Here’s a question that confuses more Americans than almost any other in personal finance: should you open a Roth IRA or contribute to your 401(k) first?

It sounds simple. It isn’t — because the correct answer depends on three things most articles never ask you about: whether your employer matches contributions, what your income is, and what tax bracket you expect to be in during retirement.

Get it wrong, and you could leave tens of thousands of dollars in free money on the table. Get it right, and you’ll have two powerful tax-advantaged accounts working together for you, compounding quietly for decades.

This guide gives you the plain-English explanation of both accounts, the verified 2026 contribution limits straight from the IRS, and a clear step-by-step decision framework — so you’ll know exactly what to do and in exactly what order.

Financial Disclaimer: This article is for educational purposes only and does not constitute financial or tax advice. Tax laws change and individual circumstances vary. Always consult a qualified financial advisor or CPA before making retirement decisions.

1. The Quick Answer (For People in a Hurry)

Before we get into the details, here’s the framework in three sentences:

- Always contribute to your 401(k) first — up to your employer match. That match is a guaranteed, instant 50–100% return on your money. Nothing else comes close.

- Then, open a Roth IRA and max it out — if your income is under the limit ($153,000 single / $242,000 married in 2026).

- Then, go back and contribute more to your 401(k) if you still have money to invest.

That’s the order of operations. The rest of this article explains exactly why.

2. What Is a 401(k)?

A 401(k) is a retirement savings account sponsored by your employer. You tell your HR department what percentage of each paycheck to send directly into the account — before you ever see it. That money then gets invested in a menu of funds your employer has chosen, typically including index funds and target-date funds.

The big appeal: contributions are usually made pre-tax (traditional 401(k)), meaning you don’t pay income tax on that money now. You pay it later, when you withdraw in retirement. This reduces your taxable income today, which can lower your tax bill right now.

Many employers also match a portion of your contributions — essentially depositing extra money into your account based on how much you put in. More on why this is the single most important factor in a moment.

Key facts about 401(k)s:

- Offered only through employers — you can’t open one independently

- Traditional 401(k): contributions are pre-tax, withdrawals in retirement are taxed

- Roth 401(k): contributions are after-tax, withdrawals in retirement are tax-free

- Funds are generally locked until age 59½ — early withdrawal triggers a 10% penalty plus income taxes

- As of 2024, Americans held $9.3 trillion in 401(k) plans across more than 715,000 plans, serving about 70 million active participants Searchvolume

3. What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a retirement account you open yourself, completely independently of your employer. You contribute money you’ve already paid taxes on — and in return, every dollar that grows inside the account is completely tax-free forever, including when you withdraw it in retirement.

That’s the magic of the Roth IRA. You pay tax once, upfront, and then never again — not on the growth, not on the dividends, not on the withdrawals decades later.

Key facts about Roth IRAs:

- You open it yourself through any brokerage — Fidelity, Schwab, Vanguard, or others

- Contributions are after-tax: no tax break today, but total tax-free growth forever

- You can invest in virtually anything: stocks, ETFs, index funds, bonds — your choice

- You can withdraw your contributions (not earnings) at any time, penalty-free

- There are income limits — high earners above a certain threshold cannot contribute directly

- No required minimum distributions during your lifetime — you never have to touch it if you don’t need to

4. Roth IRA vs 401(k): Head-to-Head Comparison

| Feature | 401(k) | Roth IRA |

|---|---|---|

| Who opens it | Your employer | You, independently |

| Contribution type | Usually pre-tax (traditional) or after-tax (Roth 401k) | After-tax only |

| 2026 contribution limit | $24,500 (under 50) | $7,500 (under 50) |

| Employer match | Yes — often 3–6% of salary | No |

| Income limits | None | Yes — phases out above $153K (single) |

| Investment choices | Limited to employer’s menu | Unlimited — any brokerage |

| Tax on withdrawal | Yes (traditional) / No (Roth 401k) | No — completely tax-free |

| Early withdrawal | 10% penalty + taxes before 59½ | Contributions anytime penalty-free |

| Required distributions | Must start at age 73 | None during your lifetime |

| Access if you leave job | Roll over to new 401(k) or IRA | Stays with you, always |

The single most important thing this table shows: the 401(k) has a much higher contribution limit and offers employer matching. The Roth IRA offers more flexibility, more investment options, and completely tax-free growth. They’re not competing — they’re complementary.

