Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, legal, or insurance advice. Rates shown are averages compiled from third-party sources and will vary based on your personal driving profile, location, vehicle, and insurer. Always obtain personalised quotes before making coverage decisions.

California plays by different rules when it comes to car insurance — and if you don’t know those rules, you’re almost certainly overpaying.

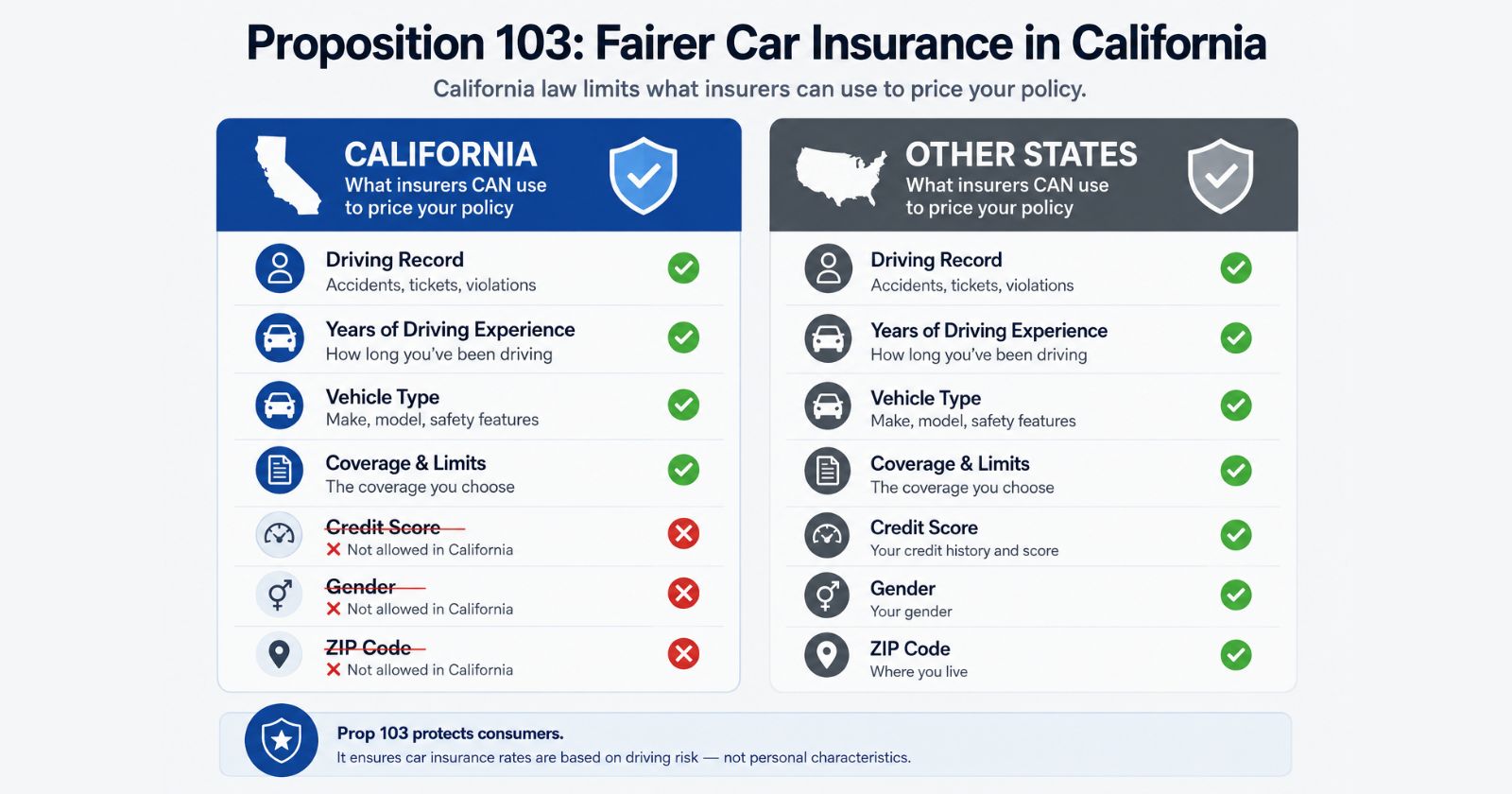

Most states allow insurers to price your policy based on your credit score, gender, and ZIP code. California bans all three as primary rating factors under Proposition 103, passed in 1988. That changes the entire competitive landscape: the factors that make someone expensive to insure in Texas can be completely irrelevant to your California premium. The factors that matter most here — your driving record, annual mileage, and years of driving experience — are almost entirely within your control.

