A massive hailstorm rolls through your city overnight. You wake up, walk outside, and your car looks like a golf ball. Or you come out of the grocery store and your car is just — gone. Stolen.

In both situations, your collision insurance pays nothing. Your liability insurance pays nothing. The only coverage that steps in and writes you a check? Comprehensive.

Most drivers know comprehensive coverage exists. Far fewer know exactly what it covers, what it doesn’t, how much it actually costs, or — critically — when it stops being worth paying for.

This guide answers all of it, with verified 2026 numbers and zero jargon.

Important Disclaimer: This article is for informational purposes only and does not constitute insurance or financial advice. Coverage terms vary by policy, insurer, and state. Always read your specific policy documents and consult a licensed insurance professional for advice tailored to your situation.

1. What Is Comprehensive Car Insurance?

Comprehensive car insurance is the coverage that pays for damage to your vehicle caused by events that have nothing to do with driving into something.

Sometimes called “other than collision” coverage, comprehensive insurance protects against theft, vandalism, weather damage, animal strikes, falling objects, fire, and natural disasters. WebMD

Think of it this way: if you caused it by driving — that’s collision. If the world did it to your car while it was just sitting there — that’s comprehensive.

Comprehensive coverage pays for damage to your car from events that have nothing to do with driving into something. Healthline

It’s important to understand what comprehensive coverage is not. “Full coverage” is not the same as comprehensive alone. Full coverage typically includes comprehensive, collision, and liability insurance, while comprehensive alone only covers non-collision damages. When a lender tells you they require “full coverage,” they mean all three working together. Tea Drops

Pro Tip: The industry nickname for comprehensive is “comp” — you’ll hear this term from agents, adjusters, and in policy documents. When someone says “I have comp and collision,” they mean they carry both types of coverage on top of their required liability insurance.

