If you live in the UK and you’re trying to invest your money in the most tax-efficient way possible, two accounts will keep coming up: the ISA and the SIPP. Both are genuinely powerful. Both shelter your money from tax. And both are widely misunderstood by people who could benefit from them enormously.

The internet is full of articles that explain what each account is — but very few clearly tell you which one to open first, which one suits your situation, and what the critical 2026 rule changes mean for your planning.

This guide does exactly that. You’ll get the plain-English breakdown of both accounts, verified 2026/27 limits, real-pounds tax relief calculations, an honest look at the major rule change coming in April 2027, and a clear decision framework by situation. No jargon beyond what’s necessary.

Important Disclaimer: This article is for informational and educational purposes only. It does not constitute financial or tax advice. Tax rules can and do change. Always consult a qualified, regulated financial adviser before making investment decisions. Capital is at risk when investing.

1. The One-Line Answer

If your employer offers a pension match — contribute to that first.

Then: SIPP for the tax relief if you’re a higher-rate taxpayer. ISA for flexibility if you might need the money before 57.

Best answer for most people: both, in that order.

Everything below explains the reasoning in full.

2. What Is a Stocks and Shares ISA?

An ISA — Individual Savings Account — is a tax-free wrapper you put around your investments. You contribute money you’ve already paid income tax on, and in return, everything that happens inside the account is completely sheltered from tax: no capital gains tax on growth, no income tax on dividends, no tax on withdrawals. Ever.

The Stocks and Shares ISA specifically lets you invest in funds, ETFs, shares, bonds, and investment trusts — not just cash. Think of it as a normal brokerage account with a permanent tax shield over it.

Key features of an ISA:

- Contribute up to £20,000 per tax year (2026/27)

- All growth is free from Capital Gains Tax and income tax

- Withdraw your money at any age, any time — no restrictions

- You choose the investments — stocks, index funds, ETFs, bonds

- No tax relief on the way in — you contribute from post-tax income

- Withdrawals do not count as income for any tax purpose — including Universal Credit or student loan repayments

The ISA is the bedrock of UK personal finance. You can invest up to £20,000 per tax year across all ISA types combined, and everything inside grows completely free of capital gains tax and income tax. Withdrawals are also tax-free — and crucially, withdrawals do not count as income for any purpose, including means-tested benefits or student loan repayments. FlavoristaLuna

The ISA’s superpower is flexibility. There are no rules about when you can access your money. Retire at 45? Draw from your ISA. Need the money in an emergency at 38? Draw from your ISA. No penalties, no questions, no tax.

3. What Is a SIPP?

A SIPP — Self-Invested Personal Pension — is a pension you manage yourself. Unlike a standard workplace pension where your employer picks the investment options, a SIPP gives you complete control over what you invest in, from individual shares and global ETFs to bonds and commercial property.

The defining feature of a SIPP is tax relief on contributions. When you put money in, HMRC automatically adds basic-rate tax relief on top — and higher and additional rate taxpayers can claim even more back through Self Assessment.

The tax relief on SIPP contributions is one of the most powerful wealth-building tools available in the UK. Every £80 a basic-rate taxpayer contributes becomes £100 inside the pension, with HMRC automatically adding the 20% top-up. Higher and additional rate taxpayers can claim even more through Self Assessment — effectively turning a £55–£60 personal cost into £100 of pension savings. Link Assistant

Key features of a SIPP:

- Contribute up to £60,000 per year (or 100% of UK earnings if lower)

- Significant upfront tax relief — 20%, 40%, or 45% depending on your tax band

- Investments grow free from Capital Gains Tax and income tax inside the pension

- Currently accessible from age 55 — rising to 57 from April 2028

- Up to 25% can be taken tax-free at retirement (your “tax-free lump sum”)

- Remaining withdrawals are taxed as income in retirement

- Can carry forward unused allowance from the previous three tax years

Pro Tip: A SIPP is not just for the self-employed. Any UK resident under 75 with UK earnings can open one — including employees who also have a workplace pension. You can hold both at the same time.

