Trying to pick the perfect moment to invest is one of the most expensive habits a beginner can have. Waiting for the market to “calm down.” Holding cash because it “feels like a bad time.” Checking your portfolio every morning and wondering whether to buy today or wait until next week.

Every month you spend waiting is a month compound interest isn’t working for you.

Dollar-cost averaging is the strategy that fixes this problem — and it does it by making the timing decision completely irrelevant. Instead of picking the perfect moment, you invest a fixed amount at regular intervals, automatically, no matter what the market is doing.

It’s the closest thing personal finance has to a genuinely beginner-proof strategy. This guide explains exactly how it works, walks you through a real month-by-month example, gives you the honest verdict on DCA versus lump sum investing, and then shows you exactly how to set it up on every major platform — in both the USA and the UK.

Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute financial or investment advice. All investing carries risk, including the risk of losing money. Past performance does not guarantee future results. Always consult a regulated financial adviser before making investment decisions.

1. What Is Dollar-Cost Averaging? (One Sentence)

Dollar-cost averaging (DCA) means investing a fixed amount of money at regular intervals — monthly, fortnightly, or weekly — regardless of what the market is doing.

That’s it. You pick an amount ($100, $250, $500 — whatever fits your budget). You pick a schedule (1st of every month, every payday). And then you invest that amount automatically, every single time, whether the market is up, down, or sideways.

Dollar-cost averaging is a strategy in which you invest your money in equal portions, at regular intervals, regardless of which direction the market or a particular investment is going. Your purchases occur regardless of the changes in price for the stock or other investment, potentially helping reduce the impact of volatility on the overall purchase. Link Assistant

The result: when prices are high, your fixed amount buys fewer shares. When prices are low, your fixed amount buys more shares. Over time, this produces an average cost per share that is often lower than the average market price across that same period. More on the exact maths in the next section.

