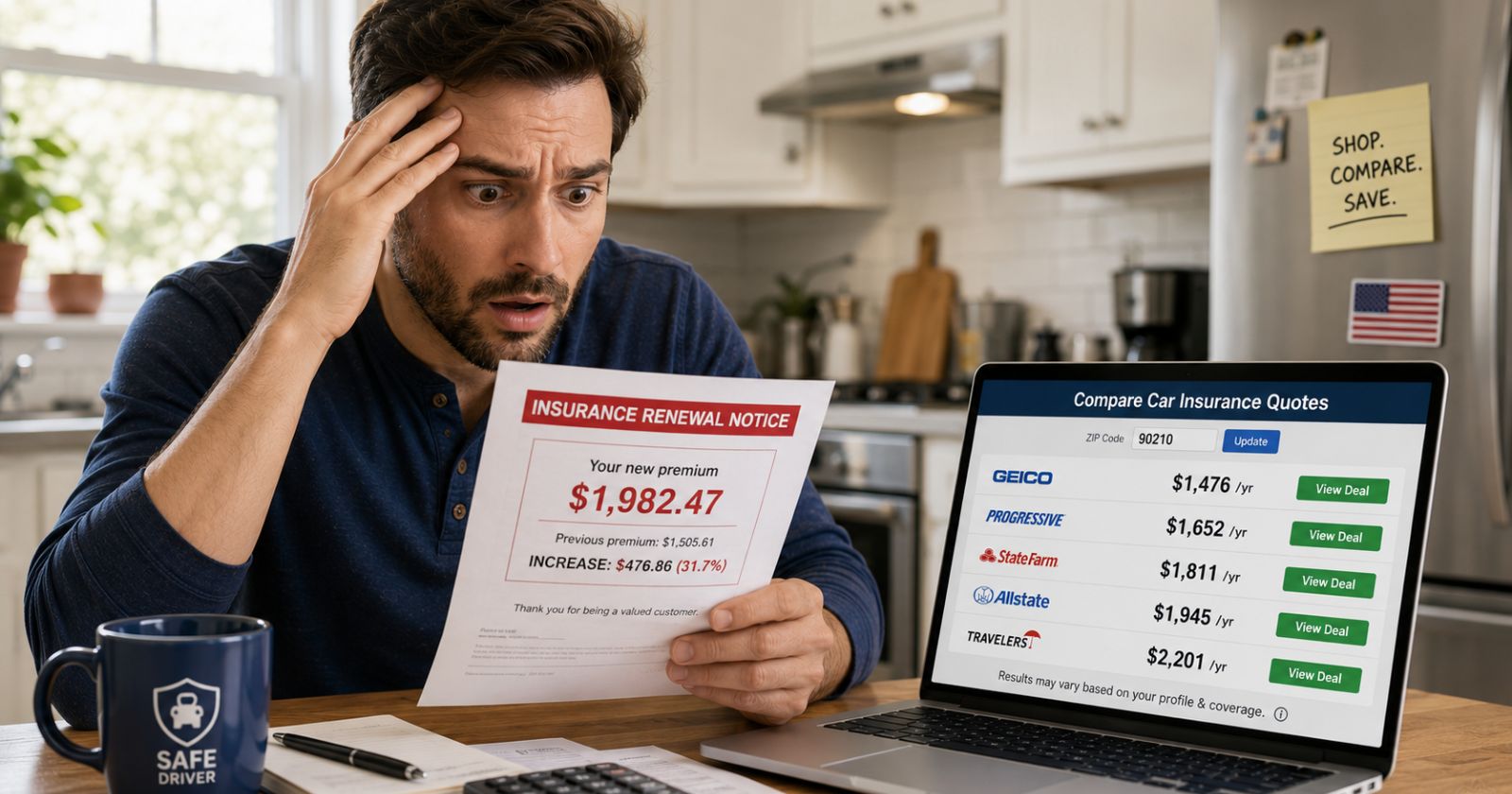

You opened your renewal notice. The number went up — again. Maybe it jumped $30 a month. Maybe it jumped $80. Either way, you didn’t have an accident. You didn’t get a ticket. Nothing changed — so why on earth is your car insurance so high?

