You’ve heard the phrase a hundred times. You’ve nodded along when someone mentions it. But if someone asked you right now to explain exactly what compound interest is and show why it matters, could you do it?

Most people can’t — and that gap quietly costs them tens of thousands of dollars (or pounds) over their lifetime.

Here’s the good news: compound interest is not complicated. It’s one of those concepts that sounds technical but takes about five minutes to genuinely understand. And once it clicks, it changes the way you think about money forever.

In this guide you’ll get the clearest plain-English explanation of compound interest available in 2026 — with real numbers, real examples, a growth table for both USA and UK investors, and an honest look at how compounding works against you in debt. No formulas until you’re ready for them.

1. The One-Sentence Answer

Compound interest is earning interest on your interest — not just on your original money.

That’s it. That’s the whole concept. Everything else in this article is just showing you why that one sentence is so powerful.

2. Simple Interest vs Compound Interest: The Real Difference

Before compound interest makes sense, you need to see what it’s not.

Simple interest is interest calculated only on your original amount — called the principal. Every year, the same fixed amount gets added. It’s predictable, it’s flat, and it’s boring.

Compound interest is calculated on your original amount plus all the interest you’ve already earned. Every year, the base gets bigger — which means the interest gets bigger — which means the next year’s base gets bigger still.

Let’s put real numbers to it. Say you invest $1,000 at 10% interest for 3 years.

| Year | Simple Interest | Compound Interest |

|---|---|---|

| Start | $1,000 | $1,000 |

| Year 1 | $1,100 (+$100) | $1,100 (+$100) |

| Year 2 | $1,200 (+$100) | $1,210 (+$110) |

| Year 3 | $1,300 (+$100) | $1,331 (+$121) |

| Difference | $1,300 total | $1,331 total |

After just 3 years, the difference is $31. That sounds small. But hold on — we’re about to stretch that out to 30 years and watch your jaw drop.

Pro Tip: Simple interest barely exists in the real world. Savings accounts, investment funds, mortgages, and credit cards all use compound interest. Understanding it isn’t optional — it’s the foundation of every major financial decision you’ll ever make.

3. How Compound Interest Actually Works (Step by Step)

Here’s the process in plain steps, no jargon:

- You invest a starting amount — let’s say $5,000

- It earns interest — say 7% in year one, so you earn $350

- That interest gets added to your total — you now have $5,350

- Next year, you earn 7% on $5,350 — not just on the original $5,000

- That gives you $374.50 — $24.50 more than the year before

- Repeat for 20, 30, or 40 years — and the numbers become extraordinary

The formula for compound interest is:

A = P(1 + r/n)^(nt)

Where:

- A = the final amount

- P = principal (your starting money)

- r = annual interest rate (as a decimal — so 7% = 0.07)

- n = number of times interest compounds per year

- t = time in years

Don’t let the formula scare you. The key inputs are simple: more money + higher rate + more time = dramatically more wealth. Of those three, time is the one most people underestimate.

4. The Snowball Analogy — Warren Buffett’s Own Words

Warren Buffett — widely considered the greatest investor of all time — describes compound interest in the most visual way possible. Buffett explains its power in his autobiography as a snowball rolling down a long hill, picking up more snow as it gains momentum until it becomes a massive snowball. Google Support

That’s exactly right. At the top of the hill, your snowball is tiny. The first few rolls barely seem to matter. But as it gathers more snow, each revolution adds more snow than the last — and by the time it reaches the bottom, what started as a handful of powder has become something enormous.

The two things that make the snowball grow are:

- The size of the snowball (how much money you start with and add)

- The length of the hill (how long you let it compound)

Over 99% of Warren Buffett’s wealth was accumulated after his 50th birthday, illustrating how compounding dramatically accelerates in later years. He started investing at age 11 — but the real explosion happened after decades of compounding had stacked up. Keywords Everywhere

The lesson? Start early. The hill needs to be long.