2. How DCA Actually Works: A Real Month-by-Month Example

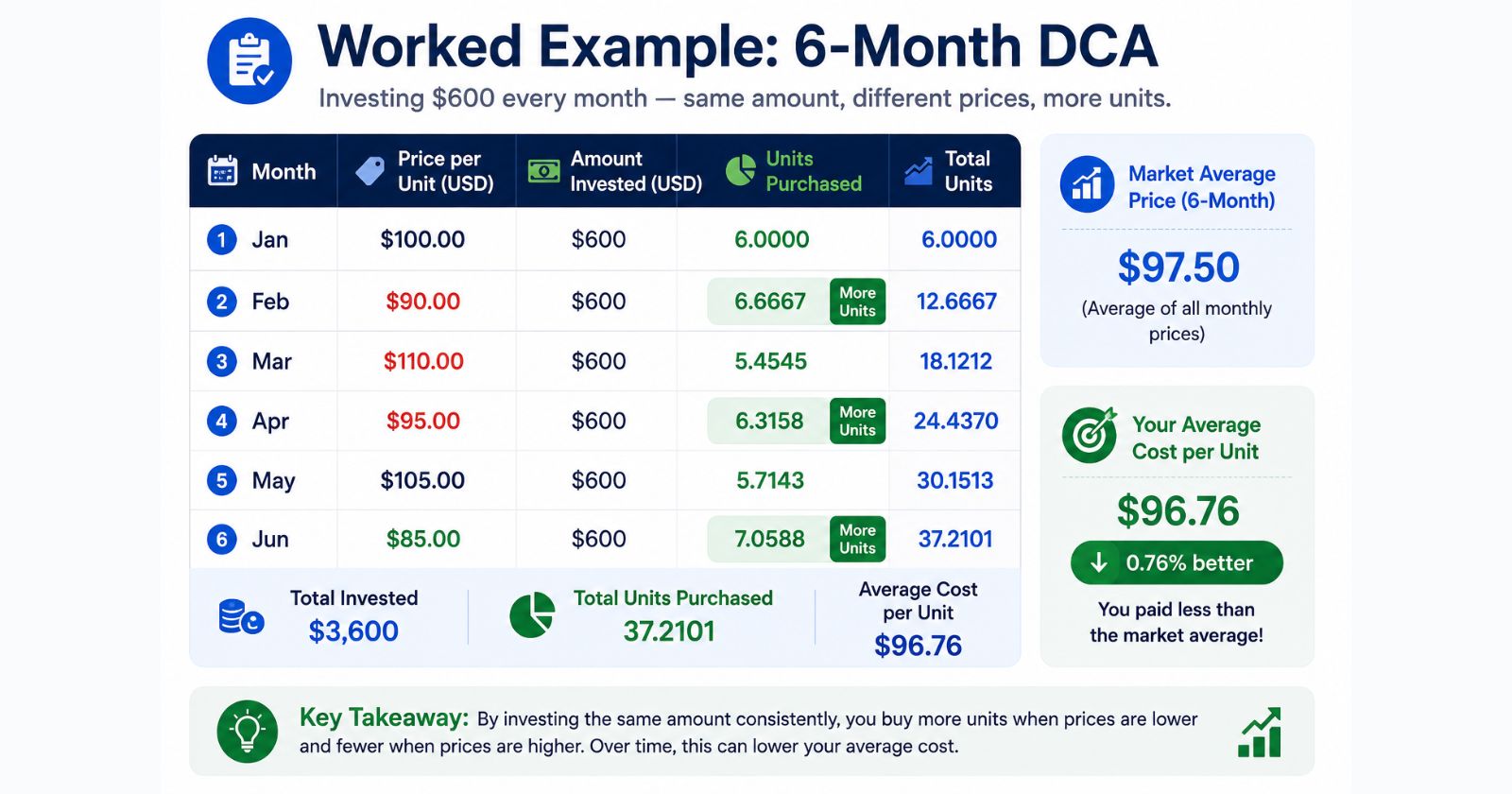

This is the section most guides skip — a genuine worked example that shows the maths in action. Let’s say you invest $200 per month into an S&P 500 index fund over six months, and the price per unit moves like this:

| Month | Unit price | Units bought | Running total units | Total invested |

|---|---|---|---|---|

| January | $100 | 2.00 | 2.00 | $200 |

| February | $80 | 2.50 | 4.50 | $400 |

| March | $60 | 3.33 | 7.83 | $600 |

| April | $80 | 2.50 | 10.33 | $800 |

| May | $100 | 2.00 | 12.33 | $1,000 |

| June | $120 | 1.67 | 14.00 | $1,200 |

After 6 months, you’ve invested $1,200 and own 14.00 units.

Now here’s the critical comparison:

- Your average cost per unit: $1,200 ÷ 14.00 = $85.71

- Simple average of all 6 prices: ($100 + $80 + $60 + $80 + $100 + $120) ÷ 6 = $90.00

You paid $85.71 per unit — while the market’s average price over those months was $90.00.

That $4.29 difference per unit across 14 units means you’re $60 ahead compared to someone who tried to buy at the “average” price each month. And you did this without predicting anything, timing anything, or making a single active decision after the first one.

Pro Tip: The reason DCA produces a lower average cost is mathematical. Because you invest the same fixed dollar amount, you automatically buy more units when prices are low and fewer units when prices are high. A rising market followed by a dip followed by a recovery is actually the ideal DCA scenario — the dip is when your fixed amount buys the most shares.

3. Why Most Beginners Fail Without It

The single biggest threat to a beginner investor’s returns isn’t market volatility, inflation, or even picking the wrong fund. It’s their own behaviour.

Here’s the typical pattern:

- Markets go up — beginner feels confident, invests more

- Markets drop — beginner panics, stops investing or sells

- Markets recover — beginner waits for another drop before buying back in

- Markets continue rising — beginner buys back in near the top

- Repeat until frustrated and broke

The single biggest threat to long-term investing performance isn’t market volatility — it’s the investor’s own behaviour. When you can buy and sell with a few clicks, emotion creeps in. A bad jobs report, a Fed announcement, a dip in the news cycle — all of it becomes a reason to do something when the right answer is usually to do nothing. Semrush

Dollar-cost averaging solves this by removing the decision entirely. There’s no “should I invest this month?” There’s no “is now a good time?” The money leaves your account on a fixed date and goes into your chosen fund. Automatically. Every period. Full stop.

Automating removes that decision entirely. Your contributions go in on schedule, every month, regardless of what the market did last week. This is the core principle behind dollar-cost averaging — you buy more shares when prices are low and fewer when they’re high, without ever having to predict which is which. Searchvolume

The automation is not just convenient. It’s psychologically protective. You can’t panic-sell what you didn’t consciously buy that day.