4. ISA vs SIPP: Head-to-Head Comparison

| Feature | Stocks & Shares ISA | SIPP |

|---|---|---|

| Annual allowance 2026/27 | £20,000 | £60,000 (or 100% of earnings) |

| Tax on contributions | None (post-tax money in) | Tax relief added by HMRC |

| Growth inside account | Tax-free | Tax-free |

| Tax on withdrawal | None — ever | Yes, as income (after 25% tax-free lump) |

| Access age | Any age, any time | Age 55 now (rising to 57 in April 2028) |

| Employer contributions | No | Yes (via workplace pension / SIPP) |

| Investment choice | Stocks, ETFs, funds, bonds | Stocks, ETFs, funds, bonds, commercial property |

| Inheritance tax | Part of your estate (IHT applies) | Currently outside estate — changing April 2027 |

| Income limits | None | Must have UK earnings (or £3,600 minimum) |

| Carry forward unused allowance | No | Yes — up to 3 previous tax years |

| Best for | Flexibility, accessibility, all ages | Retirement savings, tax relief, higher earners |

5. The 2026/27 Allowances: Exact Numbers

The standard ISA allowance is £20,000 for 2026/27. The SIPP annual allowance is £60,000 — or 100% of earnings if lower. Many UK savers use both products together rather than choosing one over the other. Grow Forage Cook Ferment

ISA allowance breakdown

| ISA type | 2026/27 allowance | Notes |

|---|---|---|

| Stocks and Shares ISA | Up to £20,000 | Best for investing |

| Cash ISA | Up to £20,000 | Allowance shared across all ISA types |

| Lifetime ISA (LISA) | Up to £4,000 | Counts toward the £20,000 total; 25% bonus |

| Junior ISA | £9,000 (per child) | Separate from adult allowance |

The £20,000 ISA allowance is the combined total across all your ISAs in a single tax year. You cannot, for example, put £20,000 into a Stocks and Shares ISA and another £20,000 into a Cash ISA in the same tax year.

SIPP contribution limits

You can contribute up to 100% of your relevant UK earnings into pensions each year, subject to an overall annual limit of £60,000. This limit includes both personal and employer contributions. MasterClass

| Scenario | Maximum annual contribution |

|---|---|

| Standard (under 60) | £60,000 or 100% of UK earnings |

| Non-earner / very low earner | £3,600 gross (you pay £2,880, HMRC adds £720) |

| Using carry forward | Up to £120,000+ (prior years’ unused allowance) |

One major SIPP advantage over the ISA: if you didn’t use your full allowance in the past three tax years, you can carry it forward and contribute more than £60,000 in a single year. The ISA offers no such benefit — unused allowance is simply lost at the end of the tax year.