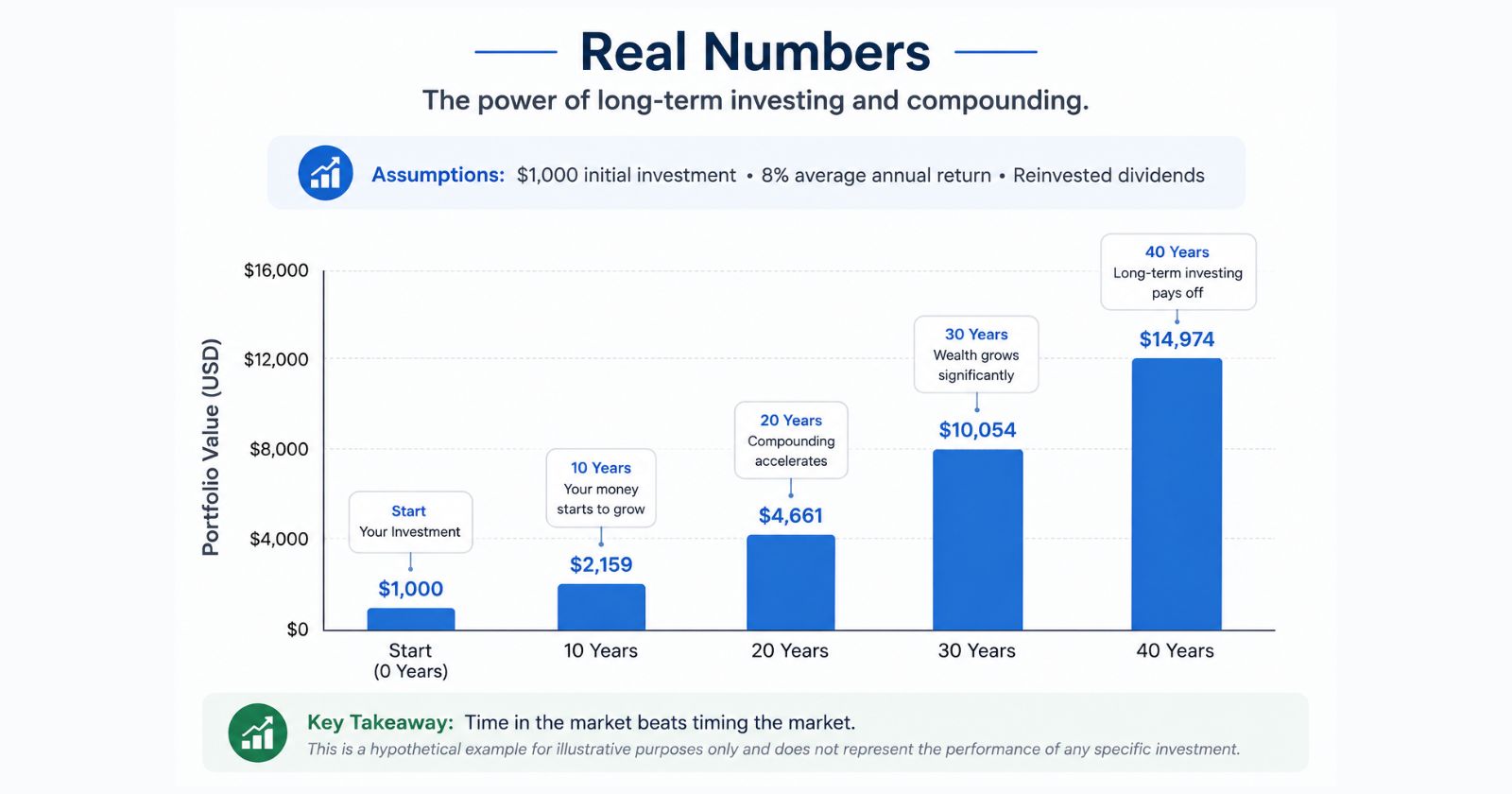

5. Real Numbers: What $1,000 / £1,000 Actually Grows Into

This is the section that makes compound interest click for most people. Let’s use a realistic 7% annual return — close to the S&P 500’s long-run average after inflation.

USA Example: $1,000 invested at 7% annually

| Years | Value |

|---|---|

| 5 years | $1,403 |

| 10 years | $1,967 |

| 15 years | $2,759 |

| 20 years | $3,870 |

| 30 years | $7,612 |

| 40 years | $14,974 |

One thousand dollars becomes nearly fifteen thousand without you touching it. You added zero extra money. Time did all the work.

UK Example: £1,000 invested at 7% annually

| Years | Value |

|---|---|

| 5 years | £1,403 |

| 10 years | £1,967 |

| 20 years | £3,870 |

| 30 years | £7,612 |

| 40 years | £14,974 |

The numbers are identical — the compounding formula doesn’t care about currency.