California also isn’t cheap. Despite Prop 103’s consumer protections, full-coverage policies average between $150 and $249 per month depending on the source and driver profile analysed. The state’s high repair costs, dense urban traffic, elevated theft rates, and a 20%-plus uninsured driver rate all push premiums above the national average. The state approved more than 30 rate increases between 2023 and 2025 alone.

But the spread between the cheapest and most expensive insurer for the same California driver can exceed $144 per month for identical coverage — more than $1,700 per year. This guide tells you exactly who is cheapest in 2026, how the state’s unique rules affect your premium, and what you can do right now to reduce what you pay.

1. What California Drivers Actually Pay in 2026

Rate data for California varies across sources because each uses different driver profiles, coverage specifications, and ZIP code mixes. Here’s an honest overview across the main data sources analysed in June 2026:

| Coverage Type | Average Monthly | Average Annual |

|---|---|---|

| Minimum liability only | $39–$75/month | $470–$1,055/year |

| Full coverage (source range) | $113–$249/month | $1,358–$2,989/year |

| State average (Insure.com) | ~$259/month | $3,106/year |

| State average (ValuePenguin) | $221/month | $2,652/year |

| State average (MoneyGeek) | $155/month | $1,860/year |

The wide range between sources reflects different driver profiles. MoneyGeek uses a 40-year-old with a clean record and 100/300/100 liability limits; Insure.com uses a broader cross-section. The takeaway: a 35–40-year-old with a clean record can realistically find full coverage in the $113–$150/month range with the right insurer. Drivers younger, older, or with incidents on their record will pay more.

California’s full-coverage average is modestly above the national average — roughly 5–9% depending on the analysis — despite the consumer protections of Prop 103. Higher vehicle repair labour rates, dense metro traffic, and a high uninsured driver rate (around 20%) all push premiums up even under regulatory oversight.

2. Proposition 103: The California Law That Changes Everything

This is the section you won’t find in most car insurance guides — and it’s the most important thing to understand before shopping for coverage in California.

Proposition 103, passed by California voters in 1988, fundamentally restructured how auto insurance is priced in the state. Its core provisions:

What insurers CANNOT use as primary rating factors in California:

- Credit score or credit history

- Gender

- ZIP code or neighbourhood

- Education level

- Occupation or employment status

What insurers MUST use as the three mandatory primary rating factors:

- Driving safety record (your most important factor by far)

- Annual miles driven

- Years of driving experience

What else Prop 103 requires:

- Rate increases above 7% require advance approval from the California Department of Insurance

- Every insurer must offer a Good Driver Discount of at least 20% to qualifying drivers (those with no more than one moving violation in the past three years and no at-fault accidents)

- Public participation in rate hearings is permitted

- The Insurance Commissioner is an elected position, not an appointed one

Why this matters for you:

If you have poor credit, Prop 103 is enormously beneficial — your credit score simply doesn’t affect your California premium. The same driver with a 580 credit score and a clean driving record pays the same as a driver with an 800 credit score and the same profile.

If you have a clean driving record, California’s mandatory 20% Good Driver Discount means you’re entitled to a significant rate reduction that insurers must legally provide.

If you’ve had incidents on your record, your driving history carries even more weight in California than in most states, because it’s doing the work that credit and ZIP code do elsewhere. A single DUI or at-fault accident can have an outsized impact on your California premium.

Prop 103 also created the California Low Cost Automobile Insurance Program (CLCA) — a subsidised programme for income-eligible drivers covered in detail in Section 9.