Here’s the answer nobody gives you upfront: your rate is probably being hit by two completely separate forces at the same time. Industry-wide cost increases that affect every driver in America. And personal factors specific to your profile that your insurer quietly adjusts each renewal.

Understanding which category is hitting you — and how hard — is the first step to actually doing something about it.

This guide breaks down all 11 real reasons your car insurance is high in 2026, then gives you a practical, dollar-specific action plan to bring it down — without sacrificing the coverage you actually need.

Disclaimer: This article is for informational purposes only and does not constitute insurance or financial advice. Insurance pricing varies significantly by state, insurer, and individual profile. Always consult a licensed insurance agent for advice specific to your situation.

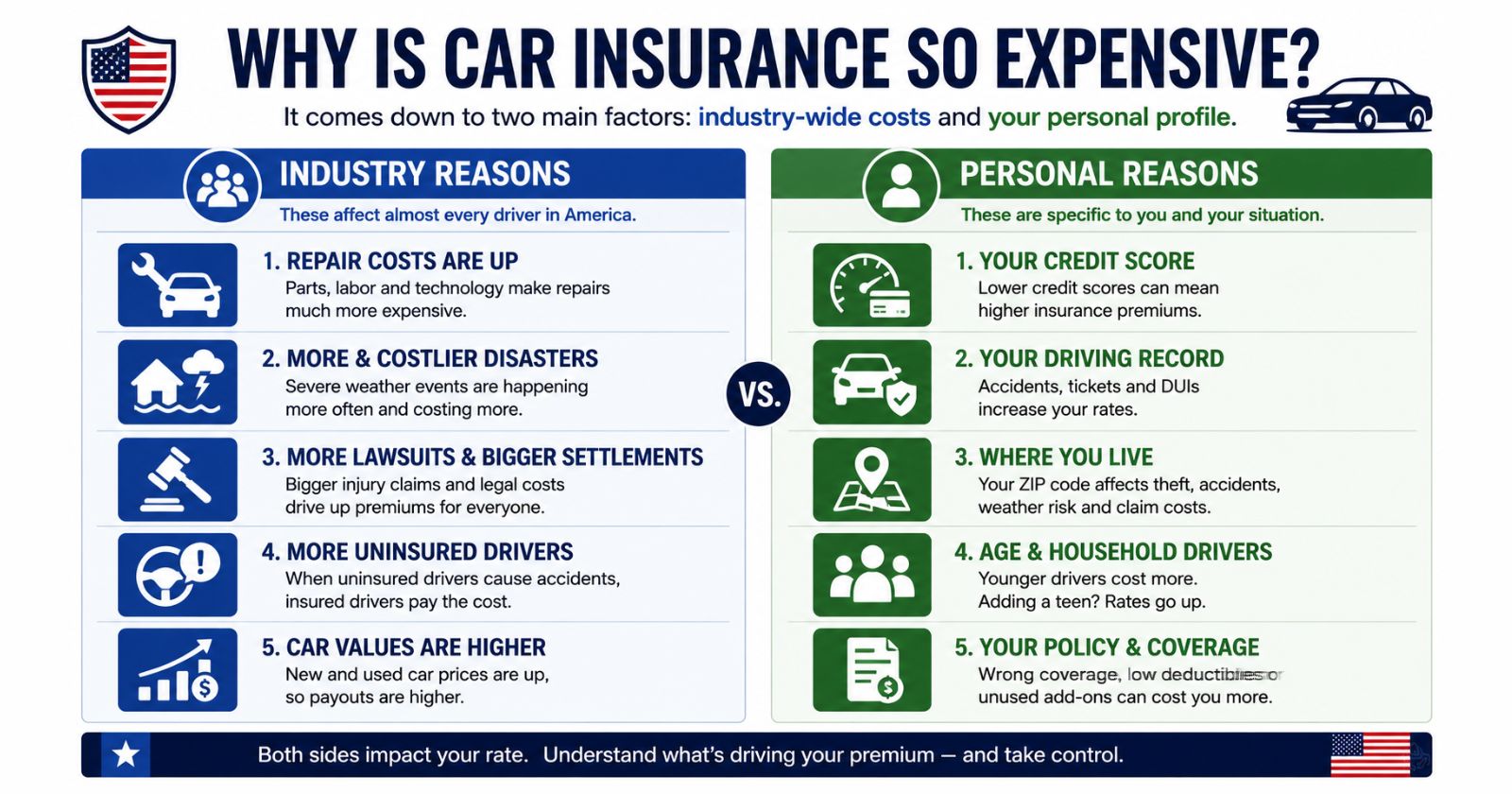

1. The Short Answer: Two Types of Reasons

Before we get into the list, it helps to understand the structure.

