in a single incident. Most insurance professionals recommend at least 50/100/50 limits — and higher if you own a home or have significant assets that could be targeted in a liability lawsuit.

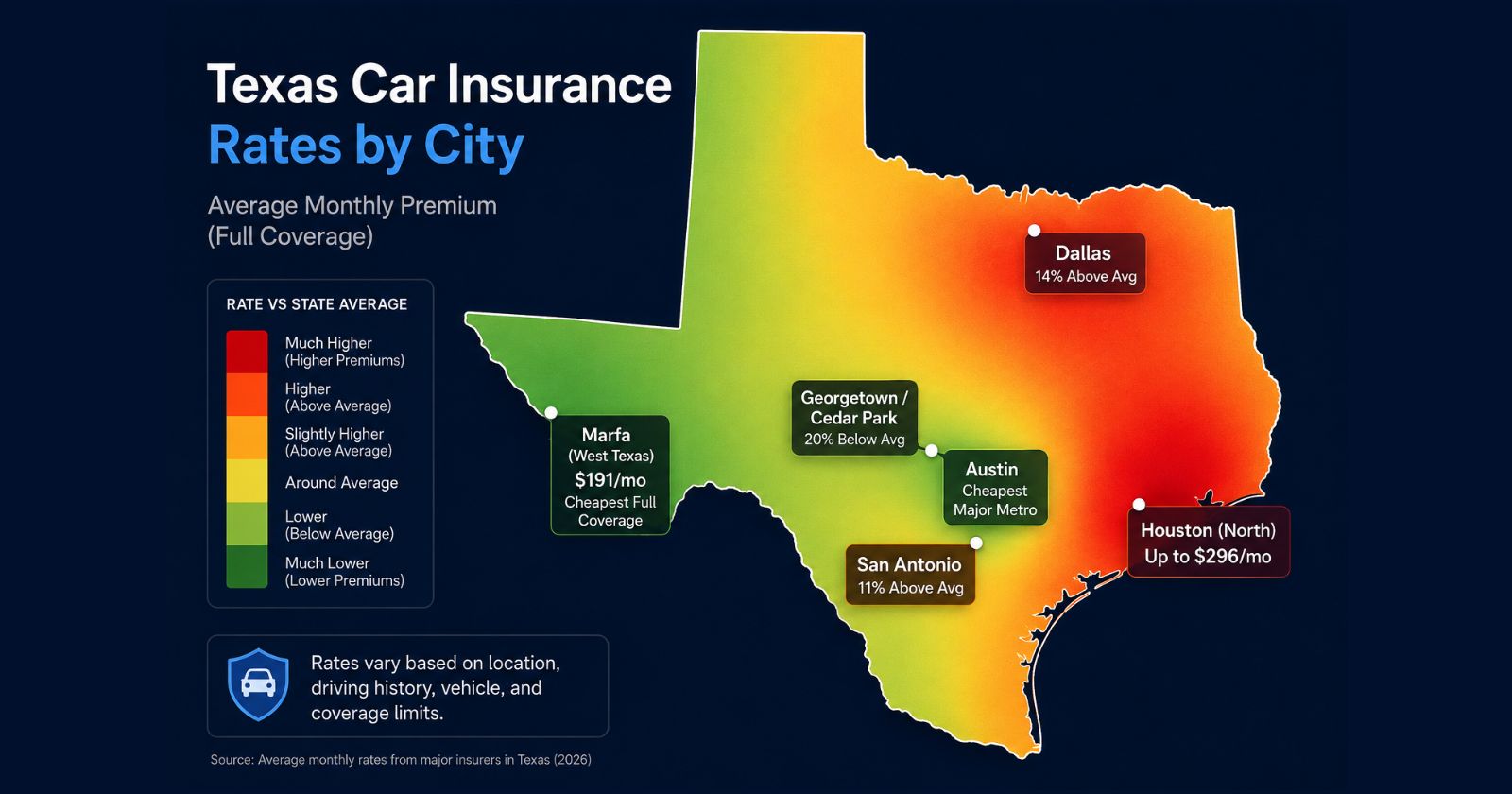

5. How Your City Affects Your Rate

Where you live in Texas can change your premium by over $100 per month for the same policy and driver profile.

| City / Area | Rate vs State Average | Why |

|---|---|---|

| Houston (North) | Up to $296/month full coverage | Highest accident frequency, flood/hurricane exposure, urban density |

| Dallas | ~14% above average | Dense traffic; northern suburbs significantly cheaper |

| San Antonio | ~11% above average | Military activity, dense urban core |

| Austin | Among cheapest major metros | Lower accident frequency, higher income area |

| Austin suburbs (Georgetown, Cedar Park) | ~20% below average | Lower density, fewer claims |

| Marfa (West Texas) | ~$191/month — cheapest full coverage in the state | Very low density, minimal traffic |

The practical lesson: even within the same metro, moving to a suburb can save hundreds per year. If you’re near a city boundary, it’s worth checking quotes with both ZIP codes.