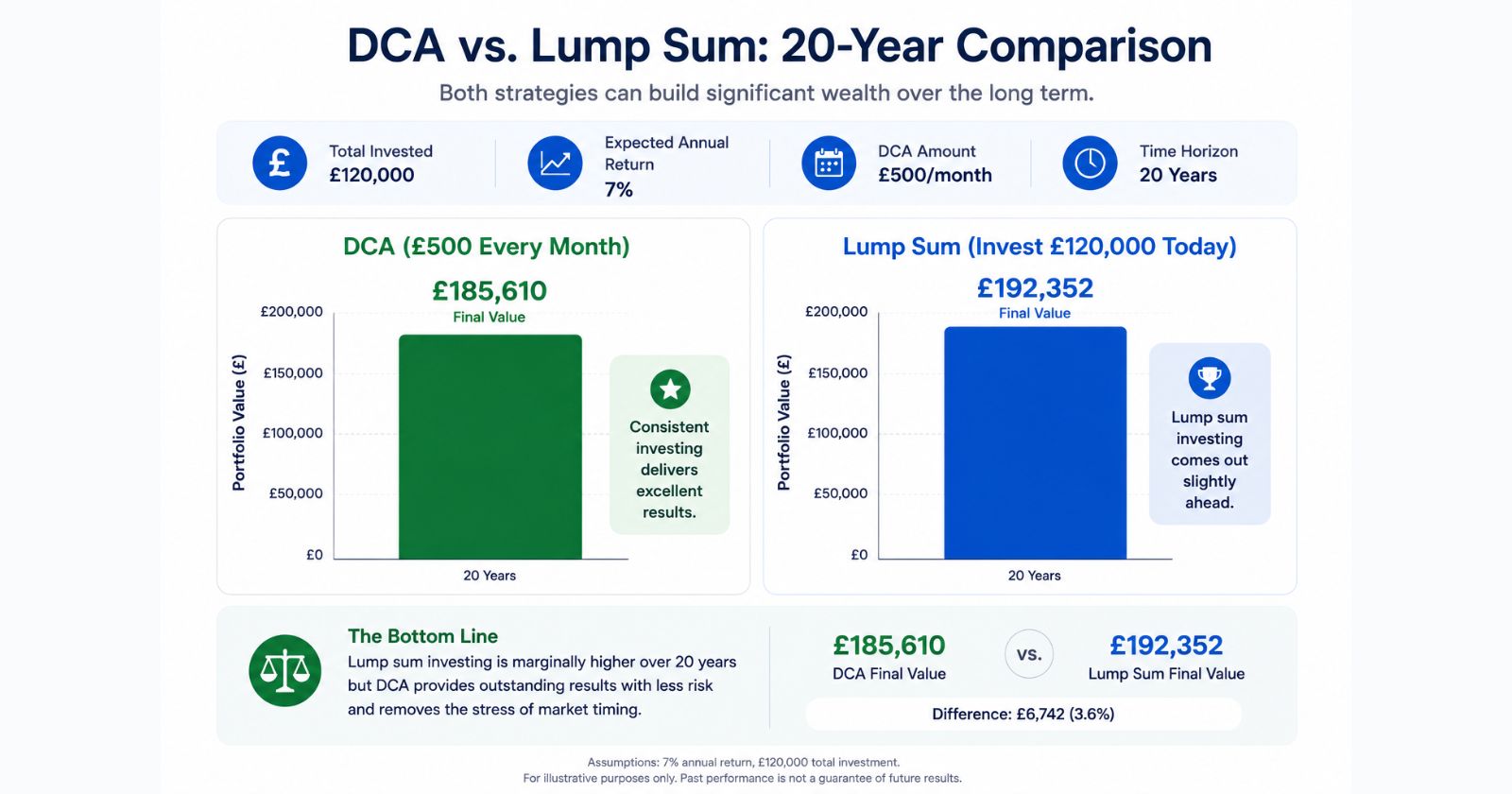

4. Dollar-Cost Averaging vs Lump Sum: The Honest Truth

Most personal finance articles dodge this question. We’re not going to.

Here’s the honest answer, backed by the data:

Mathematically, lump sum investing wins most of the time.

Vanguard’s research examining market data from 1926 through 2015 found that lump-sum investing outperformed dollar-cost averaging roughly two-thirds of the time across U.S., U.K., and Australian markets. In the U.S. market, lump-sum investing generated higher returns than 12-month dollar-cost averaging in 68% of the rolling 10-year periods examined. The mathematical explanation is simple: markets trend upward over time. Semrush

Lump sum investing tends to outperform dollar-cost averaging about 70% of the time, according to research, thanks to more time in the market. Dollar-cost averaging spreads out risk and can ease anxiety during volatile or uncertain markets. Slow Living Kitchen

So why does anyone use DCA? Two big reasons:

Reason 1: Most people don’t have a lump sum.