2. What Does Comprehensive Car Insurance Cover?

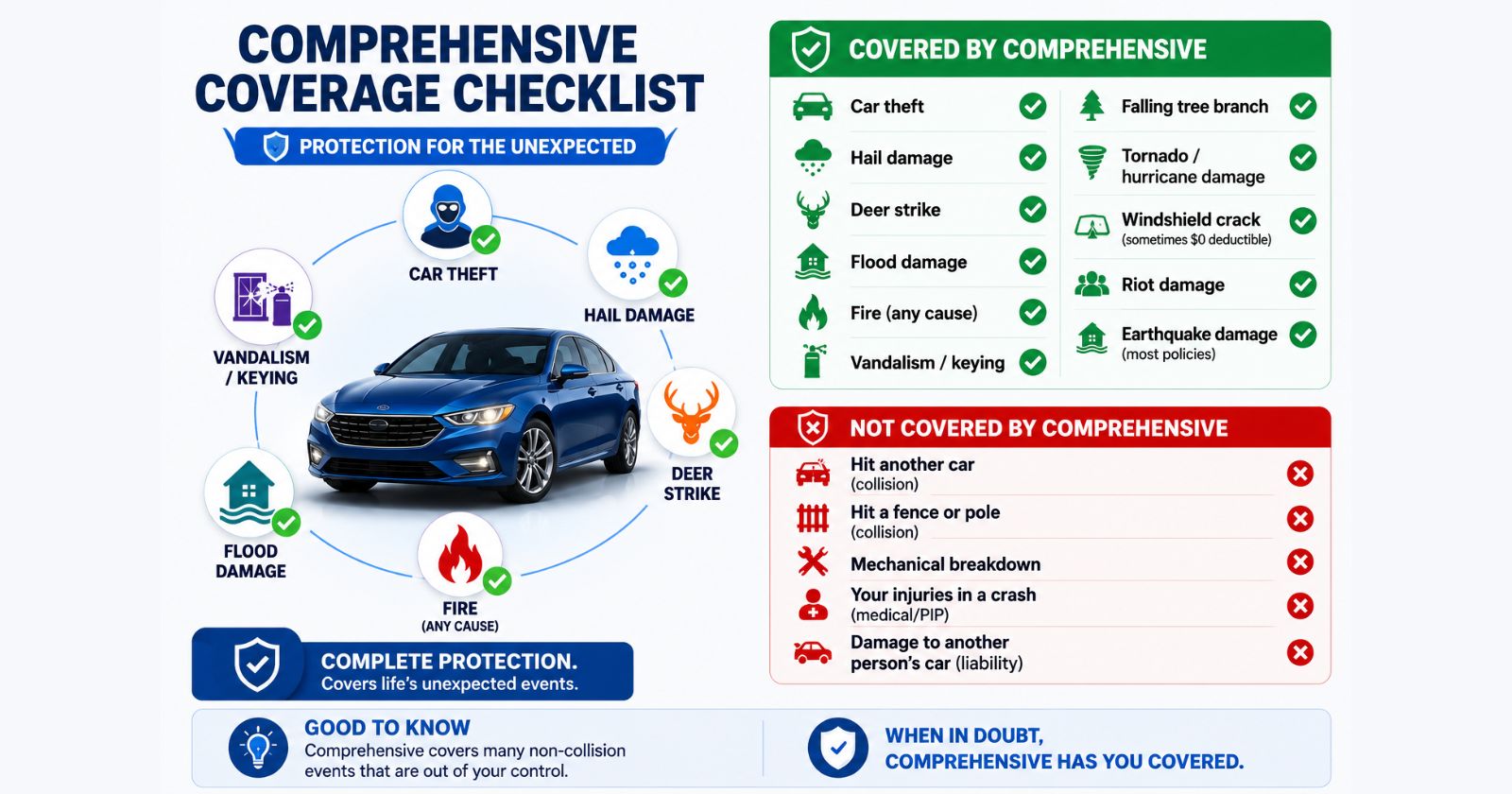

Here’s the complete list of what a standard comprehensive policy covers in 2026:

✅ Theft

If your car is stolen and not recovered, comprehensive pays you the actual cash value (ACV) of the vehicle — what it was worth on the market the day it was taken, minus your deductible. If it’s recovered but damaged, comprehensive covers the repairs.

Auto theft remains a significant risk. According to the NICB, the most stolen vehicles in 2025 include the Hyundai Elantra, Hyundai Sonata, Kia Optima, and Kia Sportage — driven partly by the viral “Kia Boys” theft method. If you drive one of these models, comprehensive isn’t optional — it’s essential. WebMD

✅ Weather Damage

Severe weather coverage includes damage by hail, tornadoes, hurricanes, and other natural events. This is one of the most common comprehensive claims filed in America. nih

Hail damage is the single largest comprehensive claim category, with the average hail claim costing approximately $4,300 in 2025. If you live anywhere in Tornado Alley — Texas, Oklahoma, Kansas, Nebraska — this coverage alone is worth every penny of the premium. WebMD

✅ Animal Strikes

Hit a deer? That’s comprehensive, not collision. Wildlife collisions alone cause over $1 billion in vehicle damage annually in the United States. The average animal-strike claim exceeds $4,000, and insurers process over 2 million such claims each year. West Virginia, Montana, and Pennsylvania have the highest deer-collision rates per driver. WebMD

✅ Flood Damage

If a flash flood submerges your car — whether parked or caught in rising water — comprehensive pays for repairs or replacement. With flood events increasing across the USA, this protection is more relevant than ever.

✅ Fire

Covers your vehicle if it catches fire from a mechanical fault, arson, or is caught in a wildfire.

✅ Vandalism

Someone keys your car, smashes your windows, or spray-paints graffiti on it? Comprehensive covers the repair bill, minus your deductible.

✅ Falling Objects

Tree branches, rocks kicked up on the highway, ice sliding off a building — if something falls on your car, comprehensive handles it.

✅ Civil Disturbances

Riots and civil unrest that result in damage to your vehicle are covered under most comprehensive policies.

✅ Windshield and Glass Damage

Some insurers waive the deductible for glass-only claims — and in Arizona, Florida, Kentucky, and South Carolina, state law requires insurers to offer zero-deductible glass coverage. More on this below. WebMD

Quick-reference coverage checklist:

| Event | Covered by comprehensive? |

|---|---|

| Car theft | ✅ Yes |

| Hail damage | ✅ Yes |

| Deer strike | ✅ Yes |

| Flood damage | ✅ Yes |

| Fire (any cause) | ✅ Yes |

| Vandalism / keying | ✅ Yes |

| Falling tree branch | ✅ Yes |

| Tornado / hurricane damage | ✅ Yes |

| Windshield crack | ✅ Yes (sometimes $0 deductible) |

| Riot damage | ✅ Yes |

| Earthquake damage | ✅ Yes (most policies) |

| Hit another car | ❌ No — that’s collision |

| Hit a fence or pole | ❌ No — that’s collision |

| Mechanical breakdown | ❌ No |

| Your injuries in a crash | ❌ No — that’s medical/PIP |

| Damage to another person’s car | ❌ No — that’s liability |

3. What Comprehensive Insurance Does NOT Cover

Knowing the exclusions is just as important as knowing the coverages — especially when you’re standing at a body shop trying to figure out whether to file a claim.