Type 1 — Industry reasons: Things happening across the entire insurance market that are raising rates for almost every American driver regardless of their personal record or behavior.

Type 2 — Personal reasons: Factors specific to you, your car, your location, and your policy that are making your individual rate higher than it needs to be.

Nearly two-thirds of drivers saw their rates increase in the past 12 months. The most common experience was a 5–10% hike. Nearly 74% of respondents blame general inflation for rising rates — but a significant share point to insurers themselves, saying the drive to increase profits is behind higher premiums. Grow Forage Cook Ferment

The frustrating truth: both types are real, both are happening simultaneously in 2026, and they require different responses. Let’s go through all 11.

2. Industry-Wide Reasons Your Rate Is High

These are the reasons your rate went up even though you did everything right.

Reason 1: Repair Costs Exploded — and Haven’t Fully Come Back Down

This is the biggest driver of the rate increases that started in 2022 and are still working their way through the system in 2026.

The cost of vehicle repairs and maintenance increased by more than 36% between 2021 and 2025. Repair costs and bodywork each rose by just over 13%. Semrush

Why? Modern vehicles are computers on wheels. A bumper that used to cost $400 to replace now costs $1,800 because it contains parking sensors, cameras, and radar emitters that all need recalibrating after replacement. A windshield that used to be a simple glass swap now requires ADAS sensor recalibration at $300–$800 on top of the glass itself.

The 2024 Auto Insurance Trends Report from LexisNexis Risk Solutions found that the severity of material damages rose by 47% since 2020. Total loss claims increased by 29%. ALM Corp

When every claim costs more to settle, every driver’s premium goes up — regardless of whether they personally filed a claim.

Reason 2: Your Car Is Worth More Than It Used to Be

In 2025, the average price of a used car was about 23% higher than it was in 2019. Semrush

Insurance pays out based on your vehicle’s actual cash value. When car values rise — as they did dramatically post-pandemic and have remained elevated since — the maximum payout on total loss claims rises with them. That means higher payouts across the industry, which translate directly into higher premiums for everyone.

Car insurance premiums surged dramatically between 2022 and 2024, driven by pandemic-related supply chain disruptions, catastrophic natural disasters, urban theft and increased lawsuits. The nationwide average full coverage is now $2,539 annually — up dramatically from $1,127 just a few years ago. Semrush

Reason 3: Natural Disasters Are Costlier and More Frequent

Climate change is playing a growing role in the insurance industry. In 2026, natural disasters like floods, hurricanes, and wildfires are happening more often, causing a rise in comprehensive insurance claims. The National Oceanic and Atmospheric Administration reported that 2025 saw over 20 billion-dollar weather disasters in the United States alone. Keywords Everywhere

About 27% of drivers say the rising cost of parts and repairs is the culprit for rate increases, while 16% say severe weather is to blame. Organic Facts

If you live in Florida, Texas, California, Oklahoma, or anywhere along the Gulf Coast, your rates reflect not just your personal risk but the elevated regional risk of weather-driven claims. Rates remain high in some states because of a high rate of uninsured drivers and a high volume of vehicle thefts. ALM Corp

Reason 4: More Lawsuits, Bigger Settlements

Insurance companies don’t just pay for repairs — they also pay out bodily injury claims, legal fees, and settlements when accidents result in injuries or fatalities. And those costs have risen sharply.

Bodily injury severity increased by 20% since 2020. Additionally, drivers increasingly turned to attorneys for their claims — meaning settlements are larger and more contested. Hobby Homestead

This trend — sometimes called “social inflation” — means every insurer is paying out more per liability claim than they did five years ago. Those costs are spread across the entire pool of policyholders. Your premium includes a slice of that systemic cost increase even if you’ve never been in an at-fault accident.

Reason 5: More Uninsured Drivers on the Road

When an uninsured driver hits you, your own uninsured motorist coverage (if you have it) or your collision coverage steps in. That means more claims, more payouts — costs borne by insured drivers collectively.