The lump sum vs DCA debate is largely irrelevant for the majority of investors. If you’re investing $300 from each monthly paycheck, you’re doing DCA by default. You can’t lump sum money you haven’t earned yet. For regular savers investing from income, DCA is simply the only realistic option.

Reason 2: Psychology beats maths if the maths makes you panic-sell.

Dollar-cost averaging spreads out risk and can ease anxiety during volatile or uncertain markets. The best strategy depends on your financial goals, time horizon, and how you feel about market swings. Organic Facts

A lump sum investor who panics and sells during a downturn earns far less than a DCA investor who never wavers. A mathematically superior strategy executed poorly beats a mathematically optimal strategy executed well only on paper.

| Scenario | Best approach | Why |

|---|---|---|

| Investing monthly income | DCA | You have no lump sum — DCA is automatic |

| Received a windfall (bonus, inheritance) | Lump sum (mathematically) | More time in market = better expected returns |

| Windfall + high anxiety about markets | DCA over 6–12 months | Worse in theory, better in practice if it keeps you invested |

| Just starting out, nervous investor | DCA | Builds the habit without the psychological shock |

| Experienced investor with conviction | Lump sum | If the research supports it and you won’t panic |

The bottom line: if you’re investing regular income, DCA is your strategy by default and it works brilliantly. If you have a lump sum, lump sum investing has the mathematical edge — but only if you can truly commit to it without emotional interference.

5. The Psychology of DCA: Why It Works When Nothing Else Does

Markets don’t go up in a straight line. They lurch, dip, correct, crash, and recover. That volatility is what creates long-term returns — but it’s also what causes most individual investors to underperform the market they’re invested in, because they sell at the wrong time.

DCA turns market dips from terrifying events into mechanical advantages.

When the market drops 20%, a DCA investor doesn’t panic. They know that next month’s fixed contribution will buy more units at the lower price. The dip becomes an opportunity built into their system — they don’t even have to decide to take it.

Dollar-cost averaging can help take some of the guesswork and emotion out of investing, which may keep you from panicking when prices fall or buying more when things might seem too good to be true. While dollar-cost averaging doesn’t ensure a profit or protect against loss in declining markets, it’s a strategy that some investors use to make regular contributions without trying to “time the market.” Semrush

Think of it like buying petrol for your car. When prices are low at the pump, you fill up the tank. When prices are high, you put in less. Over a year, you’ve paid below the average price without ever having to predict where prices were heading.

DCA applies that same logic to investing — automatically, every month, forever.

6. Pound Cost Averaging: The UK Version

In the UK, the exact same strategy goes by a slightly different name: pound cost averaging (PCA). Same concept, same mechanics — just denominated in pounds rather than dollars.

The strategy works identically inside a Stocks and Shares ISA or SIPP:

- Set up a monthly direct debit from your bank account into your investment platform

- Platform automatically buys your chosen fund (typically a global index fund or FTSE tracker)

- Same fixed amount every month, regardless of market conditions

- When markets are down, your £200 buys more units; when markets are up, it buys fewer

Pound cost averaging means investing smaller fixed amounts over time rather than deploying all available money at once. By buying at different price points, investors avoid the regret of putting all their money in right before a market decline. Asinsight

The UK platforms that best support this are Vanguard UK (simple, low cost), InvestEngine (commission-free ETF investing with full automation), and Hargreaves Lansdown (for those who want more investment choice). We’ll cover the exact setup steps below.

One UK-specific note: the tax wrapper matters. Setting up pound cost averaging inside a Stocks and Shares ISA means all your growth and withdrawals are tax-free. Setting it up inside a SIPP means you receive tax relief on each contribution. Both are dramatically better than investing in a general account. For more on choosing between them, see our full ISA vs SIPP guide.

7. What to Actually Invest In When You DCA

DCA is a strategy — not an investment in itself. The question of what to put your regular contributions into matters a lot.

For most beginners doing DCA, the answer is simple: a broad, low-cost index fund or ETF.

Here’s why. DCA is designed to smooth out the volatility of markets over time. That smoothing effect only works if the underlying investment has a reliable long-term upward trend. Individual stocks can and do go to zero. Narrow sector funds can underperform for decades. Broad market index funds have never permanently lost value over any 20-year period in recorded history.