Not covered by comprehensive:

- Collision damage — If you drive into another car, a guardrail, a mailbox, or a tree, that’s collision coverage — not comprehensive. A common misconception is that hitting a large animal while swerving causes a collision claim, but the animal strike itself is comprehensive.

- Mechanical failures — Engine breakdown, transmission failure, worn brakes — none of these are covered. You’d need a vehicle service contract or extended warranty for those.

- Your personal belongings inside the car — Your laptop, golf clubs, or camera stolen from your car are not covered by comprehensive. Your homeowner’s or renter’s insurance handles personal property stolen from a vehicle.

- Injuries to you or others — Comprehensive is property coverage only. Medical expenses from an accident fall under personal injury protection (PIP), medical payments coverage (MedPay), or health insurance.

- Regular wear and tear — Tires wearing down, paint fading, interior aging — none of it is covered. Insurance covers sudden, unexpected events.

- Damage you intentionally cause — Filing a claim for damage you deliberately inflicted is insurance fraud. Policies explicitly exclude intentional acts.

4. Comprehensive vs Collision vs Liability: The Key Differences

These three coverage types confuse more drivers than anything else in auto insurance. Here’s the clearest breakdown possible:

| Coverage type | What it covers | Required by law? | Who it protects |

|---|---|---|---|

| Liability | Damage and injuries you cause to others | Yes — in 49 states | Other people |

| Collision | Damage to your car from hitting something | No (lenders may require) | Your car |

| Comprehensive | Damage to your car from non-collision events | No (lenders may require) | Your car |

Comprehensive vs collision: collision covers damage when your car hits something while moving. Most drivers need both. Together they protect your vehicle from nearly every scenario. Healthline

The simplest memory trick: liability protects other people from you. Collision and comprehensive protect your car from everything else.

Comprehensive vs liability: liability coverage pays for damage and injuries you cause to others in an accident. Liability coverage is required by all states, except New Hampshire. Healthline

80% of insured drivers buy comprehensive coverage alongside liability insurance, according to the Insurance Information Institute. Most of those also carry collision, making them “fully covered” in the industry’s practical definition. Healthline

5. How Much Does Comprehensive Insurance Cost in 2026?

Comprehensive coverage averages $200 to $350 per year on its own, according to MoneyGeek’s analysis of over 2.4 million quotes. Drivers buy it with collision coverage as part of a full coverage policy, which averages $137 per month nationally. Healthline

To put that in context against the full picture:

The national average cost of car insurance in the United States as of May 2026 is $2,276 annually or $190 per month, according to Experian data. The national average cost of full coverage car insurance is $2,926 annually or $244 per month. An Off Grid Life

So comprehensive on its own — roughly $200–$350 per year — is one of the least expensive parts of your total insurance package, yet it protects against some of the most financially devastating scenarios (total theft, flood, hail).

What affects your comprehensive premium:

- Your car’s value — A $40,000 SUV costs more to insure comprehensively than an $8,000 sedan

- Your location — Living in a hail-prone state, high-theft zip code, or flood zone increases your rate

- Your deductible — Higher deductible = lower premium (more on this below)

- Your claims history — Prior comprehensive claims can raise your rate at renewal

- Your credit score — Most states allow insurers to factor in credit-based insurance scores

Nationally, the average full-coverage premium dropped 6% to $2,144 a year in 2025, according to Insurify analysis. Wyoming (-30%), Iowa (-25%) and Arkansas (-23%) had the largest price cuts — but ten states continued to see prices rise, led by New Jersey (+20%), Rhode Island (+13%) and Michigan (+12%). FlavoristaLuna

6. How Your Deductible Works (And How to Pick the Right One)

Your comprehensive deductible is the amount you pay out of pocket when you file a claim before your insurance covers the rest.