6. The 8 Biggest Factors That Set Your Premium

Insurance companies in Texas can legally consider all of the following when pricing your policy:

1. Driving record. Accidents, tickets, and DUIs all raise your premium. A single at-fault accident can increase rates by 30–50% at many carriers. The impact typically lasts three to five years.

2. Age. Teenagers and young adults under 25 pay the highest rates. Premiums typically decline through middle age, then rise again for drivers over 70 as reaction times and claim frequency increase.

3. Location (ZIP code). Your specific ZIP code determines your exposure to theft, accident frequency, flood risk, and vandalism rates. This is one of the factors you have the least control over.

4. Vehicle type. High-end vehicles, sports cars, and electric vehicles with expensive repair costs all attract higher premiums. Vehicles with strong safety ratings and anti-theft systems attract discounts.

5. Credit history. Texas allows insurers to use credit-based insurance scores. Drivers with poor credit can pay dramatically more than drivers with excellent credit for an identical policy. This is one of the most significant and least-discussed rate factors.

6. Coverage level and deductible. Choosing higher deductibles lowers your premium. Dropping optional coverages on older vehicles (comprehensive and collision) can produce significant savings.

7. Annual mileage. Drivers covering more miles are statistically more likely to be involved in an incident. Low-mileage drivers can save by switching to usage-based policies.

8. Marital status. Insurers view married drivers as statistically lower risk. Married drivers typically pay less than single drivers with an otherwise identical profile.

7. How to Lower Your Car Insurance Rate Right Now

These are the most effective, actionable steps for reducing your Texas car insurance premium:

Get at least three competing quotes. This single step has more impact than almost any other. The difference between the cheapest and most expensive major insurer in Texas can exceed $2,000 per year for identical coverage. Most people last compared quotes when they first bought their policy — rates change constantly and loyalty is not rewarded.

Bundle home and auto. State Farm and Allstate both offer 15–25% savings on bundled home and auto policies. If you have a homeowner’s policy with a different carrier, it’s worth pricing a bundle.

Raise your deductible. Moving from a $250 to a $1,000 deductible on collision and comprehensive can reduce the comprehensive and collision portion of your premium by 30–40%. Only do this if you can genuinely cover the deductible from savings in the event of a claim.

Use telematics. If you’re a safe driver, programmes like State Farm’s Drive Safe & Save, Progressive’s Snapshot, or Allstate’s Drivewise can produce real discounts based on your actual driving behaviour. The key word is “if” — telematics programmes can also raise rates for drivers who don’t drive as safely as they think.

Drop comprehensive and collision on older vehicles. Once a vehicle is worth less than $4,000–$5,000, carrying collision and comprehensive coverage may cost more per year than the maximum payout after the deductible. A vehicle worth $3,000 with a $1,000 deductible means the most you can ever receive is $2,000. If your annual collision premium exceeds what that payout would be worth to you, dropping the coverage makes financial sense.

Improve your credit score. Because Texas allows credit-based pricing, improving your credit score can meaningfully reduce your renewal rate over time. Paying down revolving debt and avoiding new credit enquiries are the most impactful short-term credit moves.

Ask about every available discount. Most insurers have 10–24 discounts that aren’t automatically applied. Common examples: safe driver, good student, anti-theft device, airbag, loyalty, paperless billing, automatic payment, and alumni association memberships. A single call to your insurer asking specifically “what discounts am I not currently receiving?” frequently uncovers savings.

Consider a higher-risk insurer if your record has improved. If you received a ticket or had an accident three or more years ago and are now with an insurer that penalises these incidents long-term, switching to a carrier that weights recent behaviour more heavily (like Progressive or GEICO) can produce significant rate reductions.

8. Full Coverage vs Minimum Coverage: Which Do You Need?

The right choice depends primarily on your vehicle’s value and your financial situation.