3. Cheapest Car Insurance Companies in California: Ranked

Based on 2026 rate data from NerdWallet, ValuePenguin, MoneyGeek, Insure.com, and QuoteMoto, here are the consistently cheapest insurers for California drivers with clean records.

GEICO — Overall Cheapest for Most Drivers

GEICO tops the cheapest rankings in the majority of 2026 California analyses. NerdWallet puts GEICO at $113/month ($1,358/year) for full coverage and $49/month for minimum coverage for a 35-year-old with a clean record. MoneyGeek cites $90/month for full coverage and $39/month for minimum coverage for a 40-year-old. Insure.com’s broader cross-section puts GEICO at $170/month ($2,039/year) — still the cheapest in their dataset.

The reason GEICO prices this low in California: it sells direct online without captive local agents, removing a significant overhead cost from every policy. It’s also fully available in California — both online and through its mobile app.

Best for: Clean-record drivers of all ages who want the lowest available rate. Digital-first customers. Young adults in their 20s and 30s. Teens (GEICO is the cheapest teen insurer in California at around $430/month for a standalone policy, or less on a parent’s policy).

Limitation: Fewer add-on coverage options than regional specialists like Mercury. No in-person agent offices for face-to-face service.

Wawanesa — Best Customer Service (California Only)

Wawanesa is a California-focused regional insurer that has topped J.D. Power’s auto insurance customer satisfaction survey in California every year since 2020. It’s the best-rated insurer in the state for claims handling and service quality, and offers competitive rates particularly in Northern California. Wawanesa also uniquely covers custom and aftermarket parts following a covered loss — something most major carriers exclude.

Best for: Drivers who prioritise claims experience and customer service over the absolute lowest premium. Northern California residents. Drivers who have had a bad claims experience with a national carrier.

Limitation: California-focused — less relevant if you move out of state. Rate competitiveness varies more by region than national carriers.

Mercury Insurance — Best for DUI/High-Risk and Bundling

Mercury Insurance is a California-founded regional carrier with the most competitive rates for drivers with a DUI on their record. It also offers some of the best bundling discounts in the state — up to 15% on auto and 20% on homeowners when combined. Mercury’s RealDrive pay-per-mile product is one of the better usage-based options available in California for low-mileage drivers.

Best for: Drivers with a DUI or at-fault accident who need competitive rates. Homeowners who can bundle. Low-mileage drivers interested in pay-per-mile pricing.

Limitation: Customer satisfaction scores trail Wawanesa and USAA. Claims experience is mixed in independent surveys.

USAA — Best for Military Families

For active-duty service members, veterans, and eligible family members, USAA remains the highest-rated insurer in California for both price and customer satisfaction. It combines competitive rates with the strongest claims and service scores of any major carrier nationally.

Best for: Anyone with military eligibility — this should be the first quote you get if you qualify.

Limitation: Eligibility strictly restricted to the military community.

Progressive — Best for Telematics Savings and High-Risk Drivers

Progressive is competitive for clean-record California drivers and distinctly the best choice for drivers with accidents, tickets, or DUIs who want a path to lower rates over time. The Snapshot telematics programme can reduce premiums by 10–30% after a 90-day monitoring period for drivers who demonstrate safe behaviour. Progressive also leads on rideshare endorsements in California alongside Mercury and State Farm.

Best for: Drivers with a blemished record who want to earn their way to lower rates. Rideshare drivers (Uber, Lyft). Tech-forward drivers comfortable with telematics.

Limitation: Not the cheapest clean-record option. Snapshot can increase rates if the monitoring reveals risky driving habits.

AAA — Best Regional Option for Northern California

AAA offers a strong combination of price and service in Northern California specifically, though rates in Southern California are generally less competitive. The membership also provides genuine value through roadside assistance, travel discounts, and other benefits that can partially offset the membership fee.

Best for: Northern California residents, particularly those who value AAA’s roadside service. Drivers who want a single provider for auto insurance and roadside assistance.

Limitation: Membership required. Rates in Southern California (LA, San Diego) are less competitive than in Northern California.