Example: Your car suffers $3,500 in hail damage. You have a $500 deductible. You pay $500. Your insurer pays $3,000.

Common deductible amounts: $250, $500, $1,000, $1,500, $2,000.

The relationship is simple: higher deductible = lower monthly premium.

A move from $500 to $1,000 might save $15–$35 per month, but it varies by car, driver, and state. Some carriers offer “vanishing deductible” credits that reduce your deductible over time for safe driving. ALM Corp

The right deductible formula:

Choose the highest deductible you could genuinely pay from your emergency fund without financial stress. If your emergency fund holds $1,000, a $1,000 deductible is manageable — and you’ll save meaningfully on premiums. If you’re living paycheck to paycheck, a $250 or $500 deductible gives you peace of mind even if the premium is slightly higher.

Your deductible applies per incident, not per year — so if you have two separate incidents in one year and a $1,000 deductible, you’re potentially out $2,000. Think about your realistic claim likelihood before choosing. Organic Facts

Pro Tip: Ask your insurer about a glass deductible waiver. Many companies will waive your deductible entirely for windshield-only claims — meaning a cracked windshield repair costs you nothing out of pocket. This is separate from the state laws covered below.

7. The One Thing EV Owners Need to Know

Electric vehicle ownership is growing fast, and comprehensive coverage for EVs has a nuance most standard articles ignore.

Comprehensive car insurance covers theft, hail, fire, vandalism, animal collisions, falling objects, flood — and yes, this protection covers hail, flood, or theft damage to EV batteries and advanced driver assistance (ADAS) sensors, subject to your deductible. Cleveland Clinic

However, EV batteries are dramatically more expensive to replace than conventional engine components. A Tesla Model 3 battery replacement can run $10,000–$20,000. If your EV is flooded or fire-damaged, your insurer will pay actual cash value — but if your car is newer, that ACV should cover you. If your EV has depreciated significantly, you may be underinsured.

Key EV questions to ask your insurer:

- Does my policy cover damage to the battery pack specifically?

- Are my home charging equipment and wall charger covered if damaged by a covered event?

- Does my policy cover ADAS sensor recalibration costs after a covered repair?

- Do I need gap insurance given how fast EVs can depreciate?

These aren’t hypothetical questions. As EVs become mainstream, insurers are updating their policies — and gaps in coverage are emerging for drivers who don’t ask specifically.

8. When Should You Drop Comprehensive Coverage? (The 10% Rule)

Here’s the practical question most drivers ask — and that most insurance articles dodge with vague advice.

The updated 2026 rule of thumb: if the annual premium exceeds 10% of your car’s current market value, or if you can comfortably replace the vehicle out of pocket, it often makes financial sense to drop comprehensive coverage. Cleveland Clinic

The 10% rule in action:

| Car value | 10% threshold | Annual comp. premium | Keep or drop? |

|---|---|---|---|

| $25,000 | $2,500 | $280 | ✅ Keep — premium well under threshold |

| $12,000 | $1,200 | $260 | ✅ Keep — still worthwhile |

| $6,000 | $600 | $280 | ⚠️ Borderline — consider dropping |

| $3,500 | $350 | $270 | ❌ Drop — premium nearly equals threshold |

Other factors that change the calculation:

- You can’t afford to replace the car — Even on a low-value car, if losing it would financially devastate you, keep the coverage.

- You’re in a high-theft area — A $5,000 car in a high-theft zip code may still warrant comprehensive.

- You’re in a hail-prone region — One hailstorm can total an older vehicle; comprehensive makes sense even on lower-value cars in these areas.

- You have a loan or lease — While not legally required in most states, comprehensive auto insurance is typically required by lenders if you’re financing or leasing your car. You don’t get to make this choice if you don’t own the car outright. GoodRx

If your car is older and has depreciated significantly in value, you might consider dropping comprehensive and collision coverage to save on premiums, especially if the repair costs could exceed your car’s value. MasterClass

9. Do You Legally Have to Have Comprehensive Insurance?

No — with one major exception.

While not legally required in most states, comprehensive auto insurance coverage is often recommended for newer vehicles and is typically required by lenders if you’re financing or leasing your car. GoodRx

In plain terms:

- If you own your car outright: Comprehensive is optional in every state. You choose whether to carry it.