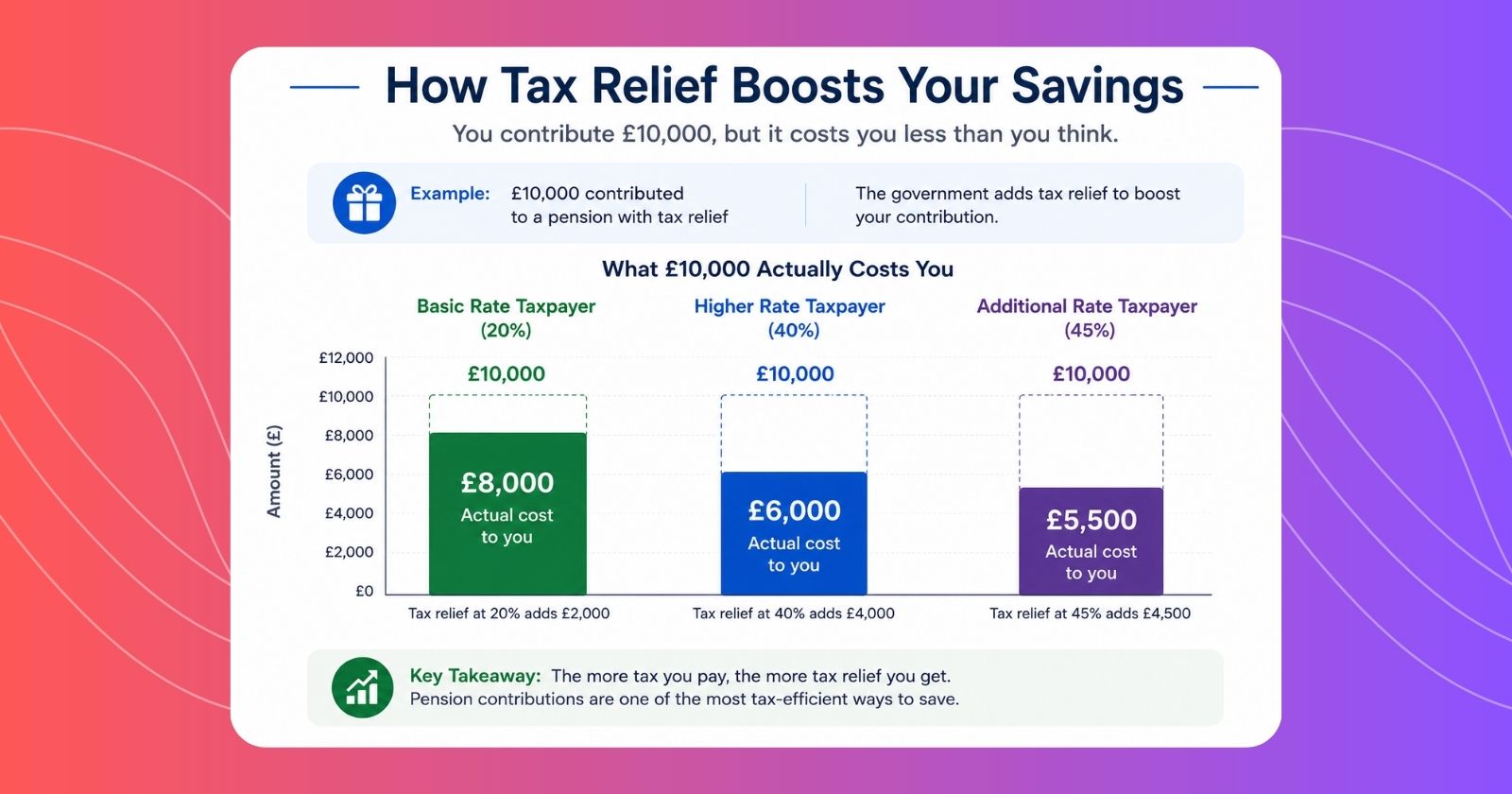

6. SIPP Tax Relief: The Real Pounds You Get Back

This is the section that makes most people rethink how much they’re leaving on the table.

The relief is equal to your marginal income tax rate — so basic rate taxpayers get 20% relief, higher rate taxpayers get 40%, and additional rate taxpayers get 45%. Semrush

Here’s what that actually means in pounds, for a £10,000 gross pension contribution:

| Tax band | Income threshold | Your actual cost | HMRC adds | Gross in pension |

|---|---|---|---|---|

| Basic rate (20%) | Up to £50,270 | £8,000 | £2,000 | £10,000 |

| Higher rate (40%) | £50,270–£125,140 | £6,000 | £4,000 | £10,000 |

| Additional rate (45%) | Over £125,140 | £5,500 | £4,500 | £10,000 |

The 40% tax relief makes the effective SIPP contribution cost 60p for every £1 gross. If the same money were invested in an ISA instead, the full £1 must come from post-tax income with no uplift. Semrush

To put this in sharp relief: a higher-rate taxpayer who contributes £6,000 of their own money ends up with £10,000 working for them inside the pension. That’s a 67% instant return on their contribution — before the investments have earned a single penny.

For example, if you pay £80 into your SIPP, it will be topped up with 20% tax relief. This turns your contribution into £100 in your pension. Essentially, every 80p you pay in is topped up to £1. Google Support

The ISA offers nothing like this. Your £8,000 contribution is simply £8,000. The SIPP’s tax relief is by far its biggest advantage — and the primary reason higher-rate taxpayers should almost always prioritise it.

7. The Flexibility Gap: When Can You Actually Access Your Money?

This is where the ISA wins decisively — and it’s the most important practical difference for most people.

ISA: No restrictions whatsoever. You can withdraw money the day after you invest it, at age 25 or age 75. There are no penalties, no tax charges, and no minimum age.

SIPP: Currently locked until age 55. From April 2028, that minimum access age rises to 57. Accessing your SIPP before the minimum pension age triggers a punishing 55% unauthorised payment tax charge from HMRC — essentially eliminating any benefit of having saved there at all.

This single difference changes the ISA vs SIPP decision significantly depending on your situation:

- If you’re saving for retirement and won’t touch it until 57+: The SIPP’s tax relief advantage dominates.

- If you might need flexibility before 57 — buying a house, career change, early semi-retirement: the ISA’s immediate accessibility is crucial.

- If you’re planning to retire early (before 57): You need ISA savings as a bridge. See the next section.

Pro Tip: The pension age rising from 55 to 57 in April 2028 is not just future news — if you’re planning any kind of early retirement or semi-retirement in the next two years, this change could directly affect your plans. Check your timeline now.