Summary Comparison Table

| Insurer | Full Coverage (monthly) | Best For | Availability |

|---|---|---|---|

| GEICO | ~$90–$143/month | Overall cheapest, teens, digital users | All drivers |

| Wawanesa | Competitive | Best customer service, NorCal | All drivers |

| Mercury | Competitive | DUI, bundling, pay-per-mile | All drivers |

| USAA | Low | Military families | Military only |

| Progressive | Moderate | High-risk, telematics, rideshare | All drivers |

| AAA | Moderate | NorCal, roadside coverage | Members |

| State Farm | $158–$248/month | Bundling, agent access | All drivers |

| Allstate | $192–$310/month | Accident forgiveness, agent network | All drivers |

| Farmers | Highest | Wide agent network | All drivers |

4. Best for Specific Driver Profiles

Teens and Young Drivers (Under 25)

California teen drivers pay some of the highest rates in the country — averaging $3,195–$3,439 per year for standalone policies depending on gender (though California cannot use gender as a primary factor, age remains significant). GEICO is the cheapest insurer for California teens at around $430/month ($5,166/year) for standalone full coverage. Mercury is second. The cheapest route for most young drivers is remaining on a parent’s policy, where shared risk significantly lowers the per-driver cost.

Drivers After a DUI

California applies DUI consequences particularly harshly in insurance pricing because driving record carries extra weight under Prop 103. Mercury offers the most competitive rates for DUI-affected drivers. Progressive’s Snapshot telematics programme is the best tool for rebuilding a lower rate over time after a DUI, as it allows drivers to demonstrate improved behaviour. Note: California requires SR-22 filing following a DUI, which must be maintained for three years.

Drivers After an At-Fault Accident

GEICO and Progressive are the most competitive for post-accident drivers in California. Progressive’s Snapshot programme gives drivers with incidents a genuine route to lower premiums through demonstrated safe driving.

Senior Drivers (Over 65)

Senior drivers in California pay above average but less than teenagers. Safeco offers a notable discount for drivers 55 and older who complete an approved defensive driving course. GEICO remains competitive for seniors with clean records, and Wawanesa’s service reputation makes it particularly attractive for seniors who value responsive claims handling.

Low-Mileage Drivers

California law explicitly allows mileage-based rating — an important point under Prop 103 that many drivers underutilise. Mercury’s RealDrive pay-per-mile product and Progressive’s Snapshot both offer meaningful savings for drivers covering fewer than 7,500 miles per year. If you work from home, have a second car, or simply drive infrequently, usage-based pricing is worth exploring.

Rideshare Drivers (Uber, Lyft)

Progressive, State Farm, and Mercury are the three major California carriers that offer rideshare endorsements. Mercury’s endorsement — at around $0.90/day — is the lowest-priced among California’s top carriers. Without a rideshare endorsement, your personal auto policy will not cover damage during the period you’re logged into the app waiting for a ride request, which is a significant and often-overlooked coverage gap.

5. California’s Minimum Coverage Requirements

California requires all drivers to carry minimum liability insurance of:

- $30,000 bodily injury liability per person

- $60,000 bodily injury liability per accident

- $15,000 property damage liability per accident

This is known as 30/60/15 coverage. Note: some sources still reference the older 15/30/5 limits, which were the minimum before California’s update. As of 2026, any policy written below 30/60/15 limits is non-compliant. If you’re carrying a legacy minimum-limit policy, your insurer may have auto-upgraded you (and re-priced you) at renewal. If you’re unsure, check your declarations page.

California is an at-fault state — the driver determined to be responsible for an accident is liable for bodily injury and property damages incurred by others, up to your policy’s limits.

Why minimum coverage is almost never enough: In a serious accident involving hospitalisation or a multi-vehicle pile-up, $30,000 per person and $15,000 in property damage can be exhausted quickly. Medical bills alone can exceed $30,000 for a single hospitalised victim. If damages exceed your coverage limits, you’re personally liable for the difference. Most insurance professionals recommend at least 100/300/100 in liability — and if you own a home or have significant assets, higher limits still.