Recommended DCA targets for most beginners:

| Market | USA investors | UK investors |

|---|---|---|

| US market | FXAIX / VOO / SCHB | Vanguard US Equity Index |

| Global market | VTWAX / VT | HSBC FTSE All World / VWRP |

| UK market | — | Vanguard FTSE UK All Share |

| Bonds (defensive) | BND / AGG | Vanguard UK Gov Bond Index |

For most beginners, a single global index fund is sufficient and simplest. It gives you exposure to thousands of companies across dozens of countries in a single investment — maximum diversification, minimum complexity.

Our guide to Index Funds vs ETFs explains the specific differences between these fund types and helps you choose the right one for your account.

Pro Tip: Don’t chase recent performance when choosing your DCA target. The fund that performed best last year is frequently not the best fund for the next decade. Stick with broad market index funds tracking the entire global or US market.

8. How to Set Up Automatic DCA: USA Platforms

This is the practical section most guides skip. Here’s how to actually automate DCA on the three most popular US platforms in 2026.

Fidelity

Fidelity allows you to automate stock, mutual fund, ETF, and basket trades. Recurring investments can be paid from your Fidelity core cash position or from your linked bank account. You can set the amount, frequency, and timing of your recurring investments, and change them whenever you need to. Local Search Forum

Steps:

- Log in at fidelity.com

- Navigate to Accounts & Trade → Transfers → Recurring Transfers

- Select your account (Roth IRA, brokerage, etc.)

- Choose “Transfer and invest funds from external bank account”

- Select your fund (e.g. FXAIX or FZROX)

- Enter your fixed amount and choose your frequency (weekly, biweekly, monthly)

- Set your start date — ideally your payday

- Review and confirm

Fidelity supports recurring investments as low as $1 for fractional shares, making it accessible at any budget.

Charles Schwab

Schwab’s Automatic Investment Plan (AIP) lets you put your index fund contributions on autopilot — as little as $1 per transaction, on a schedule you set. Once it’s running, you don’t have to think about it. ScienceDirect

Steps:

- Log in at schwab.com

- Go to Trade → Automatic Investing

- Click “Enroll” next to the fund you want to automate

- Enter your dollar amount, frequency, and transaction date

- Select “Continue” then review and “Submit”

Schwab requires that sufficient cash be available in your account on the date of each AIP transaction. If funds aren’t there when the transaction is scheduled, no investment is made for that period. This is why timing your bank transfer a day or two before the transaction date is important. Keywords Everywhere

Vanguard USA

Vanguard investors can set up recurring investments for eligible Vanguard mutual funds and Vanguard ETF positions. Recurring purchases are available for Vanguard ETFs, while mutual funds can be used for recurring investments and recurring withdrawals. SEOmator

Steps:

- Log in at vanguard.com

- Navigate to the “Automatic or Recurring Investments” section

- Select the fund (e.g. VFIAX or VTSAX)

- Enter amount, frequency (monthly is most common), and funding source

- Confirm and submit

Note: Vanguard mutual funds typically require a $1,000 minimum initial investment before recurring purchases can be set up. After that, recurring amounts can be much smaller.

9. How to Set Up Automatic DCA: UK Platforms

Vanguard UK

The simplest UK option for beginners investing in index funds.

Steps:

- Open a Stocks and Shares ISA or general account at vanguard.co.uk

- Complete identity verification

- Under “Regular investing”, select your fund (e.g. Vanguard FTSE Global All Cap)

- Set your monthly amount (minimum £100/month for regular investing)

- Link your bank account and confirm your payment date

- Vanguard automatically purchases units on your chosen date each month

InvestEngine

Commission-free ETF investing with full DCA automation — ideal for those who want to invest in ETFs rather than mutual funds.

Steps:

- Open a Stocks and Shares ISA or general account at investengine.com

- Build your portfolio (choose your ETFs — e.g. VWRP for global market)

- Go to “Auto-invest” settings

- Set your monthly contribution amount and date

- InvestEngine automatically buys your selected ETFs proportionally each month

Hargreaves Lansdown

More investment choice, higher fees — better for those who want access to individual shares and a wider fund range alongside index funds.

Steps:

- Open a Stocks & Shares ISA at hl.co.uk

- Go to “Regular Savings Plan” under account settings

- Select your fund and set a monthly amount

- Choose your payment date (align with payday for easiest budgeting)

- Confirm bank direct debit

10. Common DCA Mistakes to Avoid

Mistake 1: Stopping during a market crash.