8. The April 2027 Inheritance Tax Change Nobody Is Talking About

This is the content gap almost no beginner article addresses — and it’s potentially the most significant change to UK retirement planning in a decade.

The current rule: SIPP funds passed on at death are currently outside your estate for Inheritance Tax (IHT) purposes. If you die before age 75, your beneficiaries inherit the entire pension pot tax-free. This made SIPPs one of the most powerful estate planning tools in the UK — many people deliberately left their pension untouched, living off ISA and other savings, specifically to pass the pension on tax-free.

The April 2027 change: From 6 April 2027, most unused pension funds will also be brought into the estate for IHT (40%), potentially creating an effective combined rate of 67%+ for higher-rate-taxpayer beneficiaries of post-75 SIPP holders. ALM Corp

As a result, inherited pensions could be subject to “double taxation” — creating an effective tax rate of 52% for pots passed on to basic rate taxpayers, rising to 64% and 67% for higher and additional rate taxpayers respectively. Practical Ecommerce

What this means practically:

| Death scenario | Current rule | From April 2027 |

|---|---|---|

| Die before 75 | Entire pot tax-free to beneficiaries | IHT applies on pot (40%) |

| Die after 75 | Beneficiary pays income tax on withdrawal | IHT (40%) + income tax on withdrawal |

Who this affects most: People with large SIPP pots who were planning to leave pension wealth to children or grandchildren as part of their estate. If your estate — now including your pension — exceeds the nil-rate band (£325,000, or up to £500,000 with the residence nil-rate band), IHT will apply.

What to do: If estate planning is a significant consideration for you, this change means the ISA becomes relatively more attractive as a wealth transfer vehicle from April 2027 — ISA assets remain within your estate (subject to IHT), but at least they’re only taxed once. This is a complex area that genuinely warrants regulated financial advice.

9. The ISA Bridge: The Early Retirement Strategy

This is the strategy that most articles completely ignore — but it’s critical for anyone considering retiring or semi-retiring before 57.

Because the SIPP is locked until 57 (from 2028), anyone who wants to stop full-time work earlier faces a gap: their pension savings are inaccessible, but they need income. The solution is to build ISA savings large enough to bridge that gap — funding your living expenses from the ISA until your SIPP becomes accessible.

A sophisticated drawdown strategy might draw a small amount from the pension each year to keep within the personal allowance, supplementing with ISA withdrawals as needed. This maximises the tax-free pension allowance over time and can result in very low effective tax rates throughout retirement — often below 5% on total income. FlavoristaLuna

A simple example:

Sarah, 48, wants to retire at 52. She has:

- A SIPP worth £280,000 (inaccessible until age 57)

- An ISA worth £120,000

She needs £24,000 per year to live on. Her ISA funds her for 5 years (ages 52–57), at which point she accesses her SIPP. She retires 13 years early — possible only because she built both accounts simultaneously.

The lesson: If early retirement is even a possibility, you need ISA savings as a bridge. Putting everything into a SIPP because the tax relief looks attractive today can leave you pension-rich but cash-poor in your 50s.

10. Who Should Choose What: Scenario-by-Scenario

Scenario 1: Basic-rate taxpayer in their 20s or 30s

Best approach: ISA first, then SIPP.

The 20% tax relief on a SIPP is helpful but not dramatic enough to sacrifice flexibility at this life stage. Prioritise the ISA for accessible savings and the flexibility to use money for a house, career change, or life event before 57. Contribute to your workplace pension up to the employer match first.

Scenario 2: Higher-rate taxpayer (earning £50,270+)

Best approach: SIPP first (beyond employer match), then ISA.

For most UK higher-rate taxpayers with no immediate need for flexible access, the SIPP should be filled before the ISA. A higher-rate taxpayer contributing £10,000 net to a SIPP receives £6,667 in tax relief, making the gross contribution £16,667, with the effective net cost £6,000 after claiming higher-rate relief through self-assessment. The ISA offers no upfront tax relief. This is too large an advantage to ignore. Organic Facts

Scenario 3: Planning to retire before 57

Best approach: Both — with heavy ISA weighting.

You need ISA savings to bridge the gap between your planned retirement date and the minimum pension access age. Calculate how much you’ll need to live on from retirement to 57, and ensure your ISA can cover it.

Scenario 4: Self-employed with no employer pension

Best approach: SIPP as primary vehicle, ISA as secondary.