California’s uninsured driver reality: Around 20% of California drivers carry no insurance — the eighth-highest rate nationally. This makes uninsured/underinsured motorist (UM/UIM) coverage particularly valuable in California, even if it’s not legally required. Without it, being hit by one of those uninsured drivers means bearing your own injury and vehicle costs out of pocket.

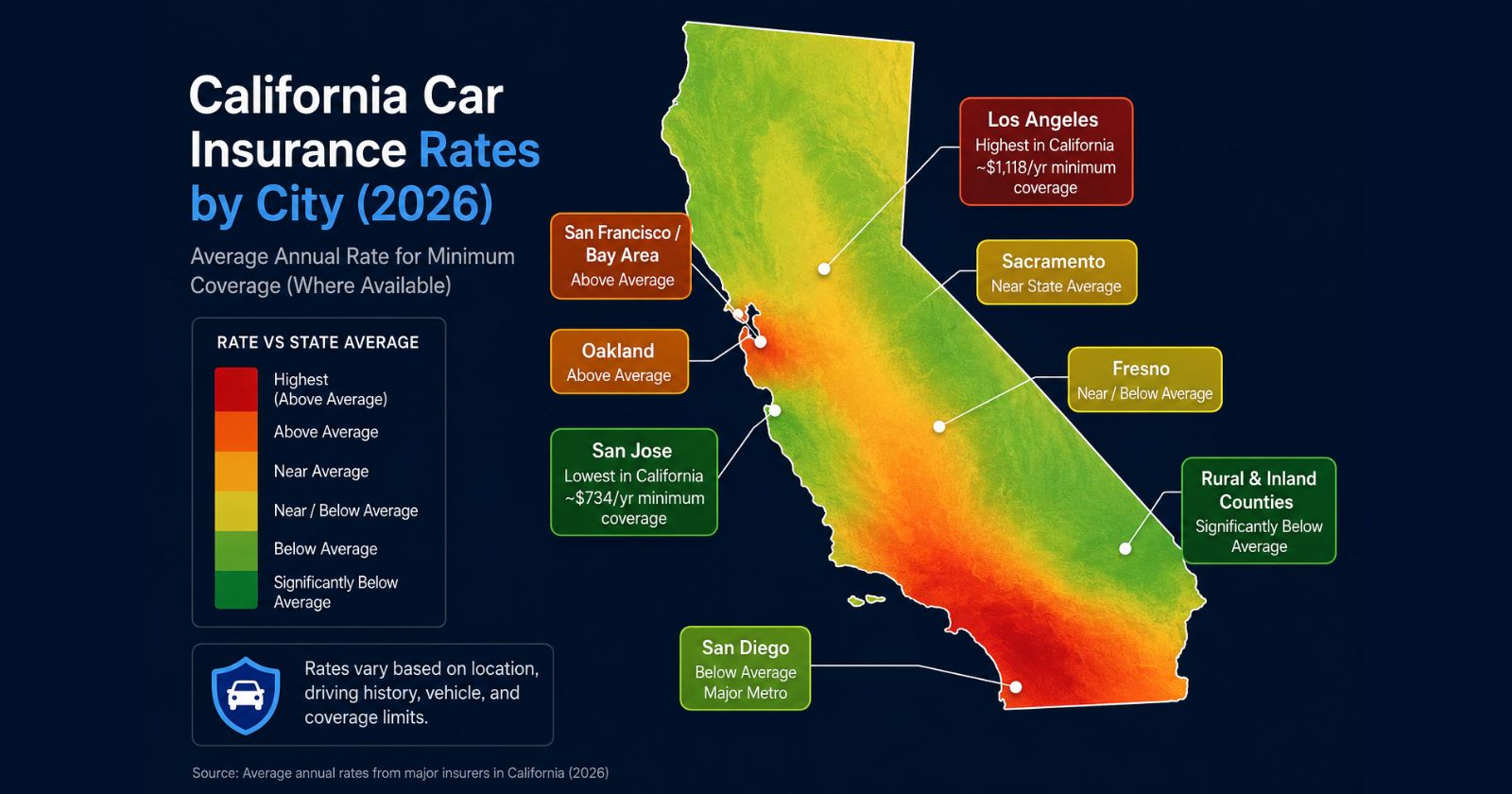

6. How Your City Affects Your Rate

Despite Prop 103’s restrictions on using ZIP code as a primary rating factor, location still influences your California premium through traffic density, theft rates, and wildfire-risk classifications. Here’s how major California metros compare:

| City / Area | Rate vs State Average | Key Drivers |

|---|---|---|

| Los Angeles | Highest minimum coverage in state (~$1,118/yr) | High traffic density, very high auto theft, expensive vehicle mix, high litigation |

| San Francisco / Bay Area | Above average | High vehicle values, congestion, above-median labour repair rates |

| Oakland | Above average | High theft rate, dense urban area |

| San Diego | Below average for a major metro | Lower accident frequency than LA; Progressive charges $33/month less here vs LA |

| Sacramento | Near state average | Moderate density, lower vehicle values than coastal metros |

| Fresno | Near or below average | Lower density, lower vehicle values |

| San Jose | Lowest minimum coverage rate in California (~$734/yr) | Lower accident frequency despite tech-area income and vehicle values |

| Rural/inland counties | Significantly below average | Low traffic density, fewer claims, lower theft exposure |

The $33/month gap between Los Angeles and San Diego with the same insurer (Progressive) illustrates how meaningfully city matters even under Prop 103’s restrictions. Within cities, wildfire-risk ZIP codes in inland areas can also push comprehensive coverage rates higher than the city-wide average.

7. The Key Factors That Set Your Premium in California

California’s Prop 103 framework means your rate is built differently here than in almost any other state.

The three mandatory primary factors (by law):

1. Driving safety record. This is the single most important factor in California — and carries more weight here than in most states because credit and ZIP code can’t compensate for it. At-fault accidents, speeding tickets, DUIs, and other violations all increase your premium significantly. The Good Driver Discount (mandatory at 20% minimum) makes a clean record especially valuable — it’s a legally required reward that you either qualify for or you don’t.

2. Annual miles driven. California law permits mileage-based rating, and most insurers use it. Drivers who commute long distances pay more. Low-mileage drivers can access meaningful discounts, particularly through usage-based and pay-per-mile programmes.

3. Years of driving experience. Experience behind the wheel is distinct from age — a 30-year-old who has held a licence for 12 years is priced differently than one who received their licence at 25. The more documented driving experience you have, the lower this factor pushes your rate.

Additional permitted factors (secondary):

4. Vehicle type. High-value vehicles, sports cars, and models with expensive or hard-to-source parts attract higher premiums. Safety features, anti-theft systems, and vehicle age all factor in. California had the fifth-highest rate of vehicle theft per 100,000 people nationally in 2023, making theft risk a real factor in comprehensive pricing.

5. Annual mileage (again, in more detail). Some insurers use self-reported mileage; others verify through telematics. High-mileage drivers pay proportionally more.

6. Age. Teens and seniors pay more. Rates tend to decline through middle age and rise again after around 70. California cannot use gender as a primary factor, but age remains a permitted variable.

What California insurers CANNOT price on:

Credit score, gender, ZIP code as a primary factor, education level, or occupation. This is a significant consumer protection and meaningfully different from the 46 states that allow credit-based pricing.

8. How to Lower Your Car Insurance Rate in California

Get five quotes, not two. The rate spread between the cheapest and most expensive carrier for the same California driver averages 87% in 2026 sample data — that’s not a typo. The difference in annual premium between GEICO and Farmers for the same driver profile can exceed $2,400 per year. Loyalty pricing, where carriers quietly raise long-term customers’ rates at renewal, costs the average California driver an estimated $487 per year. Annual shopping is the single highest-return habit available to California drivers.

Claim your mandatory Good Driver Discount. If you’ve had no more than one moving violation in the past three years and no at-fault accidents, California law requires insurers to offer you a discount of at least 20%. This should already be applied to your quote — but verify it is. If you’ve recently cleared an old violation from your record, re-quote immediately.