- If you finance your car (auto loan): Your lender almost certainly requires both comprehensive and collision coverage for the life of the loan. They’re protecting their asset — the car is technically collateral for the loan until you’ve paid it off.

- If you lease your car: Same as financing — the dealership or leasing company will require full coverage.

Dropping comprehensive while you have an outstanding loan is a breach of your loan agreement. If your lender discovers it — which they typically will when insurance lapses — they may force-place insurance on your behalf, which is nearly always more expensive than finding your own policy.

10. The State Glass Coverage Law Most Drivers Don’t Know

This is the content gap most comparison articles miss entirely.

In Arizona, Florida, Kentucky, and South Carolina, state law requires insurers to offer zero-deductible glass coverage. If you live in one of these four states and have comprehensive insurance, you may be entitled to get your windshield repaired or replaced without paying a single dollar out of pocket — including your deductible. WebMD

If you’re in Arizona, Florida, Kentucky, or South Carolina:

- Contact your insurer and confirm your glass deductible is waived

- If you have a cracked or chipped windshield, file a claim — it should cost you nothing

- Many drivers in these states are unaware and pay out of pocket unnecessarily

If you’re in any other state:

- Ask your insurer about a glass deductible waiver endorsement — many offer it optionally

- Some insurers waive the deductible for chip repairs only (not full replacement)

- This is worth asking about at renewal — it often costs nothing to add

For more everyday money and insurance guides, visit InfoBrave’s Informative section — and explore InfoBrave for practical guides on finance, tech, and lifestyle.

11. Frequently Asked Questions {#faq}

Does comprehensive car insurance cover hitting a deer?

Yes. Hitting a deer is covered by comprehensive insurance, since comprehensive coverage protects against damage caused by animals. This surprises many drivers who assume it would fall under collision because the car was moving. The distinction is animal strike (comprehensive) versus hitting a stationary object or another vehicle (collision). Even swerving to avoid a deer and hitting a guardrail is collision — only the direct animal strike is comprehensive. Tea Drops

Does comprehensive insurance cover a stolen car?

Yes — fully. If your car is stolen and not recovered, comprehensive pays you the actual cash value of the vehicle minus your deductible. If it’s recovered but damaged, comprehensive covers the repairs. Auto theft remains a significant risk, with Hyundai and Kia models among the most stolen vehicles in 2025 due to a widely known vulnerability. WebMD

Is comprehensive the same as full coverage?

No. Full coverage typically includes comprehensive, collision, and liability insurance, while comprehensive alone only covers non-collision damages. “Full coverage” is an informal term for having all three types — liability, collision, and comprehensive — working together on your policy. Tea Drops

Does comprehensive insurance cover flood damage?

Yes. Flood damage is explicitly covered under comprehensive car insurance, whether your car was parked during a flash flood or caught in rising water. This is one of the most valuable parts of the coverage for drivers in flood-prone regions.

Does comprehensive cover a cracked windshield?

Yes — windshield and glass damage is covered by comprehensive. Some insurers waive the deductible for glass-only claims, and in Arizona, Florida, Kentucky, and South Carolina, state law requires insurers to offer zero-deductible glass coverage. Always ask your insurer whether a glass deductible waiver applies before paying out of pocket for windshield repair. WebMD

How much is comprehensive car insurance per month in 2026?

Comprehensive coverage averages $200 to $350 per year on its own, or roughly $17–$29 per month. The total cost of full coverage — which includes comprehensive, collision, and liability — averages $244 per month nationally in 2026 according to Experian data. Your actual rate depends on your car’s value, location, deductible, and driving history. HealthlineAn Off Grid Life

When should I drop comprehensive insurance?

The 2026 rule of thumb is: if the annual premium exceeds 10% of your car’s current market value, or if you can comfortably replace the vehicle out of pocket, it often makes financial sense to drop comprehensive coverage. However, if you have an outstanding car loan or lease, your lender requires comprehensive — you don’t have the option to drop it until the loan is paid off. Cleveland Clinic

Does comprehensive insurance cover personal belongings stolen from my car?

No. Your laptop, phone, or other personal items stolen from your vehicle are not covered by comprehensive car insurance. Those fall under your homeowner’s or renter’s insurance policy — typically with a deductible. Check your renters or homeowners policy to see what coverage applies.

You may also like: What Is Compound Interest?