5. 2026 Contribution Limits: The Exact Numbers

These are the official IRS-confirmed limits for 2026:

401(k) contribution limits 2026

The 401(k) contribution limit increased to $24,500 for 2026, up from $23,500 in 2025. Google Support

| Age group | 2026 employee limit | Catch-up | Total allowed |

|---|---|---|---|

| Under 50 | $24,500 | — | $24,500 |

| 50–59 | $24,500 | +$8,000 | $32,500 |

| 60–63 | $24,500 | +$11,250 | $35,750 |

| 64+ | $24,500 | +$8,000 | $32,500 |

The combined employer and employee contribution limit for 2026 is $72,000 — or $80,000 for employees 50 and older. Asinsight

Roth IRA contribution limits 2026

The IRA contribution limit for 2026 is $7,500 — up from $7,000 in 2025. For savers age 50 and older, the limit increases to $8,600. Practical Ecommerce

| Age group | 2026 Roth IRA limit |

|---|---|

| Under 50 | $7,500 |

| 50 and older | $8,600 |

Note: this $7,500 limit is combined across all your IRAs — traditional and Roth together. You can’t put $7,500 in a Roth and another $7,500 in a traditional IRA in the same year.

Pro Tip: Even if you can’t contribute the maximum, contribute something — consistently. The compounding math (covered in our compound interest guide) makes starting early far more valuable than waiting until you can max out.