Rates remain high in certain states because of a high rate of uninsured drivers, according to the Insurance Information Institute. States with high uninsured driver rates — including Michigan, Mississippi, Tennessee, and New Mexico — consistently show higher-than-average premiums for everyone, even safe, fully insured drivers. ALM Corp

3. Personal Reasons Your Rate Is High

These are the factors you can actually control or address directly.

Reason 6: Your Driving Record Has Something on It

This one’s obvious — but the duration surprises most people.

At-fault accidents typically impact rates for three to five years, depending on your state and insurer. Standard moving violations affect premiums for three to five years in most states. Serious offenses like DUI can impact rates for five to ten years. Local Search Forum

Most drivers assume a fender-bender from two years ago is “old news.” It almost certainly isn’t. Insurers look at your motor vehicle report (MVR) at every renewal. One at-fault accident from 2023 is likely still costing you meaningfully in 2026.

| Incident | Typical rate impact duration |

|---|---|

| Minor speeding ticket | 3 years |

| At-fault accident | 3–5 years |

| Reckless driving | 5 years |

| DUI / DWI | 5–10 years |

| Serious injury accident | Up to 10 years |

The good news: once these age off your record, your rate should drop at renewal — if you proactively get new quotes rather than passively accepting the renewal.

Reason 7: Your Credit Score Is Dragging Your Rate Up

This is the factor most people don’t know about — and one of the most impactful.

In many U.S. states, insurers use a “credit-based insurance score.” Better credit equals a lower risk profile, which equals a lower premium. Improving credit can reduce premiums by 15–40%. Zapier

Insurers have found through decades of data that credit score correlates strongly with the likelihood of filing claims. Drivers with poor credit are statistically more likely to file claims — so insurers charge them more.

Important exceptions: Some states like California, Hawaii, and Massachusetts restrict or prohibit credit scoring for auto insurance. If you live in one of these states, your credit score cannot affect your auto insurance rate. Zapier

If you’re in a state that allows it and your credit score is below 670, improving it is one of the highest-ROI moves you can make for your insurance costs.

Reason 8: Where You Live — Down to Your ZIP Code

Your address affects your rate more than most people realise. Insurers don’t just look at your state — they look at your specific ZIP code and factor in:

- Local theft rates — A high-theft neighbourhood raises your comprehensive rate

- Local accident rates — Dense urban areas with heavy traffic see more frequent claims

- Weather risk — Hail-prone regions, flood zones, and wildfire areas command higher rates

- Average lawsuit costs — States with higher litigation costs (Florida, Michigan, New Jersey) pass those costs to all drivers

Areas with high rates of natural disasters or litigation see more frequent insurance rate increases due to high costs per claim. An Off Grid Life

If you’ve recently moved — even within the same city — update your garaging address with your insurer immediately. An outdated address can mean you’re being charged for a risk profile that no longer matches your reality.

Reason 9: Your Age or Household Members

Drivers under 25 pay higher rates due to the statistically higher rate of collisions. Teen drivers pay the highest rates, and then rates decrease steadily through your early 20s as risk decreases. Semrush

If you added a teen driver to your policy recently, that explains a significant portion of your increase. But this also works in reverse — once a young driver on your policy turns 25 or leaves the household, make sure your insurer knows. Rates don’t always adjust automatically.

Older drivers can also see rates creep up after age 70 as some insurers adjust for increased accident risk.

Reason 10: The Loyalty Penalty Nobody Warns You About

This is the content gap almost no article covers honestly.

Don’t assume your current insurer is giving you the best rate — loyalty is often not rewarded in auto insurance. In fact, the opposite is frequently true. Many insurers offer their most competitive rates to attract new customers, while gradually raising rates on existing policyholders who are unlikely to shop around. Local Search Forum

Despite rate hikes, 87% of drivers did not switch insurers in the past year. Insurers know this. Staying with the same company for five or ten years without getting competing quotes is one of the most expensive passive habits a driver can have. ALM Corp

The fix is simple — and free. Get quotes from three to five other insurers at every renewal. If your current insurer is still competitive, stay. If they’re not, switch. The average driver who actively shops saves $200–$800 annually.

Reason 11: Your Coverage Hasn’t Been Reviewed in Years

Your life has changed. Your policy probably hasn’t kept up.