This is the single most damaging thing you can do with DCA. The whole point is to keep investing through the dip — that’s when your fixed amount buys the most units. Stopping is exactly backwards. If you feel the urge to stop during a crash, turn off your portfolio view and let the automation run.

Mistake 2: Investing in something too volatile or speculative.

DCA works best with investments that have a reliable long-term upward trend. Applying it to individual stocks, cryptocurrency, or narrow sector funds removes the statistical foundation the strategy rests on. Stick to broad index funds.

Mistake 3: Choosing an amount that strains your budget.

If your DCA contribution is so large that you struggle with it some months, you’re likely to start skipping. Set a sustainable amount — even £50 or $50 — that you genuinely won’t miss. You can always increase it later as income grows.

Mistake 4: Forgetting to invest your DCA in a tax-advantaged account.

Putting your saving and investing on automatic is a small change that can lighten your mental load — and it may significantly impact your net worth over the long term. But doing it in a taxable account when a Roth IRA (USA) or Stocks and Shares ISA (UK) is available is an unnecessary cost. Always wrap your DCA inside a tax-advantaged account first. Google Support

Mistake 5: Constantly changing your fund or amount.

DCA works through consistency and time. Tweaking your fund every quarter because you saw something perform better last month is counter to the entire strategy. Set it, automate it, and leave it for years.

For more guides on building wealth with simple, proven strategies, explore InfoBrave’s finance and informative guides — and check out InfoBrave for more practical everyday content.

11. Frequently Asked Questions

What is dollar-cost averaging in simple terms?

Dollar-cost averaging means investing a fixed amount of money at regular intervals — like $200 every month — regardless of whether the market is up or down. When prices are low, your fixed amount buys more shares. When prices are high, it buys fewer. Over time this produces an average cost per share that is often lower than the market’s average price across the same period.

Does dollar-cost averaging actually work?

Yes — particularly for regular investors investing from monthly income. It removes emotional decision-making, ensures you never miss a contribution, and mechanically buys more shares during market dips. Research shows it doesn’t maximise returns compared to lump-sum investing in rising markets, but for most people investing from income rather than a windfall, it’s the most practical and psychologically sound approach available.

Is DCA better than lump-sum investing?

Lump-sum investing tends to outperform dollar-cost averaging about 70% of the time, thanks to more time in the market. But dollar-cost averaging spreads out risk and can ease anxiety during volatile or uncertain markets. The best strategy depends on your financial goals, time horizon, and how you feel about market swings. For most regular investors, DCA is the default because they don’t have a lump sum — they invest from income. FlavoristaLuna

How much should I invest with dollar-cost averaging?

Start with whatever you can genuinely afford to invest every single month without straining your budget. Even $50 or £50 a month compounded over decades becomes significant wealth — see our compound interest guide for the real numbers. The amount matters far less than the consistency. You can always increase contributions as income grows.

What is the best investment for dollar-cost averaging?

A broad, low-cost global or US index fund or ETF. These have reliable long-term upward trends, hold thousands of companies for maximum diversification, and charge minimal fees. Popular choices include VOO or FXAIX for US investors and VWRP or HSBC FTSE All World for UK investors. Avoid using DCA with single stocks, sector ETFs, or speculative assets.

What is pound cost averaging?

Pound cost averaging is the UK term for dollar-cost averaging. The strategy is identical — invest a fixed amount in pounds at regular intervals — but is applied inside a Stocks and Shares ISA or SIPP using UK investment platforms like Vanguard UK, InvestEngine, or Hargreaves Lansdown.

Should I stop DCA investing during a market crash?

No — and this is the most important rule. A market crash is when DCA is working hardest for you. Your fixed monthly contribution buys significantly more units at lower prices, reducing your average cost per unit. Stopping during a crash locks in losses and means you miss the recovery gains. The discipline to keep investing through downturns is what separates successful DCA investors from unsuccessful ones.

Can I do DCA inside a Roth IRA or ISA?

Absolutely — and you should. Setting up DCA inside a tax-advantaged account (Roth IRA or 401(k) in the USA, Stocks and Shares ISA or SIPP in the UK) means all your growth is tax-free or tax-deferred. Always maximise tax-advantaged contributions before investing in a regular taxable account.

You may also like: Index Funds vs ETFs: Which Is Better for Beginners in 2026?