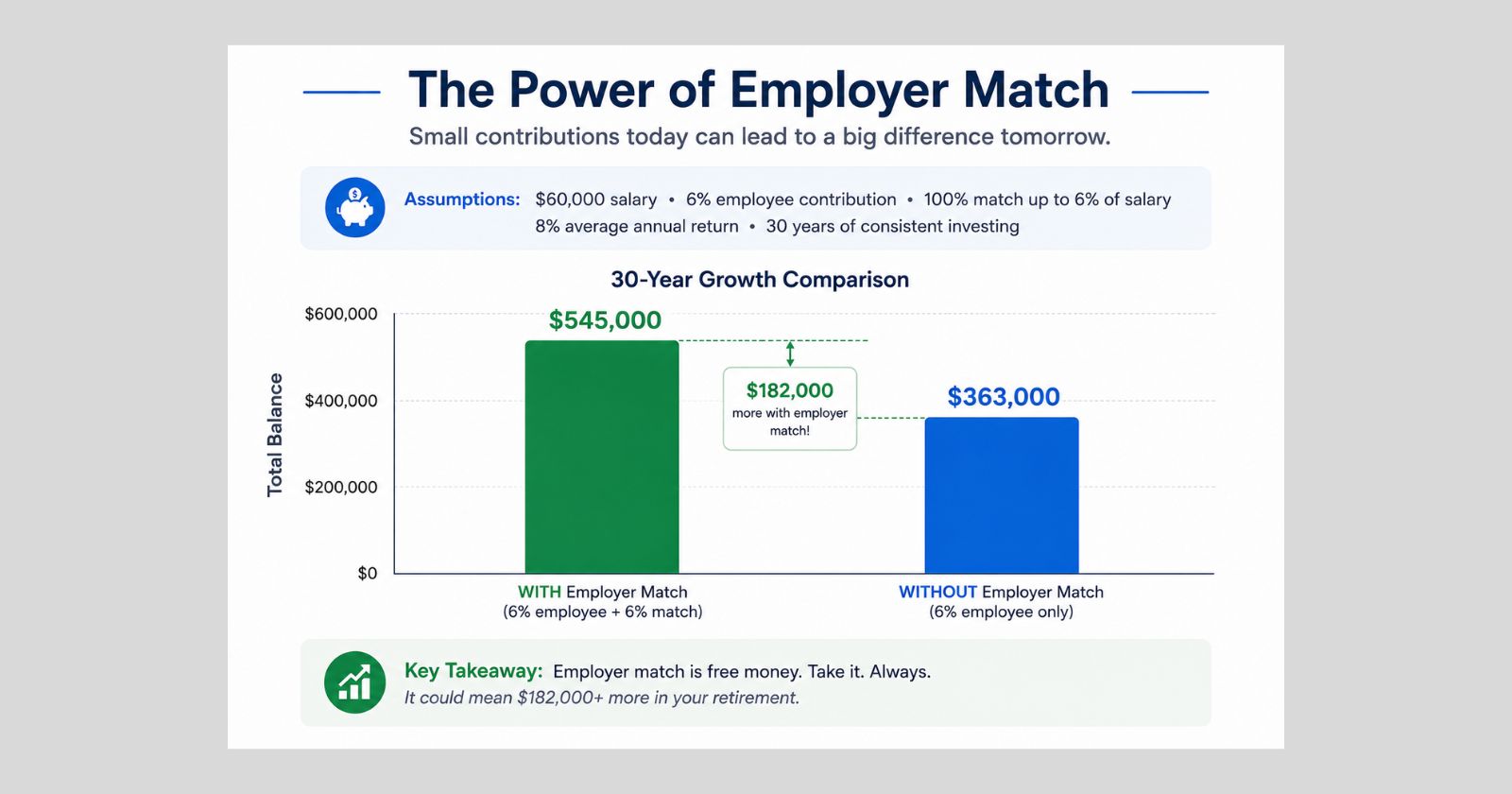

6. The Employer Match: Why Ignoring It Is the Costliest Mistake in Personal Finance

Let’s be direct: the 401(k) employer match is the single best investment available to most American workers. Before any Roth IRA, before any brokerage account, before any other financial move — the employer match comes first.

Here’s why.

The average 401(k) employer match in 2026 is around 4% to 6% of salary. According to a recent study by the US Bureau of Labor Statistics, 41% of companies that offer a 401(k) plan match up to 6% of employees’ salaries. ScienceDirect

What the match actually looks like

The most common structure: your employer matches 50% of your contributions, up to 6% of your salary.

On a $60,000 salary:

- You contribute 6% = $3,600/year

- Your employer adds 50% of that = $1,800/year

- Total going into your account = $5,400/year — for a $3,600 contribution

That’s an instant 50% return on your money before any market growth. No stock, ETF, or savings account anywhere offers that.

The true 30-year cost of ignoring the match

| Scenario | Annual own contribution | Employer match | Total/year | Value at retirement (7% growth, 30 yrs) |

|---|---|---|---|---|

| Gets full match | $3,600 | $1,800 | $5,400 | ~$545,000 |

| Skips match | $3,600 | $0 | $3,600 | ~$363,000 |

| Difference | ~$182,000 |

Missing the employer match for 30 years costs you approximately $182,000 — from the same out-of-pocket contributions. That’s not a rounding error. That’s a life-changing amount of money left on the table.

Employees should always contribute at least enough to receive the full match, since failing to do so means leaving free money on the table. SEOmator

More than 85% of 401(k) plans for which Fidelity is the service provider offer some type of employer contribution. Check your plan documents or ask your HR department — most full-time employees at medium-to-large companies have this benefit. Keywords Everywhere

7. The Vesting Schedule Trap Nobody Warns You About

Here’s the detail that blindsides thousands of employees every year: your employer’s match may not truly be yours yet.

Most 401(k) plans include a vesting schedule — a timeline that determines when you actually own the employer’s contributions. Until you’re fully vested, if you leave the company, you forfeit a portion (or all) of the employer’s contributions.

There are three main types:

| Vesting type | What it means | Example |

|---|---|---|

| Immediate | Match is yours from day one | Best for employees |

| Cliff vesting | 0% until a set date, then 100% | 0% for 2 years, then 100% |

| Graded vesting | Ownership increases gradually | 20% per year over 5 years |

Why this matters: If you’re on a 3-year cliff vesting schedule and you leave after 2 years 11 months, you walk away with $0 of your employer’s contributions. The money sits in the account — but it goes back to the company.