Now add regular contributions

Watch what happens when you invest $200 / £200 per month at the same 7% rate:

| Years | Total Contributed | Final Value |

|---|---|---|

| 10 years | $24,000 | $34,613 |

| 20 years | $48,000 | $104,185 |

| 30 years | $72,000 | $243,994 |

| 40 years | $96,000 | $528,226 |

You put in $96,000 over 40 years. You end up with $528,226. The extra $432,226 came entirely from compound interest. The longer an investment compounds, the greater the growth — $100,000 invested for 20 years at a 3.2% higher annual rate results in a difference of nearly $167,000 due to compounding alone. Slow Living Kitchen

The age comparison that changes everything

If an individual saves £100 a month from age 30 to 60 at 10% annual interest, they accumulate £217,132. But if they save £100 a month from age 20 to 30 only — then stop entirely — and leave that money until age 60, they end up with more: £253,680. FlavoristaLuna

Read that again. Ten years of investing in your 20s beats thirty years of investing starting in your 30s — with the same total contributions. That’s the power of starting early. Time in the market isn’t a factor. It’s the factor.

6. The Rule of 72: The Mental Math Trick Every Investor Should Know

Here’s a tool you can use in your head, right now, with no calculator.

The Rule of 72 tells you how many years it takes to double your money at any given interest rate. Just divide 72 by your annual return:

Years to double = 72 ÷ interest rate

| Interest Rate | Years to Double |

|---|---|

| 2% (savings account) | 36 years |

| 4% (bonds / Cash ISA) | 18 years |

| 6% (balanced fund) | 12 years |

| 8% (stock market) | 9 years |

| 10% (aggressive growth) | 7.2 years |

| 12% | 6 years |

So at 8%, your money doubles roughly every 9 years. Invest $10,000 at 25. By 34, it’s $20,000. By 43, it’s $40,000. By 52, it’s $80,000. By 61, it’s $160,000 — from a single $10,000 investment made at 25, without adding another penny.

Pro Tip: Use the Rule of 72 to instantly evaluate any investment or savings account. A 2% savings account? Your money takes 36 years to double. A 0.1% current account? 720 years. That’s why where you keep your money matters almost as much as how much you have.