Without an employer contributing to your pension, you must build it yourself. The SIPP’s tax relief is especially valuable when you’re responsible for 100% of your retirement funding. Max your SIPP contributions first — then add ISA savings for flexibility.

Scenario 5: Close to retirement, concerned about estate planning

Best approach: Review urgently before April 2027.

The upcoming IHT rule change on pensions makes this a situation that genuinely warrants professional advice. The relative attractiveness of ISA vs SIPP for estate planning is shifting significantly.

11. The UK Savings Order of Operations

Here’s the clear priority sequence for most UK investors in 2026:

| Step | Action | Why |

|---|---|---|

| 1st | Workplace pension up to employer match | Free money — instant 50–100% return |

| 2nd | Pay off high-interest debt | 20%+ debt costs more than any investment earns |

| 3rd | Build 3–6 months emergency cash | Always accessible — in a regular savings account |

| 4th | SIPP (if higher-rate taxpayer) | 40–45% tax relief is exceptional value |

| 4th | ISA (if basic-rate taxpayer or needing flexibility) | Better flexibility at lower tax relief |

| 5th | Max whichever you didn’t prioritise in step 4 | Both are worth maxing if income allows |

| 6th | General Investment Account | No tax advantages but no limits either |

Both, in this order: contribute enough to your SIPP to claim full employer match and, if relevant, salary-sacrifice into the 40% tax band — then fill your £20,000 ISA allowance for bridge-period flexibility, then return to the SIPP for additional tax relief. FlavoristaLuna

For more personal finance guides, including our full breakdown of Index Funds vs ETFs and what compound interest actually does to your money, head to InfoBrave.

12. Frequently Asked Questions

What is the main difference between an ISA and a SIPP?

The core difference is flexibility versus tax relief. An ISA lets you access your money at any age with no tax on withdrawal — but gives you no upfront tax relief. A SIPP gives you significant tax relief on contributions (20–45% depending on your tax band), but your money is locked until age 55 — rising to 57 from April 2028 — and withdrawals in retirement are taxed as income.

What are the ISA and SIPP allowances for 2026/27?

The standard ISA allowance is £20,000 for 2026/27. The SIPP annual allowance is £60,000 — or 100% of earnings if lower. The SIPP allowance includes both your own contributions and any employer contributions. Unused SIPP allowance from the past three tax years can also be carried forward; the ISA allowance cannot. Grow Forage Cook Ferment

Can I have both an ISA and a SIPP?

Yes — and for most UK investors with the budget to use both, holding both is the optimal strategy. They complement each other: the SIPP provides tax relief and long-term retirement savings; the ISA provides flexible, accessible tax-free savings for shorter-term goals or bridging early retirement.

How much tax relief do I get on SIPP contributions?

The relief is equal to your marginal income tax rate — basic rate taxpayers get 20% relief, higher rate taxpayers get 40%, and additional rate taxpayers get 45%. Basic rate relief is added automatically by your SIPP provider. Higher and additional rate taxpayers must claim the extra relief through their Self Assessment tax return. Semrush

What age can I access my SIPP?

Currently age 55. This rises to 57 from April 2028 under rules confirmed by the FCA. Accessing a SIPP before the minimum pension age triggers a 55% unauthorised payment tax charge from HMRC. Always check your own pension documents as some older “protected pension ages” may apply.

What is the ISA bridge strategy?

The ISA bridge is a retirement planning strategy where you build sufficient ISA savings to fund your living costs during the gap between your chosen retirement date and the minimum SIPP access age (57 from 2028). It’s essential for anyone planning to retire before 57 — without ISA savings as a bridge, your pension pot is inaccessible and you have no income.

Is the SIPP still worth it after the April 2027 inheritance tax change?

Yes — especially for anyone in a higher tax bracket. The tax relief on contributions remains one of the most powerful wealth-building advantages in UK personal finance. The April 2027 IHT change primarily affects people with large pension pots who were planning to leave pension wealth to beneficiaries as an estate planning strategy. For straightforward retirement saving, the SIPP remains highly attractive. Review your specific situation with a regulated financial adviser if estate planning is a priority for you.

What happens if I contribute more than my SIPP annual allowance?

You’ll face an annual allowance charge from HMRC — essentially a tax bill that claws back the tax relief on excess contributions. You’re responsible for reporting and paying this charge via Self Assessment. If you have unused allowance from the previous three tax years, you may be able to carry it forward to increase your contribution limit in the current year — but check this carefully before contributing large sums.

You may also like: Roth IRA vs 401(k): Which Should You Open First in 2026?