Before leaving any job, check your vesting status. Your HR department or plan documents will show exactly where you stand. Sometimes waiting one more quarter before leaving can be worth thousands of dollars.

8. Roth IRA Income Limits for 2026: Do You Qualify?

The Roth IRA has one major catch: high earners can’t contribute directly.

The income phase-out range for taxpayers making contributions to a Roth IRA is increased to between $153,000 and $168,000 for singles and heads of household for 2026, up from between $150,000 and $165,000 in 2025. For married couples filing jointly, the phase-out range is $242,000 to $252,000. Link Assistant

Here’s how the phase-out works in practice:

| Filing status | Full contribution | Partial contribution | Cannot contribute |

|---|---|---|---|

| Single / Head of household | Under $153,000 | $153,000 – $168,000 | Over $168,000 |

| Married filing jointly | Under $242,000 | $242,000 – $252,000 | Over $252,000 |

| Married filing separately | — | $0 – $10,000 | Over $10,000 |

If your income falls in the partial range, you can still contribute — just less than the full $7,500. The reduction is calculated proportionally across the phase-out range.

What if you earn too much? The Backdoor Roth IRA

If your income is above the limit, you’re not entirely locked out. A strategy called the Backdoor Roth IRA allows high earners to contribute to a traditional IRA (which has no income limits) and then convert it to a Roth. It’s legal, it’s widely used, and it’s worth researching with a financial advisor if you’re in this bracket.