Choose minimum coverage if:

- Your vehicle is older and worth less than $4,000–$5,000

- You own the vehicle outright (no lender requiring full coverage)

- You have sufficient savings to replace the vehicle out of pocket if it’s totalled or stolen

- You primarily need liability protection for damage you cause to others

Choose full coverage if:

- You have an auto loan or lease (lenders legally require it)

- Your vehicle is worth more than $8,000–$10,000

- You couldn’t afford to replace or significantly repair the vehicle from savings

- You live in a high-theft or flood-prone area of Texas

One essential add-on regardless of coverage tier: Given that 14.5% of Texas drivers are uninsured, uninsured/underinsured motorist (UM/UIM) coverage deserves serious consideration even on a minimum-coverage policy. Without it, being hit by an uninsured driver means bearing your own injury and vehicle costs, with a lawsuit as the only recovery route.

9. How to Compare Quotes the Right Way

Most people make three mistakes when comparing car insurance quotes: comparing different coverage levels, using a single comparison website and assuming it covers all options, and selecting based on price alone without checking claims satisfaction data.

Here’s how to do it properly:

Step 1: Decide your actual coverage needs first. Before requesting a single quote, decide on your target coverage limits and deductibles. Get every quote at the same spec — otherwise you’re comparing different products, not different prices.

Step 2: Get quotes from at least three sources. Include at least one national carrier (State Farm, GEICO, Progressive), one regional option (Texas Farm Bureau if eligible), and one quote from your current insurer for comparison. Use a comparison tool like The Zebra or NerdWallet alongside direct insurer websites.

Step 3: Check claims satisfaction, not just price. J.D. Power’s claims satisfaction rankings and the NAIC complaint ratio are publicly available and tell you how each insurer actually performs when you need them. A cheaper insurer with a high complaint ratio can be a genuinely poor choice.

Step 4: Ask specifically about discounts on each quote. Don’t assume discounts are pre-applied. Ask each insurer explicitly what discounts you qualify for.

Step 5: Repeat this process every 12 months. Your profile changes (vehicles age, driving records improve, credit scores shift) and so do insurer pricing models. Annual shopping is the simplest recurring money-saving habit for Texas drivers.

10. Frequently Asked Questions

Who has the cheapest car insurance in Texas in 2026?

Texas Farm Bureau has the lowest average rates in most 2026 analyses, with full coverage around $110/month — but it requires membership. Among nationally available carriers open to all drivers, State Farm is consistently the cheapest at around $132–$140/month for full coverage. USAA is cheapest overall for military-affiliated drivers.

What is the average cost of car insurance in Texas in 2026?

Depending on the data source, full coverage averages between $150 and $259 per month for a typical Texas driver. Minimum liability-only coverage averages $65–$87 per month. The variation reflects different driver profiles used in each analysis — your actual rate depends heavily on your age, driving record, location, and vehicle.

What car insurance is required by law in Texas?

Texas requires minimum liability coverage of $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage (30/60/25). Insurers must offer Personal Injury Protection and uninsured motorist coverage, though drivers can decline these in writing.

Can car insurance companies in Texas use my credit score?

Yes. Texas law permits insurers to use credit-based insurance scores when pricing policies. Drivers with poor credit typically pay significantly more than drivers with excellent credit for an otherwise identical profile. Improving your credit score over time can meaningfully reduce your renewal premium.

How much does adding a young driver to a policy cost in Texas?

It varies significantly by carrier, but adding a young driver (under 25) to an existing policy is substantially cheaper than a standalone policy for that driver. Texas Farm Bureau has the cheapest option for a new young driver added to a two-parent policy, averaging around $230/month for the combined family policy.

Is Houston the most expensive city for car insurance in Texas?

Yes, in most analyses. The North Houston area has the highest average full-coverage rates in the state at around $296/month. This reflects the combination of very high accident frequency, flood and hurricane claim exposure, and extreme urban density. Austin is generally the cheapest major metro.

Should I drop full coverage on my older car?

Generally yes, if your vehicle is worth less than $4,000–$5,000, you own it outright, and you could cover replacement or repair from savings. The rule of thumb: if your annual collision and comprehensive premium exceeds 10% of the vehicle’s current market value, the coverage likely isn’t cost-effective. Get the vehicle’s current value from Kelley Blue Book or Carfax before making the decision.

Will my rate go down in Texas in 2026?

Some major Texas insurers have lowered rates in 2026, while at least one major carrier has raised rates. Rate trends vary by company and individual driver profile. The best way to benefit from any downward rate movement is to get competing quotes at renewal — staying with your current insurer doesn’t guarantee you benefit from industry-wide rate reductions.

For more guides on protecting your finances with practical, data-driven strategies, explore InfoBrave’s finance and informative guides.

You may also like: Dollar-Cost Averaging Explained: The Beginner Strategy That Removes All the Guesswork (2026)