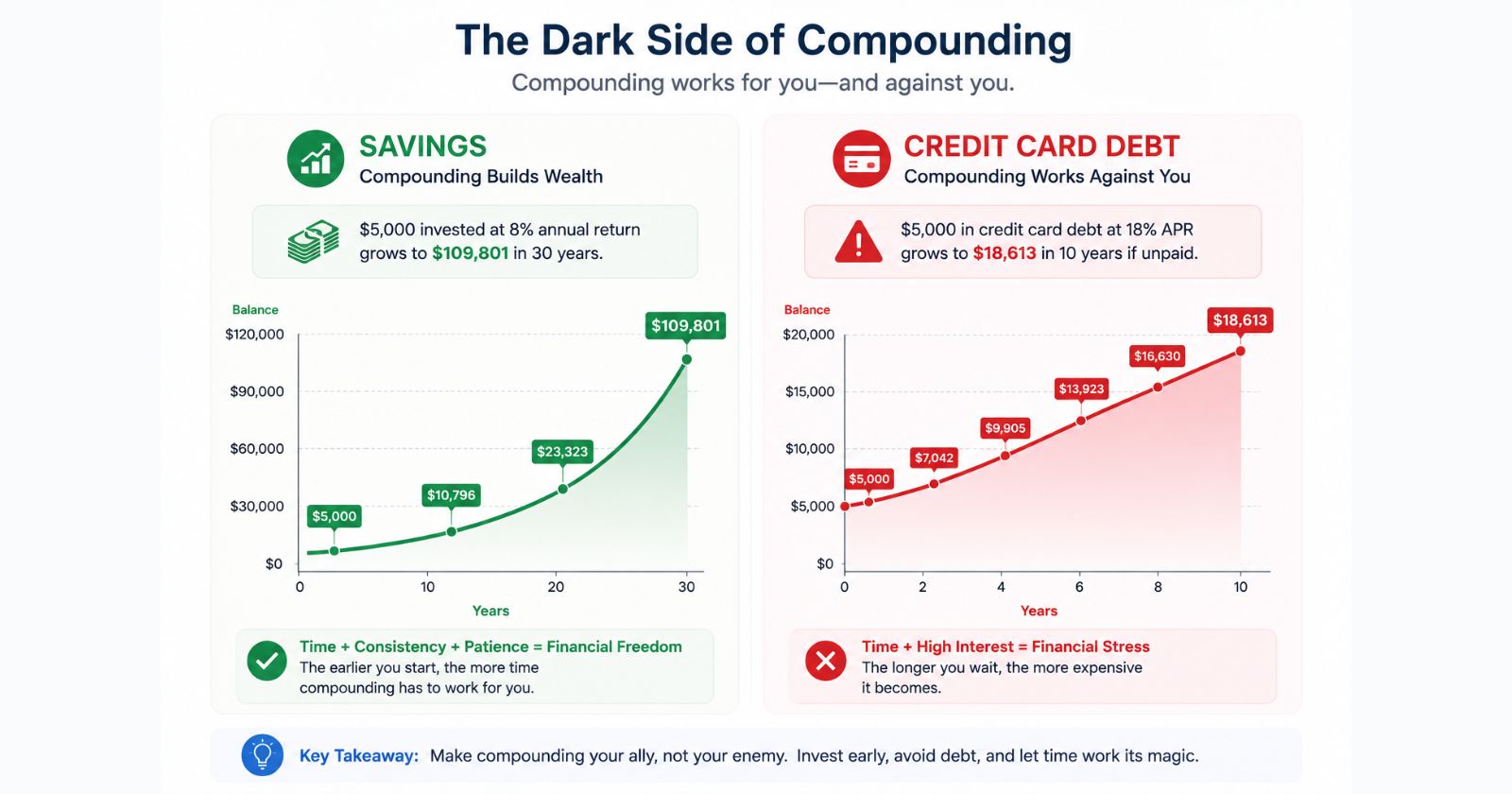

7. Compound Interest Working Against You — The Dark Side Nobody Talks About

Every article about compound interest focuses on saving and investing. Almost none of them spend equal time on the other side of compounding — the side that’s actively working against millions of people right now.

When you carry debt — especially high-interest debt like credit cards — compound interest is your enemy. And it uses exactly the same math against you.

The credit card trap

The average American credit card charges around 20–24% APR in 2026. Let’s say you carry a $3,000 balance and only make minimum payments.

A loan with a 10% interest rate compounding semi-annually means you pay interest on interest — effectively paying more than the stated rate over time. Now multiply that effect across a 20%+ credit card rate. Semrush

| Scenario | Balance | APR | Minimum payment | Total paid | Time to clear |

|---|---|---|---|---|---|

| Credit card | $3,000 | 22% | ~$60/month | ~$6,800+ | 15+ years |

| Paid off in 12 months | $3,000 | 22% | $279/month | ~$3,348 | 1 year |

The same $3,000 debt costs you either $348 in interest (if cleared in a year) or $3,800+ in interest (if you only pay minimums). Compounding turned a manageable debt into a years-long drain.

Student loans and mortgages

The same principle applies to any loan where interest compounds and you’re making small or deferred payments. In the UK, student loan interest compounds annually on an already large balance. In the USA, private student loans often compound daily.

The takeaway: compound interest is completely neutral. It works exactly the same way whether it’s building your wealth or growing your debt. Understanding it tells you exactly where to put your money — and exactly what to pay off first.

8. How Compounding Frequency Changes Everything

Here’s a detail most beginner guides gloss over: compound interest doesn’t always compound once a year. The frequency of compounding changes the outcome — sometimes significantly.

| Compounding frequency | What it means | Effect on $10,000 at 5% for 10 years |

|---|---|---|

| Annually | Interest added once a year | $16,289 |

| Quarterly | Interest added 4× a year | $16,436 |

| Monthly | Interest added 12× a year | $16,470 |

| Daily | Interest added 365× a year | $16,487 |

High-yield savings accounts pay 4.00–4.35% APY in 2026 — but that’s the gross rate. After federal taxes, a 4.35% taxable return drops to roughly 3.25% after federal taxes, while a tax-free account keeps every dollar compounding. Organic Facts

Most investment accounts (stocks, ETFs, index funds) compound continuously as dividends reinvest and prices compound. Most savings accounts and CDs compound monthly or daily.

The practical takeaway: when comparing savings accounts, always look at the APY (Annual Percentage Yield) — not just the interest rate. APY already accounts for compounding frequency, so it’s the true apples-to-apples number.

9. How to Start Letting Compound Interest Work for You Today

You don’t need a lot of money. You need to start. Here’s the exact playbook:

Step 1 — Clear your high-interest debt first.

Compound interest working against you at 20% APR will always outpace compound interest working for you at 7%. Pay off credit cards before investing.

Step 2 — Open a tax-advantaged account.