Common examples of stale coverage costing you money:

- You’re still paying for rental reimbursement even though you now have a second car

- Your collision deductible is $250 from when you first bought the car and couldn’t afford a higher one — but now you have an emergency fund and could handle $1,000

- You’re carrying full coverage on a car worth $4,000 — potentially more than the 10% rule supports

- You have roadside assistance in your policy and also pay for AAA or a credit card benefit that includes it

- Your annual mileage estimate is wrong — you work from home now but your policy still shows your old commute distance

Review your coverage annually — remove unnecessary add-ons such as rental reimbursement if you have another car. Consider whether your coverage limits and deductibles still match your current financial situation. SEOmator

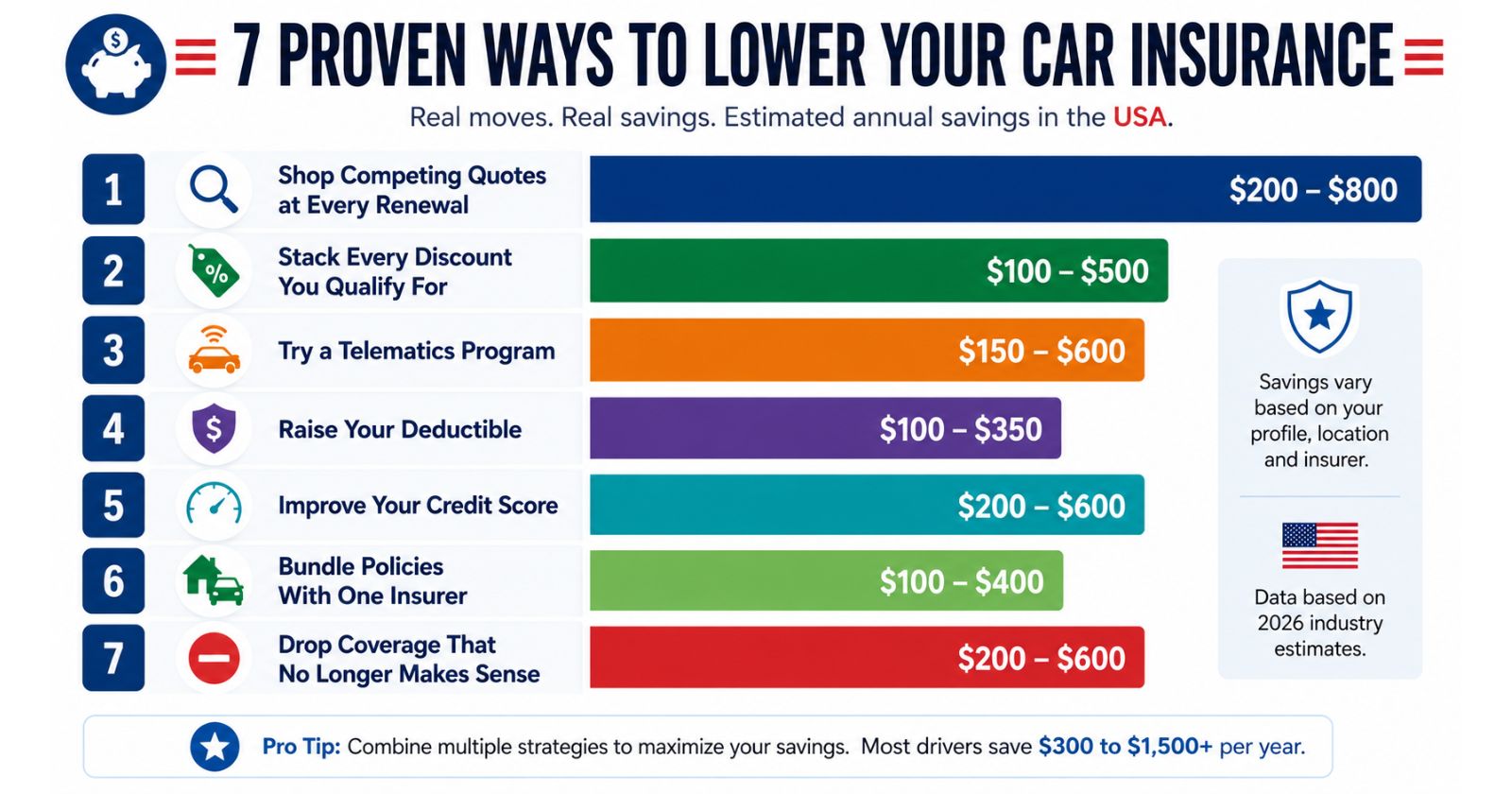

4. How to Actually Lower Your Car Insurance in 2026

Now the practical part. Here are the moves that produce real savings — with real dollar estimates for each.