Bundle home or renters insurance. Mercury, State Farm, and Allstate all offer 12–22% multi-policy discounts in California for bundling auto with home insurance. GEICO and Progressive offer 5–12% bundles. If your auto and home policies are with different carriers, pricing a bundle is worth 15 minutes.

Use telematics if you’re a safe driver. Progressive’s Snapshot and Allstate’s Drivewise can reduce clean-record premiums by 10–30% after a 90-day monitoring period. The key condition: these programmes monitor your actual driving. If you brake hard frequently, drive late at night, or use your phone while driving, telematics can raise your rate rather than lower it.

Pay your policy in full. Wawanesa, Mercury, and Progressive all offer 6–10% paid-in-full discounts that monthly billing customers miss entirely. On a $1,800 annual policy, a 10% discount saves $180 immediately with no other change to your coverage.

Drop full coverage on low-value older vehicles. Once your vehicle is worth less than $4,000–$5,000 and you own it outright, carrying collision and comprehensive coverage can cost more per year than the maximum payout after the deductible. Check your vehicle’s current Kelley Blue Book value before renewal and run the maths.

Increase your deductible. Moving from a $200 to a $500 deductible can reduce collision and comprehensive costs by up to 30%, according to the Insurance Information Institute. Only do this if you can genuinely cover the higher deductible from savings.

Look for every available discount. Beyond the standard safe-driver discount, California insurers offer discounts for good students, anti-theft devices, defensive driving courses (especially valuable for seniors), paperless billing, and vehicles with advanced safety features like automatic emergency braking. Ask your insurer specifically what discounts you aren’t currently receiving.

Re-shop every 12 months. California rate filings change quarterly. The cheapest carrier in 2024 is frequently not the cheapest in 2026. Setting a calendar reminder to get three to five competing quotes at every renewal is the cheapest ongoing saving strategy available.

9. The California Low Cost Automobile Insurance Program

One California-specific option that most articles skip: the California Low Cost Automobile Insurance Program (CLCA).

Created under Prop 103, the CLCA provides subsidised liability-only insurance for income-eligible good drivers who cannot otherwise afford coverage. To qualify:

- Household income must be at or below 250% of the federal poverty level

- Clean driving record for the past three years (no more than one point on your record)

- At least 19 years old

- Vehicle valued at $25,000 or less

CLCA policies provide minimum liability coverage at rates significantly below standard market prices. If you or a household member may qualify, the California Department of Insurance website has an eligibility tool. This is a legitimate state programme worth checking before assuming minimum coverage at market rates is the only option.

10. Full Coverage vs Minimum Coverage: Which Do You Need?

Choose minimum coverage (30/60/15) if:

- Your vehicle is paid off and worth less than $4,000–$5,000

- You could replace or significantly repair the vehicle from savings if it were totalled or stolen

- You primarily need liability protection for harm you cause to others in an accident

Choose full coverage if:

- You have an auto loan or lease (lenders legally require it until the vehicle is paid off)

- Your vehicle is worth more than $8,000–$10,000

- You couldn’t replace the vehicle from savings if it were totalled or stolen

- You live in a high-theft area (LA, Oakland, Fresno — California had the fifth-highest vehicle theft rate nationally)

- You’re in a wildfire-risk zone where comprehensive coverage pays for fire damage

One add-on worth serious consideration regardless of tier: Given that approximately 20% of California drivers are uninsured, UM/UIM coverage is a meaningful protection even on a minimum-coverage policy. It pays for your injuries and vehicle damage when you’re hit by an uninsured or underinsured driver — a genuinely common risk in California.

11. How to Compare Quotes the Right Way

The process matters almost as much as the comparison itself. Three common mistakes: comparing different coverage levels, assuming online comparison tools cover all carriers, and choosing on price without checking claims satisfaction.

Step 1: Lock your coverage specifications first. Decide on your liability limits and deductibles before requesting a single quote. Every quote must be at identical specs — otherwise you’re comparing different products at different prices and the comparison is meaningless.

Step 2: Get five quotes, not two or three. Include GEICO, Mercury, Wawanesa, Progressive, and your current insurer as a baseline. Use the California Department of Insurance’s comparison tool (available on their website) alongside direct insurer sites.