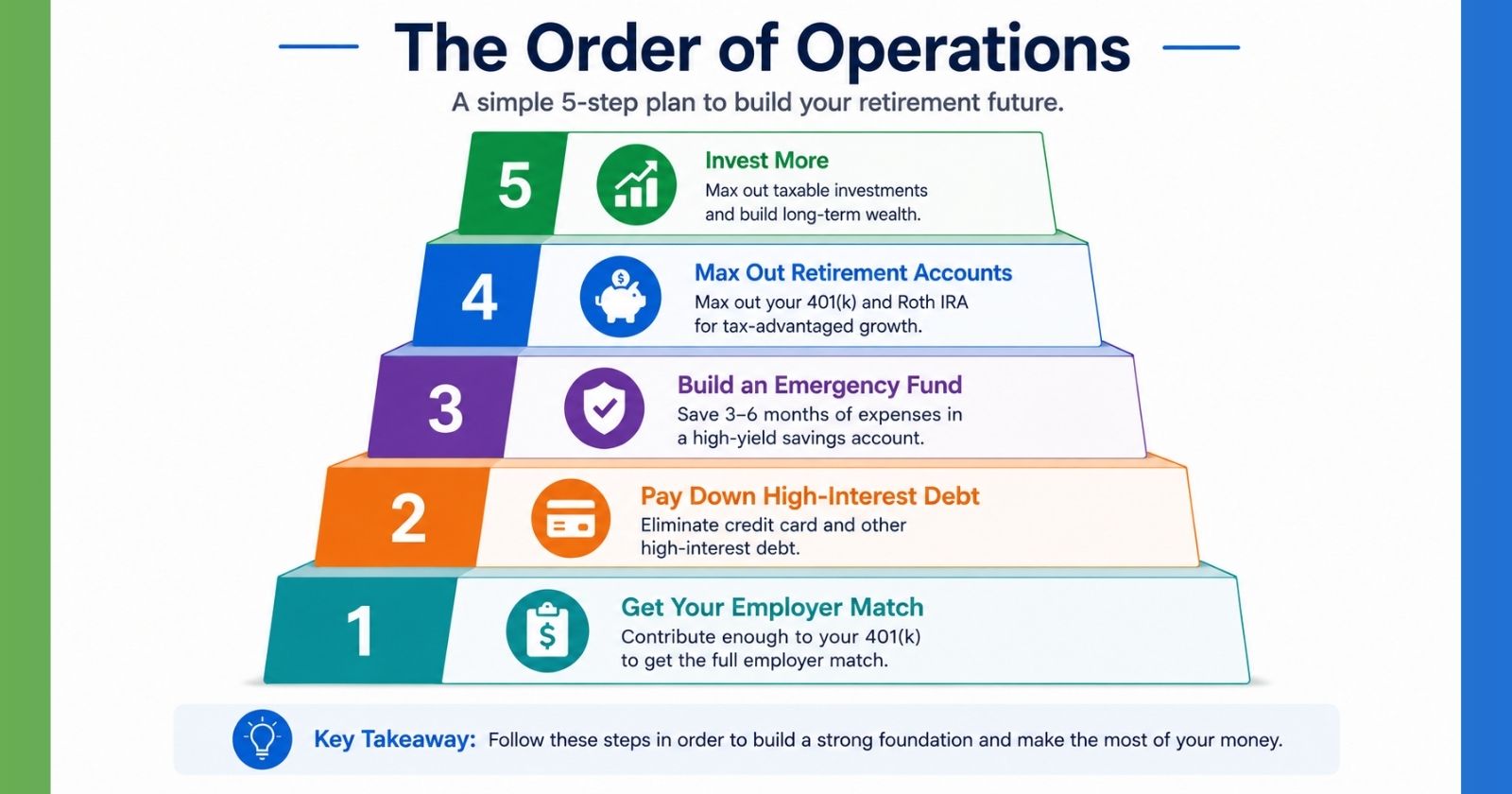

9. The Retirement Savings Order of Operations

This is the section no other beginner article puts together clearly. Here’s the exact sequence — in order — for most Americans in 2026:

Step 1: Contribute to your 401(k) up to the employer match.

This comes before everything else. The most common 401(k) match formula is a dollar-for-dollar match on the first 3% and then 50 cents on the dollar on the next 2% of salary. Find out your employer’s formula and contribute exactly that much — not a dollar less. Accio

Step 2: Pay off any high-interest debt.

Credit card balances at 20–22% APR cost you more than any investment returns you’ll earn. If you’re carrying that kind of debt, throw extra cash at it before Step 3.

Step 3: Open a Roth IRA and max it out ($7,500 in 2026).

If your income is under $153,000 (single) or $242,000 (married), open a Roth IRA at Fidelity, Schwab, or Vanguard and contribute the full $7,500. Invest it in a low-cost S&P 500 index fund. Learn more about choosing the right fund in our guide to Index Funds vs ETFs.

Step 4: Go back and max out your 401(k) ($24,500 in 2026).

If you have money left after maxing your Roth IRA, return to your 401(k) and increase contributions toward the $24,500 annual limit.

Step 5: Open a taxable brokerage account.

Once both accounts are maxed, any additional investing goes into a regular brokerage account — no tax advantages, but no limits either.

| Priority | Account | 2026 limit | Action |

|---|---|---|---|

| 1st | 401(k) up to match | Varies | Always do this first |

| 2nd | Pay off high-interest debt | — | Before more investing |

| 3rd | Roth IRA | $7,500 | Max it out |

| 4th | 401(k) beyond match | Up to $24,500 | If funds remain |

| 5th | Taxable brokerage | Unlimited | After above are maxed |

10. Traditional 401(k) vs Roth 401(k): One More Decision

Many employers now offer both a traditional and a Roth version of the 401(k). Same account, same employer match, same limits — but different tax treatment.

- Traditional 401(k): Contributions are pre-tax. You get a tax break today. You pay taxes on withdrawals in retirement.

- Roth 401(k): Contributions are after-tax. No break today. Withdrawals in retirement are completely tax-free.

Which should you choose?

The standard advice: choose based on whether you expect to be in a higher or lower tax bracket in retirement.

- If you’re young and in a lower tax bracket now → Roth 401(k) makes more sense. Pay the small tax now, enjoy tax-free growth forever.

- If you’re a high earner in your peak earning years → Traditional 401(k) may make more sense. Reduce your tax bill now, pay it later when income may be lower.

For most people in their 20s and early 30s, the Roth 401(k) — or at minimum the Roth IRA — is the better long-term choice, purely because of the power of decades of tax-free compound growth.