Move 1: Shop Competing Quotes at Every Renewal

Potential savings: $200–$800/year

Comparing auto insurance quotes can save $200 to $800 annually. Most drivers qualify for better rates at a competitor without realising it. Asinsight

Set a calendar reminder 30 days before your renewal date. Get quotes from at least three to five insurers using identical coverage specs (see the framework below). Do this every single year — not just when you notice a rate spike.

Move 2: Stack Every Discount You Qualify For

Potential savings: $100–$500/year

Most drivers are missing multiple discounts because they never asked. Common discounts worth checking:

| Discount | Typical savings |

|---|---|

| Bundling home + auto | 15–25% |

| Multi-vehicle | 10–20% |

| Good student (B average+) | 10–25% |

| Defensive driving course | 5–10% |

| Low mileage / pay-per-mile | Up to 30% |

| Autopay | 3–5% |

| Paperless billing | 2–5% |

| Anti-theft device | 5–15% |

| Affinity (employer, alumni, military) | 5–15% |

Ask your insurance agent to run through every available discount at your next renewal. Most people have never been proactively offered the full list. ScienceDirect

Move 3: Try a Telematics Program

Potential savings: $150–$600/year (up to 40%)

Telematics programs track your driving habits and reward safe behaviour, cutting premiums by $150 to $600 or up to 40% off your rates. Programs like State Farm’s Drive Safe and Save and Progressive’s Snapshot monitor factors like hard braking, speed, and phone use. Asinsight

If you’re a genuinely safe driver — smooth acceleration, no hard braking, not checking your phone — telematics programs can produce dramatic savings. The key caveat: before enrolling, check with your insurer whether risky driving performance could negatively affect your rates. Some programs lock in a higher rate if your score is poor. Most offer a small guaranteed discount just for enrolling, regardless of your score. Link Assistant

Move 4: Raise Your Deductible

Potential savings: $100–$350/year

Raising your deductible from $500 to $1,000 reduces premiums by 15 to 20%. On a $1,800/year full coverage policy, that’s $270–$360 back in your pocket annually. Asinsight

The rule: only raise your deductible to an amount you could genuinely pay out of your emergency fund tomorrow. A $1,000 deductible on a policy that saves you $25/month takes 40 months of claims-free driving to break even. A $1,000 deductible when you have no emergency fund is a financial trap.

Move 5: Improve Your Credit Score

Potential savings: 15–40% on your premium

If your credit score is below 670 and you live in a state that allows credit-based insurance scoring, improving it is one of the highest-leverage moves available. Improving credit can reduce premiums by 15–40% in states that allow credit scoring for insurance. Zapier

The fastest credit levers: pay all bills on time, reduce credit card utilisation below 30%, and dispute any errors on your credit report (use annualcreditreport.com — free and official).

Move 6: Bundle Policies With One Insurer

Potential savings: $100–$400/year

Bundling home and auto insurance saves 15–25% on both policies. Amica offers up to 30% for bundling home and auto insurance — the largest multi-policy discount available among major insurers. SearchvolumeMonsterInsights

Caveat: the bundle discount isn’t always as sweet as it looks if the other policy’s rate is inflated. Always compare your bundled total against what you’d pay with separate policies at separate insurers. Searchvolume

Move 7: Drop Coverage That No Longer Makes Sense

Potential savings: $200–$600/year

For any car worth under $4,000–$5,000, dropping collision and comprehensive and carrying liability-only may save you hundreds per year — especially if the annual premium exceeds 10% of the car’s value. See our full breakdown in the comprehensive car insurance guide.

Also audit add-ons: rental reimbursement, roadside assistance, and gap insurance all have ongoing costs. If your circumstances have changed and you don’t need them, remove them.