- 🇺🇸 USA: Open a Roth IRA or contribute to your 401(k). Both let compound interest grow completely tax-free or tax-deferred. Learn how in our guide to Index Funds vs ETFs.

- 🇬🇧 UK: Open a Stocks and Shares ISA. Up to £20,000 per tax year grows completely free from income tax and capital gains tax.

Step 3 — Invest in a low-cost index fund.

Put your money in a broad market index fund (S&P 500 for USA investors, FTSE Global All Cap for UK investors). These have returned roughly 7–10% annually over the long run, which is what all the numbers in this guide assume.

Step 4 — Set up automatic monthly contributions.

Automation removes emotion and builds the habit. Even $50 or £50 a month, started in your 20s, becomes meaningful wealth by retirement. Automation also means you dollar-cost average automatically — buying more shares when prices are low, fewer when they’re high.

Step 5 — Do nothing. Seriously.

The temptation to check, react, and tinker is the enemy of compounding. Every time you sell, you interrupt the snowball. The most powerful move in investing is also the hardest: leave it alone and let time do the work.

For more practical investing and personal finance guides, head to InfoBrave’s Informative section — and check out InfoBrave for more everyday guides on money, tech, and lifestyle.

10. The Einstein Quote — And the Truth Behind It

You’ve probably seen this one everywhere:

“Compound interest is the eighth wonder of the world. He who understands it, earns it — he who doesn’t, pays it.”

It’s almost always attributed to Albert Einstein. Here’s the thing: researchers at Quote Investigator have found no verified evidence that Einstein ever actually said or wrote these words. The earliest known appearance of the quote in print dates to 1983 — nearly three decades after Einstein’s death in 1955. Keywords Everywhere

So why mention it? Because it’s a perfect example of how a great idea gets a famous name attached to it to make it sound more credible. The quote might be misattributed — but the math is completely real. Compound interest genuinely is one of the most powerful forces in personal finance, regardless of who first said so.

The people who actually prove it? Investors who started early, stayed consistent, and let decades of compounding do the heavy lifting. Warren Buffett is the most famous example — but there are millions of ordinary people with ordinary incomes who retired comfortably by simply understanding and applying this one idea.

Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice. Always conduct your own research and, where appropriate, consult a qualified financial adviser before making investment decisions. Capital is at risk when investing.

11. Frequently Asked Questions

What is compound interest in simple terms?

Compound interest means you earn interest on both your original money and on the interest you’ve already earned. Instead of growing in a straight line, your money grows exponentially — accelerating faster the longer you leave it. A £1,000 investment earning 7% a year doesn’t just add £70 every year — it adds more each year as the total grows.

What is the difference between simple and compound interest?

Simple interest is calculated only on your original principal — the same fixed amount every year. Compound interest is calculated on your principal plus all accumulated interest, so the amount grows larger each period. Over long time periods, the difference between the two is enormous.

Is compound interest good or bad?

It’s both, depending on which side of it you’re on. When you’re saving or investing, compound interest works powerfully in your favour — your wealth grows exponentially over time. When you’re in debt, especially high-interest debt like credit cards, compound interest works against you — your balance grows exponentially if you only make minimum payments.

What is the Rule of 72?

The Rule of 72 is a quick mental math shortcut to estimate how long it takes to double your money. Divide 72 by your annual interest rate. At 8% annual return, your money doubles in roughly 9 years (72 ÷ 8 = 9). At 4%, it takes 18 years. At 2%, it takes 36 years.

How much does $1,000 / £1,000 grow with compound interest?

At 7% annual return: after 10 years it becomes roughly $1,967. After 20 years, $3,870. After 30 years, $7,612. After 40 years, $14,974. The key is time — the longer you leave it, the more dramatically it grows, because each year’s interest forms the base for the next.

When does compound interest compound — daily, monthly, or yearly?

It depends on the account. Most high-yield savings accounts and CDs compound daily or monthly. Investment funds compound continuously as dividends reinvest. When comparing accounts, look at the APY (Annual Percentage Yield) rather than the headline interest rate — APY already accounts for compounding frequency and gives you the true annual return.

Is compound interest the same as APY?

Not exactly, but they’re closely related. APY (Annual Percentage Yield) is the effective annual rate you actually earn after compounding is factored in. It’s always equal to or higher than the stated interest rate. For example, a savings account advertising 4% compounded monthly actually delivers a 4.07% APY. Always compare APYs when choosing accounts.

You may also like: Index Funds vs ETFs: Which Is Better for Beginners in 2026?