Pro Tip: If your employer offers a Roth 401(k), you can contribute to it AND a Roth IRA in the same year — as long as you stay within each account’s individual limits. This gives you a potential $32,000 in after-tax retirement contributions in 2026 ($24,500 + $7,500).

11. Can You Have Both a Roth IRA and a 401(k)?

Yes — and for most people with the budget to do it, having both is the optimal strategy.

You can have both a 401(k) and a Roth IRA and contribute to both in a given year, as long as you follow the contribution limits for each. They are two different and often complementary ways of saving for retirement. Semrush

Here’s what holding both gives you:

- Tax diversification: Some money grows pre-tax (traditional 401(k)), some grows tax-free (Roth IRA). In retirement, you can draw strategically from each to manage your tax bracket.

- Flexibility: The Roth IRA’s contribution withdrawal rules (available penalty-free anytime) give you emergency access if needed. The 401(k)’s higher limits let you shelter more income.

- Investment breadth: Your 401(k) invests in your employer’s fund menu. Your Roth IRA gives you access to every ETF, index fund, and stock on the market.

If you can only do one right now, follow the order of operations above. If you can do both — do both.

For more everyday money guides, browse InfoBrave’s Informative section — and check out InfoBrave for practical guides on finance, tech, and lifestyle.

12. Frequently Asked Questions

Should I open a Roth IRA or 401(k) first?

Contribute to your 401(k) first — but only up to your employer match. That match is an instant 50–100% return on your money that no other investment can match. After capturing the full match, open a Roth IRA and max it out ($7,500 in 2026 if you’re under 50). Then return to your 401(k) if you have more to invest.

What are the 401(k) and Roth IRA contribution limits for 2026?

The 401(k) contribution limit for 2026 is $24,500 for employees under 50, with an additional $8,000 catch-up for those 50 and older. The Roth IRA limit is $7,500 for those under 50 and $8,600 for those 50 and older. These are IRS-confirmed figures effective for the 2026 tax year. Google SupportPractical Ecommerce

Can I contribute to both a Roth IRA and a 401(k) in the same year?

Yes. The 401(k) limit and the Roth IRA limit are completely separate. You can contribute the full $24,500 to your 401(k) and the full $7,500 to your Roth IRA in the same year — for a combined $32,000 in tax-advantaged contributions in 2026.

What is the Roth IRA income limit for 2026?

For 2026, single filers can make full Roth IRA contributions if their MAGI is under $153,000, with contributions phasing out between $153,000 and $168,000. Married couples filing jointly can contribute fully if their MAGI is under $242,000, with phase-out between $242,000 and $252,000. Link Assistant

What happens to my 401(k) if I leave my job?

Your contributions are always yours. Your employer’s matched contributions depend on your vesting schedule — you may forfeit some or all if you haven’t been employed long enough. When you leave, you can roll your 401(k) into your new employer’s plan or into a traditional IRA, usually without taxes or penalties.

Is a Roth IRA better than a 401(k)?

Neither is universally better — they serve different purposes. The 401(k) offers higher contribution limits and potential employer matching. The Roth IRA offers tax-free growth, more investment choices, and greater withdrawal flexibility. For most Americans, the optimal strategy is to use both: capture the 401(k) match first, then max the Roth IRA, then add more to the 401(k).

What if my employer doesn’t offer a 401(k)?

Open a Roth IRA immediately — it becomes your primary retirement account. You can contribute up to $7,500 in 2026. If you’re self-employed, also look into a SEP-IRA or Solo 401(k), which have much higher contribution limits ($69,000+ in 2026) designed specifically for self-employed individuals.

What is a vesting schedule and why does it matter?

A vesting schedule determines when your employer’s matching contributions actually belong to you. If you leave before you’re fully vested, you forfeit the employer’s contributions. Immediate vesting means the match is yours from day one. Cliff vesting means 0% until a specific date, then 100%. Graded vesting increases your ownership percentage annually. Always check your vesting status before leaving a job — it can mean thousands of dollars.

Also read: What Is Compound Interest? The Simple Guide That Makes It Finally Click (2026)