5. The Quote Comparison Framework: How to Shop Correctly

Most drivers “shop around” by getting quotes with different coverage levels and comparing the headline numbers. That’s not shopping — that’s comparing apples to oranges.

Here’s how to do it correctly:

Step 1: Write down your current coverage specs exactly.

- Liability limits (e.g. 100/300/100)

- Comprehensive deductible (e.g. $500)

- Collision deductible (e.g. $500)

- Any add-ons (rental, roadside, gap)

Step 2: Get quotes from 3–5 insurers using identical specs.

Use the same limits, same deductibles, same add-ons across every quote. This is the only way to make a fair comparison.

Step 3: Include both national and regional carriers.

National brands (GEICO, State Farm, Progressive, Allstate) are well-known, but regional insurers often offer significantly lower rates in specific states. Erie Insurance, Auto-Owners, USAA (military only), and regional carriers are worth including.

Step 4: Compare total annual premium — not monthly payment.

Monthly payments often include financing fees. Always look at the annual total.

Step 5: Check the insurer’s claims satisfaction rating.

The cheapest policy from an insurer with poor claims service is a bad deal. Check J.D. Power claims satisfaction scores and NAIC complaint ratios before switching.

Step 6: Call your current insurer with your best competing quote.

Many insurers will price-match or offer a loyalty discount you weren’t previously receiving — but only if you call and ask.

For more everyday personal finance guides, browse InfoBrave’s Informative section — and explore InfoBrave for practical guides on insurance, finance, and lifestyle.

6. Frequently Asked Questions

Why did my car insurance go up if I didn’t have an accident?

Several reasons can raise your rate without any personal fault: industry-wide cost increases from higher repair costs, natural disasters, and litigation; changes in your credit score; a household member’s driving record; your annual mileage estimate; or simply your insurer adjusting rates in your region. Car insurance premiums surged dramatically between 2022 and 2024 and remain elevated in 2026, meaning even clean-record drivers are feeling the effects of industry-wide cost pressures. Semrush

How much can I realistically save by shopping around?

Comparing auto insurance quotes can save $200 to $800 annually. Most drivers can save $300 to $1,500 annually by combining multiple cost-reduction strategies. The exact amount depends on your profile, location, and how long it’s been since you last compared rates. Asinsight

Does my credit score affect my car insurance?

In most states, yes. In many U.S. states, insurers use a credit-based insurance score. Better credit equals a lower risk profile and a lower premium. Improving credit can reduce premiums by 15–40%. Exceptions: California, Hawaii, Massachusetts, and Michigan restrict the use of credit scoring for auto insurance. Zapier

How long does an accident stay on my insurance record?

At-fault accidents typically impact rates for three to five years depending on your state and insurer. Standard moving violations affect premiums for three to five years. Serious offenses like DUI can impact rates for five to ten years. After these periods pass, get new competing quotes immediately — your rate may drop significantly. Local Search Forum

Is it worth switching car insurance companies?

Often yes — especially if you haven’t compared rates in the past 12 months. Despite rate hikes, 87% of drivers did not switch insurers in the past year. Insurers frequently offer better rates to new customers than to long-standing policyholders. Always check claims satisfaction ratings before switching — the cheapest insurer with poor claims service is rarely the right choice. ALM Corp

Can I negotiate my car insurance rate?

You can’t negotiate in the traditional sense, but you can absolutely influence your rate. Call your insurer with a competing quote and ask whether they can match it. Ask your agent to audit every available discount on your policy. Ask about adjusting your deductible or coverage limits. Many insurers will adjust rather than lose you to a competitor.

What is the fastest way to lower my car insurance right now?

Get three to five apples-to-apples quotes in one sitting so you compare the same coverage, limits, and deductibles line by line. This single action — done correctly — consistently produces the largest immediate savings. Beyond that, call your insurer to audit your discounts, consider enrolling in a telematics program, and raise your deductible if your emergency fund supports it. Local Search Forum

Does where I live really affect my car insurance rate?

Significantly. Areas with high rates of natural disasters or litigation see more frequent insurance rate increases due to high costs per claim. Your specific ZIP code matters — not just your state or city. A move across town to a lower-theft, lower-accident neighbourhood can reduce your comprehensive and collision rates noticeably.

You may also like: What Does Comprehensive Car Insurance Cover? The Complete 2026 Guide