Step 3: Verify the Good Driver Discount is applied. If you qualify as a Good Driver under California law, confirm that each quote includes the mandatory minimum 20% discount. If it isn’t showing on your quote, ask explicitly.

Step 4: Check J.D. Power California scores and NAIC complaint ratios. Price is one dimension; claims handling is another. J.D. Power surveys California specifically. The NAIC complaint ratio (publicly available) shows how each insurer handles disputes relative to its market share. A carrier that’s $15/month cheaper but has twice the complaint ratio may not be the better choice.

Step 5: Ask about every available discount on each quote. Don’t assume discounts are pre-applied. Ask specifically: “What discounts am I not currently receiving?”

Step 6: Repeat every 12 months. California rate filings change quarterly. Annual shopping is a meaningful and repeatable saving strategy, not a one-time exercise.

12. Frequently Asked Questions

Who has the cheapest car insurance in California in 2026?

GEICO is the cheapest insurer for most California drivers in 2026 according to the majority of major analyses, with full-coverage rates ranging from $90 to $143/month for a clean-record driver depending on the profile used. USAA is cheaper for military-affiliated drivers but is not available to the general public. Wawanesa and Mercury are competitive alternatives, particularly for bundling or high-risk situations.

Does California use credit scores for car insurance?

No. California Proposition 103, passed in 1988, prohibits insurers from using credit scores as a primary rating factor for auto insurance. Your rate is based primarily on your driving record, annual mileage, and years of driving experience. California is one of only three states — alongside Hawaii and Massachusetts — that ban credit-based auto insurance pricing.

What is the minimum car insurance required in California in 2026?

California requires 30/60/15 liability coverage: $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $15,000 for property damage. If you’re carrying a policy with lower limits from before this requirement took effect, it may be non-compliant — check your declarations page.

What is the California Good Driver Discount?

Under Proposition 103, every California insurer must offer a discount of at least 20% to drivers who qualify as “Good Drivers” — defined as those with no more than one minor violation in the past three years and no at-fault accidents. This discount is mandatory and must be offered regardless of which insurer you use. It’s one of the most valuable rate protections in the state and applies across all major carriers.

Why is car insurance expensive in California despite Prop 103?

Several factors push California rates above the national average despite consumer protections. Around 20% of California drivers are uninsured, which raises costs for insured drivers. Vehicle repair labour rates in California run above the national median. Major metros including Los Angeles and San Francisco have high accident frequency, vehicle theft rates, and expensive vehicle mixes. California also has a high litigation rate, which increases liability claim costs. And rate increase approvals, while regulated, don’t prevent increases — they just require regulatory sign-off.

What is the CLCA programme?

The California Low Cost Automobile Insurance Program provides subsidised liability insurance for income-eligible drivers who meet the state’s Good Driver criteria. Household income must be at or below 250% of the federal poverty level. Eligible drivers can access minimum liability coverage at below-market rates through the California Department of Insurance’s CLCA portal.

How much can I save by shopping around for car insurance in California?

Significantly. The spread between the cheapest and most expensive major insurer for the same California driver averages 87% in 2026 data — meaning the most expensive carrier can charge nearly double what the cheapest charges for identical coverage. The average California driver who actively shops around saves over $400 per year compared to staying with their current insurer at renewal.

Should I drop full coverage on my older car in California?

Generally yes if your vehicle is worth less than $4,000–$5,000, you own it outright, and you have savings to cover replacement or major repairs. Run the specific maths: if your annual collision and comprehensive premium exceeds 10% of your vehicle’s current Kelley Blue Book value, the coverage is likely not cost-effective. The exception: if you live in a high-theft area like Los Angeles or Oakland, the comprehensive portion (which covers theft) may be worth retaining separately even on a lower-value vehicle.

For more guides on protecting your finances with practical, data-driven strategies, explore InfoBrave’s finance and informative guides.

You may also like: Best Car Insurance Rates in Texas 2026: The Complete Guide to Saving Money in the Lone Star State